Company Analysis: Apple Retail UK FY2025

Winning the Channel Wars...

Key Findings: Apple Retail UK reported £2.79bn revenue for FY2025 (+8.1% YoY), with operating margin expanding to 4.04% (FY2024: 3.73%) despite gross margin compression. AppleCare+ sales reached £60-65m (+42-54% YoY) with unit-based attachment rates rising to 19-21% against 1.8m eligible devices sold. Revenue per store increased 11.2% on like-for-like basis whilst telco equipment sales declined across European markets, reinforcing structural channel displacement toward manufacturer direct sales. Full analysis available as a downloadable report at reports.finsur.co.uk

Last year's Apple Retail UK analysis confirmed what the consumer surveys had been suggesting: the telcos were losing their grip on device sales. Since then, the evidence has only strengthened with the Telco Equipment Revenues1 report documenting notable declines across European operators whilst consumer direct purchase rates continued climbing. So, with Apple Retail UK Limited (04996702) filing another year of results last week, and the channel displacement story now looking structural rather than cyclical, it seemed worth revisiting the UK retail entity for FY2025 up to 27/09/2025. Let’s dive in…

Recap

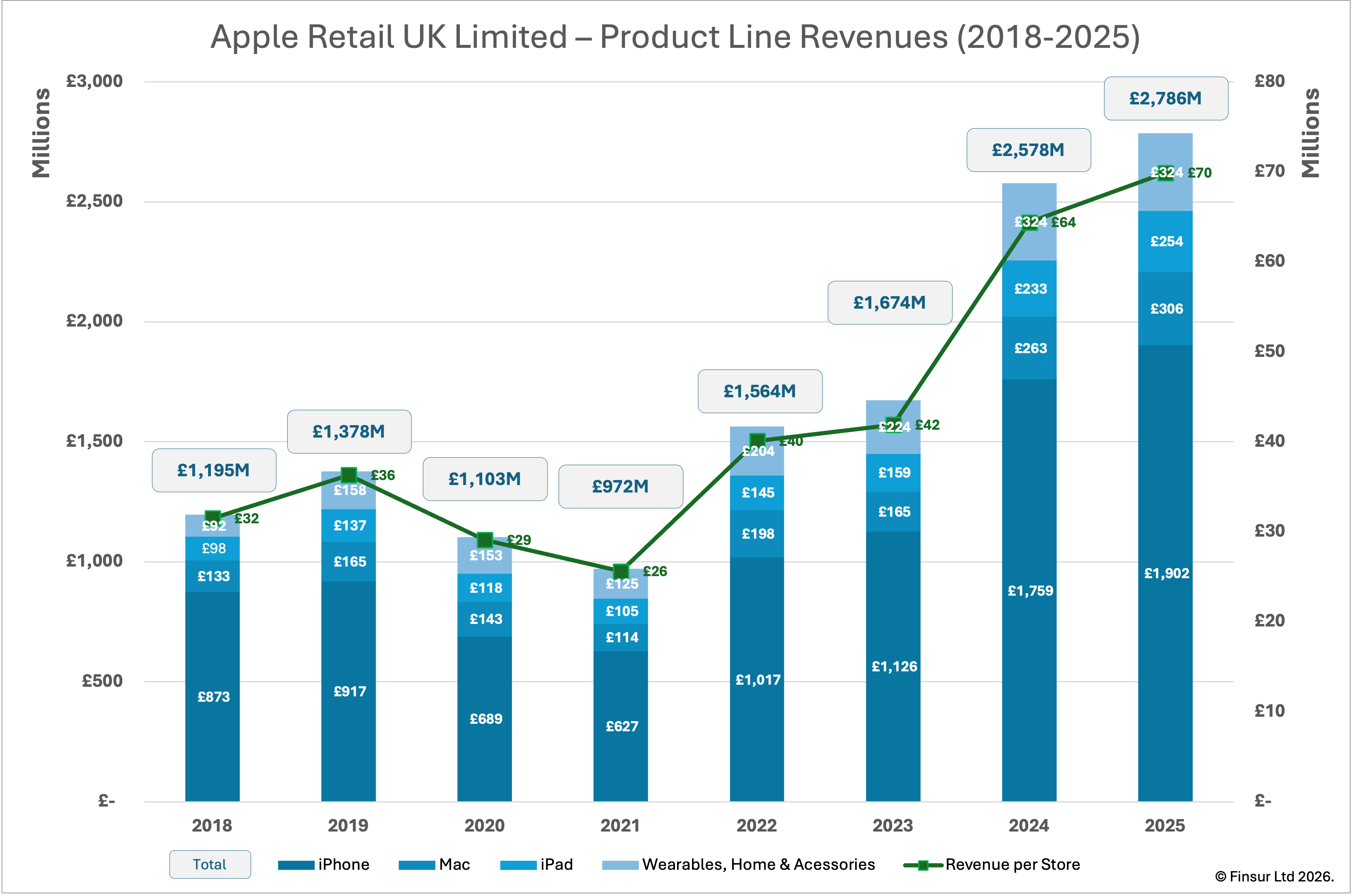

Apple Retail UK (ARUK) delivered exceptional FY2024 performance with revenues surging 54% to £2.58bn, demonstrating Apple’s ability to capture market share despite challenging economic conditions. Store productivity reached £64.4m per location whilst operating profit jumped 88% to £96m, suggesting the direct retail model was really beginning to hit its stride. AppleCare+ sales recovered sharply to £42.2m after a modest prior-year decline, with attachment rates stabilising around 12% on a unit basis.

The performance validated emerging consumer behaviour shifts favouring manufacturer direct sales over traditional telco channels. Consumer surveys throughout 2025 consistently showed Apple’s direct purchase rate approaching 25%, whilst telco equipment revenues began showing weakness across European markets setting the conditions for further channel displacement. FY2025 would test whether this momentum could be sustained and whether the strategic shift from carriers to direct retail had become permanent rather than cyclical.

Performance

FY2025 Key Performance Metrics:

- Total Revenue: £2.79bn (FY2024: £2.58bn, +8.1%)

- Gross Profit: £466.5m at 16.7% margin (FY2024: £436.2m at 16.9%)

- Operating Profit: £112.6m at 4.04% margin (FY2024: £96.1m at 3.73%)

- Profit Before Tax: £131.5m (FY2024: £115.1m, +14.3%)

- Revenue per Store: £71.4m like-for-like (FY2024: £64.4m, +11.2%)

- Revenue per Employee: £574k (FY2024: £534k, +7.5%)

- Store Count: 39 (FY2024: 40, Bristol closure)

- Employee Count: 4,850 (FY2024: 4,822, +0.6%)

Despite a significant deceleration from last year’s 54% growth surge, ARUK maintained healthy top line momentum through FY2025. Against a backdrop of suppressed consumer economics, lengthening ownership cycles and the higher comparative baseline, turnover increased 8.1% to £2.79bn (FY2024: £2.58bn). Their resilience over channel competition, particularly the telco’s who posted notable equipment sales decline through FY20252, indicates Apple’s continued market share gains and direct brand strength in the premium segment.

At finsur’s last count, Apple commanded 43.1% of the UK market3 with 24.8% of Apple customers purchasing directly from the manufacturer which would imply ARUK capturing approximately 1.8m device sales annually. That would place them among the largest single smartphone retailers in the UK, competing directly against the telco stores (39.2% market share) and the retail/marketplace channels (35%). Apple’s direct channel share significantly outperforms Samsung’s 17.2% direct sales rate which alongside brand loyalty and premium positioning, clearly justifies the investment in direct retail and service quality infrastructure.

Applying Apple Inc.’s global product revenue mix (excluding Services) to the ARUK turnover implies iPhone sales of £1.90bn, Mac sales of £306m, iPad sales of £254m and Wearables/Home/Accessories sales of £324m4. The estimated iPhone unit sales of 1.8m devices gives us an implied average (net) selling pricing of £1057 exemplifying Apple’s premium positioning but also possibly indicating a bias in the retail footprint towards Pro models.

With one seemingly enforced store closure due to the Cabot Circus redevelopment in Bristol, the ARUK store footprint dropped from 40 to 39. ARUK provides no revenue analysis, so ignoring online sales for the sake of comparisons and accounting for the store closure, per store revenue increased 11.2% to £71.5m on a like-for-like basis or to £69.9m in real terms. And, whilst further comparisons against other retailers might not quite be Apple’s to Apple’s, these levels significantly exceed say Curry’s Retail Limited at £2.4m per store, or VMO2 at £3.9m per store (equipment revenue only). This performance would suggest that the store network is apt to support further growth without proportional estate expansion should ARUK capture further channel migration.

The last revenue metric further demonstrates operation leverage within the store network. Average monthly employee count increased marginally (0.6%) to 4,850 (FY2024: 4,822) against the 8.1% revenue expansion, generating revenue per employee of £575,000 compared to £534,000 in the prior year. The minimal headcount growth suggests the retail model scales effectively, supporting margin expansion potential whilst continuing to maintain Apple's in-store experience that differentiates the brand from volume retailers.

Finsur is a reader supported publication. This level of research takes considerable time. Please consider becoming a paid subscriber to continue reading for:

Profitability deep-dive: How Apple absorbed wholesale pricing pressure whilst achieving 17% operating profit growth and a 31 basis point margin expansion

AppleCare+ evolution: New methodology reveals £60-65m sales estimates with attachment rates reaching 20% as monthly policies reshape the business model

Strategic shifts: Why Apple terminated the iPhone Upgrade Programme in favour of flexible finance accounts and what this signals about customer behaviour

Alternatively, this article is available as a single payment PDF report here.