Company Analysis: asgoodasnew FY2024

Refurbishing revenue targets...

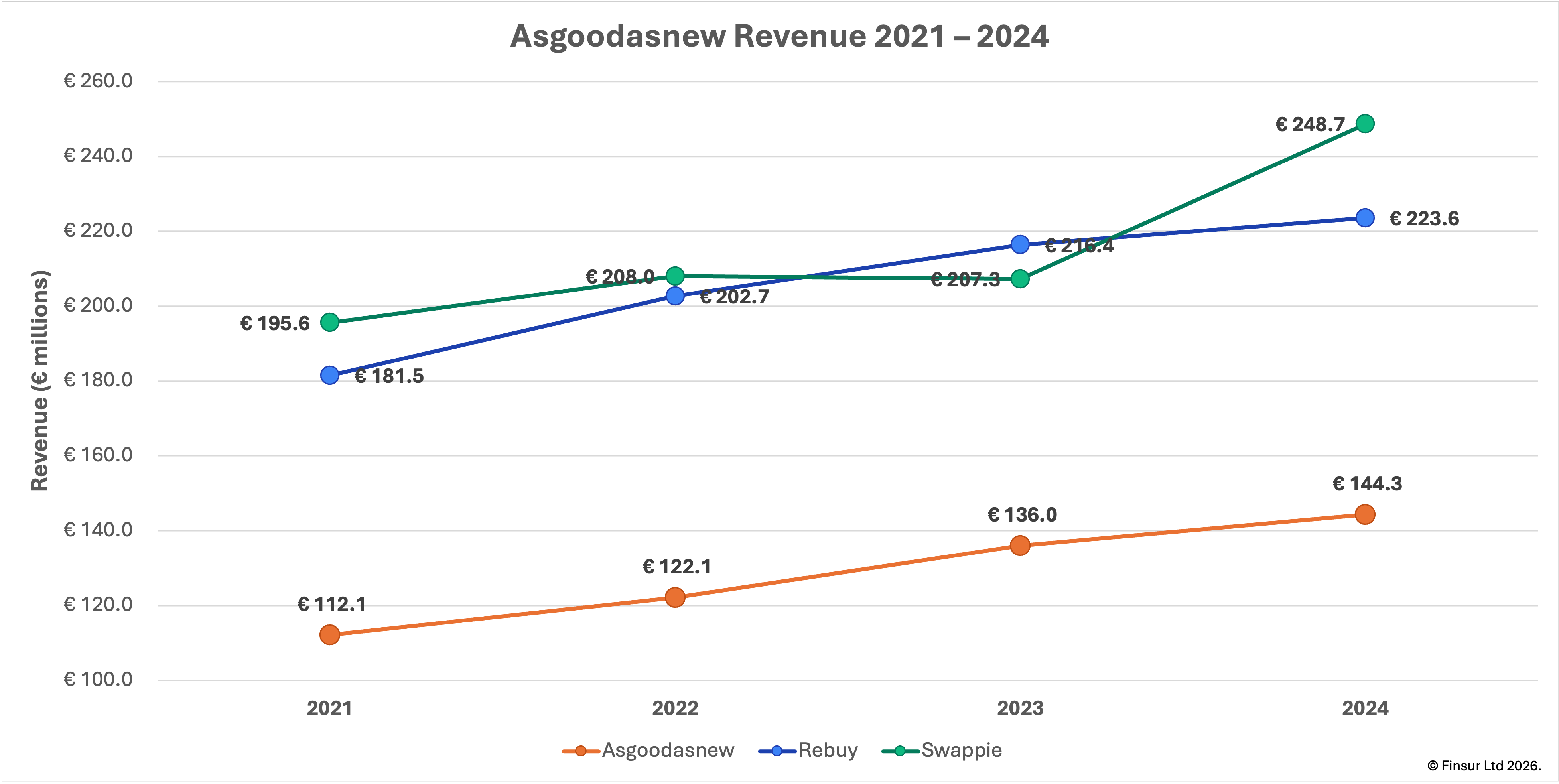

Key Findings: asgoodasnew reported €144.3m revenue in FY2024 (+6.1% YoY), with domestic own-platform sales exceeding €100m for the first time, but missing management guidance by €7.7m as the deliberate withdrawal from international marketplaces took effect. Gross profit declined to €19.2m at a 13.3% margin (FY2023: 14.5%) as aged stock clearance offset the channel strategy benefits, whilst a cost base built for €152m delivered a net loss of €6.9m, more than doubling the prior year. Management's Value Creation Plan revisits the €151m revenue target and monthly profitability in FY2025. Full analysis available as a downloadable report at reports.finsur.co.uk

The cyberattack on asgoodasnew (AGAN) at the beginning of the month1, exploiting a Klarna payment module vulnerability, wasn’t the type of news that any business owner or customer wants to hear about. The only positive is that it serves as a timely reminder to the secondary device sector that despite the noble sustainability mission, there’s no immunity from bad actors.

According to the management report in AGAN's recently filed FY2024 accounts, there's seemingly no immunity from the gap between predictions and reality either. FY2024 was characterised as a deliberate transformation year, one defined by channel simplification, organisational investment and a rebuild of the underlying IT infrastructure (uh oh); coherent and well presented framing, not without merit. But the accounts offer a more complicated story, and the distance between the narrative and the performance appears to have been harder to bridge. Let’s take a look…

Recap

AGAN is one of the leading specialist refurb retailers in Europe beginning life in 2008 and operating through two connected brands: WIRKAUFENS for acquiring devices from consumers and asgoodasnew for selling them back, to different consumers, one hopes. The product lines extend beyond mobile phones and include tablets, laptops, digital cameras/lenses and other CE items. They operate two locations: Frankfurt (Oder) for refurbishment operations and an HQ in Berlin. The business is led by Co-CEOs, Dr. Tim Seewöster and Stefan Groitl.

Just over a year ago in the European Marketplace Research Update2, I covered AGAN alongside Rebuy, Refurbed and Swappie and others, describing the business as being on a relatively stable financial footing and executing on a plan. AGAN, unlike Refurbed and Back Market, owns the full value chain; buying, refurbishing and selling directly, a model that demands more capital but offers greater control over quality, pricing and the customer relationship.

At that point, FY2023 data showed sustained, albeit modest progress with revenue improving, gross margin ticking up and a management team that confidently guided towards further revenue gains in FY2024 and a slightly positive EBITDA. The FY2024 filing up to 31/12/2024 is the first opportunity to assess whether that confidence was well placed.

Performance

FY2024 Key Performance Metrics

- Revenue: €144.3m (FY2023: €136.0m, +6.1%)

- Gross Profit: €19.2m at 13.3% margin (FY2023: €19.7m at 14.5%)

- Net Loss: €(6.9)m (FY2023: €(3.2)m)

- Cash: €3.4m (FY2023: €3.9m)

- Bank Debt: €14.6m (FY2023: €9.5m, +54%)

- Equity Ratio: 21% (FY2023: 43%)

- Employees: 171 average, generating €844k revenue per head (FY2023: 151 at €901k)

Source: asgoodasnew electronics GmbH (HRB 12158) filed accounts for the year ending 31 December 2024

I like German company accounts. First, they are readily available, delivered simply and directly via the government interface. Second, there appears to be no “notice of non-disclosure” to hide behind. Third, the management summaries very often provide the economic and strategic context in which the business operates. Now, it’s entirely feasible that the data can be challenged, but at least there’s a starting point for the analysis and discussion. So for context, according to AGAN’s FY2024 filing, German GDP contracted 0.2% in 2024, e-commerce recovered a modest 1.1% after an 11.8% decline in 2023 and whilst consumer caution persisted, management quoted that 50% of 19 - 39 year olds indicated they buy pre-loved goods more frequently3.

So, whilst there wasn’t exactly a tailwind, FY2024 revenue growth of 6.1% YoY to €144.3m (FY2023: €136.0m) missed management guidance by €7.7m, or approximately 5%. Close enough? Domestic sales generated €109.9m, up 13.6% (FY2023: €96.7m), with their own platform exceeding €100m up 17%, leaving approximately €10m flowing through what I assume are third-party marketplaces or trading channels. That implies tactical sales optimisation is operating effectively in the home market. International revenues fell 12.3% to €34.5m (FY2023: €39.3m) after deliberately pulling back from third-party marketplaces. Clearly there’s a marketing spend v commission v profit trade-off but the net effect this time appears to have compressed growth. Perhaps not materially, but enough to take a decent chunk out of the revenue guidance.

The closest direct analogue is Rebuy. Same model, same contracting home market against which AGAN’s 6.1% headline growth stands out against Rebuy’s 3.3% top line improvement, although excluding media, their consumer electronics revenue grew 5.7%. Swappie’s 20% revenue growth came from international markets as their home market (Finland) declined 13.1% and was explicitly driven by increased marketing investment.

Management, as might be reasonably expected, don’t provide product line or grade mix splits in the accounting notes. Therefore, a review of the website listings at the time of writing shows 726 SKUs of which approximately 51% are Apple and 49% Android across Samsung, Google Pixel, Xiaomi, Huawei and other brands. Whilst that isn’t a reliable proxy for revenue mix, in the UK, Apple has historically commanded approximately 75% of device revenues on 55% volume share4, illustrating the ASP premium that Apple carries over Android. The UK and German markets differ, but the underlying dynamic, that Apple buyers trade up on grade and specification more consistently than Android buyers is broadly applicable. Applied to AGAN’s roughly 51% Apple SKU share, a revenue contribution of 65% - 70% from Apple feels conservative rather than aggressive, and implies a blended ASP in the €300 to €320 range. I’m not bothering to untangle marginal VAT here so taking it directionally and applying it to the €144.3m revenue implies approximately 315k to 340k unit sell through.

Continue reading for:

The cost structure that turned a revenue miss into a doubling of losses

The warranty provision revealing more about customer retention than the P&L

What’s riding on the Value Creation Plan

Alternatively, the full report is available in PDF format here.