Company Analysis: ATRenew Q4 FY2025

The horses are coming, so you better run...

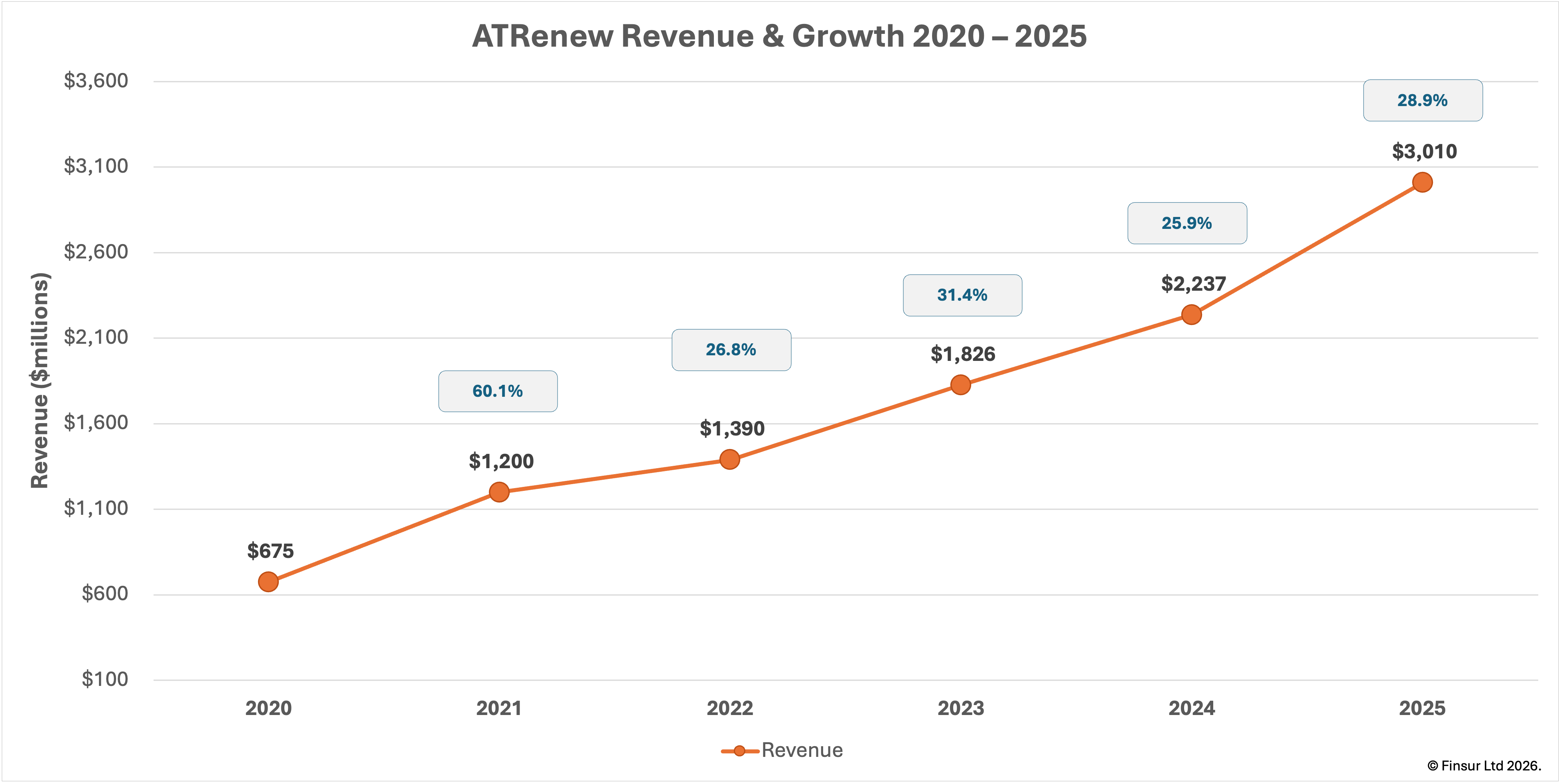

Key findings: FY2025 total net revenues RMB 21,048m (USD 3,010m) | +28.9% YoY | five-year CAGR ~34%. First full year of GAAP profitability in company history: operating income RMB 456m (USD 65m), net income RMB 336m (USD 48m). Non-GAAP operating income RMB 555m (USD 79m) at 2.6% margin, +35.5% YoY. 1P gross margin expanded 200bps to 13.8% as direct-to-consumer retail reached 36.8% of product revenues. Balance sheet conservative: disclosed liquidity of US$312.8m against short-term borrowings of US$46m and no long-term financial debt. NYSE market capitalisation of approximately $1bn against $3bn FY2025 revenues implies a sub-0.4x revenue multiple, a material discount to European marketplace peers despite the first full year of GAAP profitability. JD.com, ATRenew's largest shareholder and primary commercial partner, is acquiring CECONOMY, parent of MediaMarkt and Saturn, across more than 1,000 European stores; their cooperation agreement runs to December 2030. Full analysis available as a downloadable report at reports.finsur.co.uk.

Back in July 2025, JD.com announced the voluntary public takeover of CECONOMY, parent of MediaMarkt and Saturn. At €2.2 billion, the largest Chinese acquisition of a consumer electronics retailer was bound to attract regulatory scrutiny. After antitrust clearances in Germany, Italy and France, it fell to Austria’s foreign investment ministry to put a spanner in the works on the grounds of security, public order and critical infrastructure concerns. The Austrian outcome is now uncertain with a carve-out being floated as one solution. Regardless of that particular outcome, JD.com will end up controlling Europe’s largest physical consumer electronics retail network.

JD.com also happens to be ATRenew’s most important customer providing the primary upstream source of trade-in volume, a significant shareholder and the counterparty to a cooperation agreement renewed in March 2026 to run until December 2030. After management stated their intention to integrate with the international layout of their strategic partners back in Q3 last year and then the General Manager of International Business appeared on a CCS Circular Market panel in February this year, I’ve been wondering what ATRenew’s logistics, inspection, grading and pricing infrastructure does inside a JD.com-controlled European retail footprint. Let’s have a look…

Recap

AiHuiShou was founded in 2011 in Shanghai and subsequently renamed to ATRenew in September 2020. Nine months later in June 2021 ATRenew listed via IPO on the NYSE valuing the business at approximately $3.09bn. There’s a Cayman Island holding company with operations currently conducted entirely through Chinese subsidiaries via four operating divisions: AHS Recycle (C2B collections), PJT Marketplace (B2B merchant trading), Paipai Marketplace (B2C consumer resale) and AHS Device (international).

Paipai was integrated from JD.com in 2019 and as part of the agreement, JD led a new round of financing to become a significant shareholder, the primary upstream source via the AHS Recycle trade-in integration and the platform via which Paipai reaches consumers. The cooperation agreement runs to December 2030. In addition to JD, ATRenew have trade-in partnerships with Apple, Huawei, Xiaomi, Oppo and Vivo providing additional C2B supply. As at the end of 2025, ATRenew operated 2,195 AHS Recycle stores across China supported by door-to-door collection, express mail-in and more than 2000 proprietary self-service kiosks.

Revenue crossed $2bn in FY2024 and $3bn in FY2025 with a five-year CAGR from FY2020 to FY2025 of approximately 34%. FY2025 marked the first full year of GAAP operating profitability in the company’s history with multi-category recycling (gold & luxury goods) growing rapidly but still a small proportion of the overall mix; smartphones and consumer electronics remain the dominant category. Since the launch price of approximately $18 per share, the stock fell to a low of $1.08 at the beginning of 2024. Since then, there’s been a consistent rise back up to the $5-6 range1.

AHS Device’s international operations are active across Southeast Asia and the Middle East with monthly export volumes exceeding 10,000 units as of Q3 2025. The unit has also made equity investments in Cashify (India) and Trocafone (Brazil). They have partnered with Janpara (Japan) for self-service kiosks2 and collaborated with Swappie on kiosks in Sweden3.

Performance

Key Performance Metrics:

- Full Year FY2025 (year ending 31 December 2025):

- Total net revenues: RMB 21,048m | USD 3,010m | +28.9% YoY

- Net product revenues (1P): RMB 19,380m | USD 2,771m | +30.6% YoY | 92.1% of total

- Net service revenues (3P): RMB 1,668m | USD 239m | +12.4% YoY | 7.9% of total

- Implied gross profit: RMB 4,348m | USD 622m | ~20.7% margin (+60bps)

- 1P gross margin: 13.8% (FY2024: 11.8%, +200bps)

- GAAP income from operations: RMB 456m | USD 65m | 2.2% margin (+199bps)

- Non-GAAP income from operations: RMB 555m | USD 79m | 2.6% margin (+13bps)

- GAAP net income: RMB 336m | USD 48m (FY2024: net loss RMB 8m)

- Products transacted: 41.7 million (+18.1% YoY)

- AHS stores: 2,195 across 298 cities

Q4 FY2025:

- Total net revenues: RMB 6,254m | USD 894m | +29.0% YoY

- Net product revenues: RMB 5,831m | USD 834m | +30.7% YoY

- Net service revenues: RMB 423m | USD 61m | +8.8% YoY

- 1P gross margin: 13.7% (Q4 FY2024: 12.5%, +120bps)

- Non-GAAP income from operations: RMB 182m | USD 26m | 2.9% margin (+19bps)

- 1P-to-C retail share of product revenues: 41.7% (Q4 FY2024: 29.0%)

- Products transacted: 11.0 million (+17.0% YoY)

Q1 FY2026 guidance: RMB 5,860-5,960m | USD 838-852m | +25.9-28.1% YoY

Source: ATRenew Inc. Q4 and FY2025 earnings release and investor presentation, March 11, 2026

It’s probably worth addressing the scale differential upfront. In FY2025 ATRenew (ATR) transacted 41.7 million consumer products, up from 35.3m in FY2024. In Q4 alone, 11 million products were processed. For context, that’s roughly twice the size of the European organised secondary market4. It’s also worth noting that ATR reports under US GAAP with an explicit GAAP to non-GAAP reconciliation. If you’re unfamiliar or interested in the implications for revenue and profit presentation, check out the explanation in the Methodology section.

ATR operates two models. The first-party (1P) model involves buying the device outright, taking it onto the balance sheet and selling it on, bearing the inventory and price risk with revenue recorded at the full transaction value. The third-party (3P) model involves ATR providing the platform infrastructure and charging a commission or fee with the seller retaining the inventory. In practice AHS Recycle and Paipai are predominantly 1P and the PJT Marketplace, where merchants trade between themselves, is predominantly 3P generating the service revenue line.

Total FY2025 revenues increased to RMB 21,048m (USD 3,010m) beating the top-end guidance issued with the Q3 results, and increasing 28.9% YoY (FY2024: USD 2,237m). Net product revenues in the 1P business increased 30.6% to RMB 19,380m (USD 2,771m) representing 92.1% of the total. Net service revenues grew 12.4% to RMB 1,668m (USD 239m) with commissions and platform fee revenue representing 7.9% of the total.

Total Q4 FY2025 net revenues hit RMB 6,254m (USD 894m) which was a 29.0% increase on the same quarter in the previous year. This follows Tim Cook’s Q4 report of Apple’s “great quarter” riding the replacement wave in China from the iPhone17 launch which drove strong trade-in volumes. Net product revenues accounted for RMB 5,831m (USD 834m) growing 30.7% and net service revenues grew 8.8% to RMB 423m (USD 61m). Retail revenues in Q4, direct 1P sales to consumers, reached 41.7% of overall product revenues.

Continue reading for:

What a 200 basis point gross margin improvement actually means for the operating model

The one expense line growing twice as fast as revenue, and why management is relaxed about it

Why the balance sheet tells a more interesting story than the headline cash figure suggests

Alternatively you can download the full pdf report here.