Company Analysis: Foxway Q4 FY2025

Boggis, Bunce or Bean...

Key Findings: FY2025 net sales SEK 7,833.6m | ~€675.3m | +3.2% cc, driven entirely by C&E (+12.0% cc) as CWS and Mobile both declined. C&E margin expanded from 4.8% to 8.5% on AI infrastructure demand that management itself attributes to external tailwind. Group AdjOp. EBITDA declined 3.8% to SEK 292.0m | ~€25.2m. Operating cash flow collapsed to SEK 1.0m as interest consumed 44.6% of EBITDA. Bond fair value implies mid-70s cents versus par a year ago; covenant headroom narrows from approximately €87m to approximately €26m at the July 2027 step down.

Boggis, Bunce and Bean, one fat, one short, one lean. These horrible crooks, so different in looks, were nonetheless equally mean. The three demands on Foxway’s cash are equally unforgiving: the interest bill, working capital and investment. Let’s hope Patrick Höijer can keep his tail.

Recap

This is the fourth Finsur article on Foxway1, so only a gentle reminder of the operating model with three reporting segments: Circular Workspace Solutions (CWS) providing device-as-a-service solutions for workspace equipment to mid/large corporates and the public sector in the Nordics; Recommerce Mobile (Mobile) providing trade-in solutions and asset recovery services for smartphones, focusing on mobile operators, retailers and partners, and; Recommerce Computers & Enterprise (C&E) handling computers, business equipment and network products sourced from OEMs, financing companies, data-centres and resellers.

Foxway's previous results have been characterised by generally improving performance at the company level balancing revenue and profit variability in the reporting segments. This time last year CWS collapsed 35% after a significant client loss, Mobile was the profit engine delivering 12.6% operational EBITDA margin and C&E lagged at 4.8% margin with persistent low overstock volumes pressuring returns. H1 2025 continued the challenging dynamic with overall revenue down 7.0% YoY; CWS swung to an operational EBITDA loss whilst the Mobile and C&E segments quietly delivered 20%+ EBITDA growth. With Q3 FY2025 showing some stabilisation, the question for management was whether the final quarter would be enough to salvage the year.

In my Q2 2025 article I examined the debt covenant and concluded that Foxway was above the 4.50x threshold and therefore locked out of any meaningful M&A. In January this year, after Foxway announced the acquisition of ABD in Romania, I reviewed the covenant terms again and corrected my analysis to exclude sale and leaseback liabilities and use the Alternative Net Debt value which came in at 3.30x giving approximately €72m of headroom. The ABD acquisition, a Romanian computer refurbishment business with SEK 110m in revenues, completed post quarter and served as the first practical test of that revised headroom.

With Nordic Capital now well into their third year of ownership and the transformation from growth to sustainable profitability being led by CEO Patrick Höijer now for the last 18 months, the numbers in the Q4 FY2025 release looked strong. But as this coverage has repeatedly demonstrated, the headline numbers at Foxway can obscure as much as they reveal. Let’s dive in…

Performance

Key Performance Metrics

- Net Sales: SEK 7,833.6m (€675.3m), +0.4% reported, +3.2% cc

- Q4 Net Sales: SEK 2,129.3m (€183.6m), +17.4% reported, +22.9% cc

- C&E Full Year: SEK 2,612.4m (€225.1m), +7.6% reported, +12.0% cc

- CWS Full Year: SEK 2,473.6m (€213.2m), -2.1% reported, -1.1% cc

- Mobile Full Year: SEK 2,828.4m (€243.8m), -5.4% reported, -2.3% cc

- AdjOp. EBITDA: SEK 292.0m (€25.2m), -3.8%, margin 3.5%

- Adjusted EBITDA: SEK 706.4m (€60.9m), +3.0%, margin 9.0%

- Operating Cash Flow: SEK 1.0m (€0.1m), FY2024: SEK 292.1m

- Alternative Net Debt: SEK 2,172.0m (€187.2m), leverage 3.07x

- Net Loss: SEK -547.6m (€-47.2m) incl. SEK 350.4m goodwill impairment

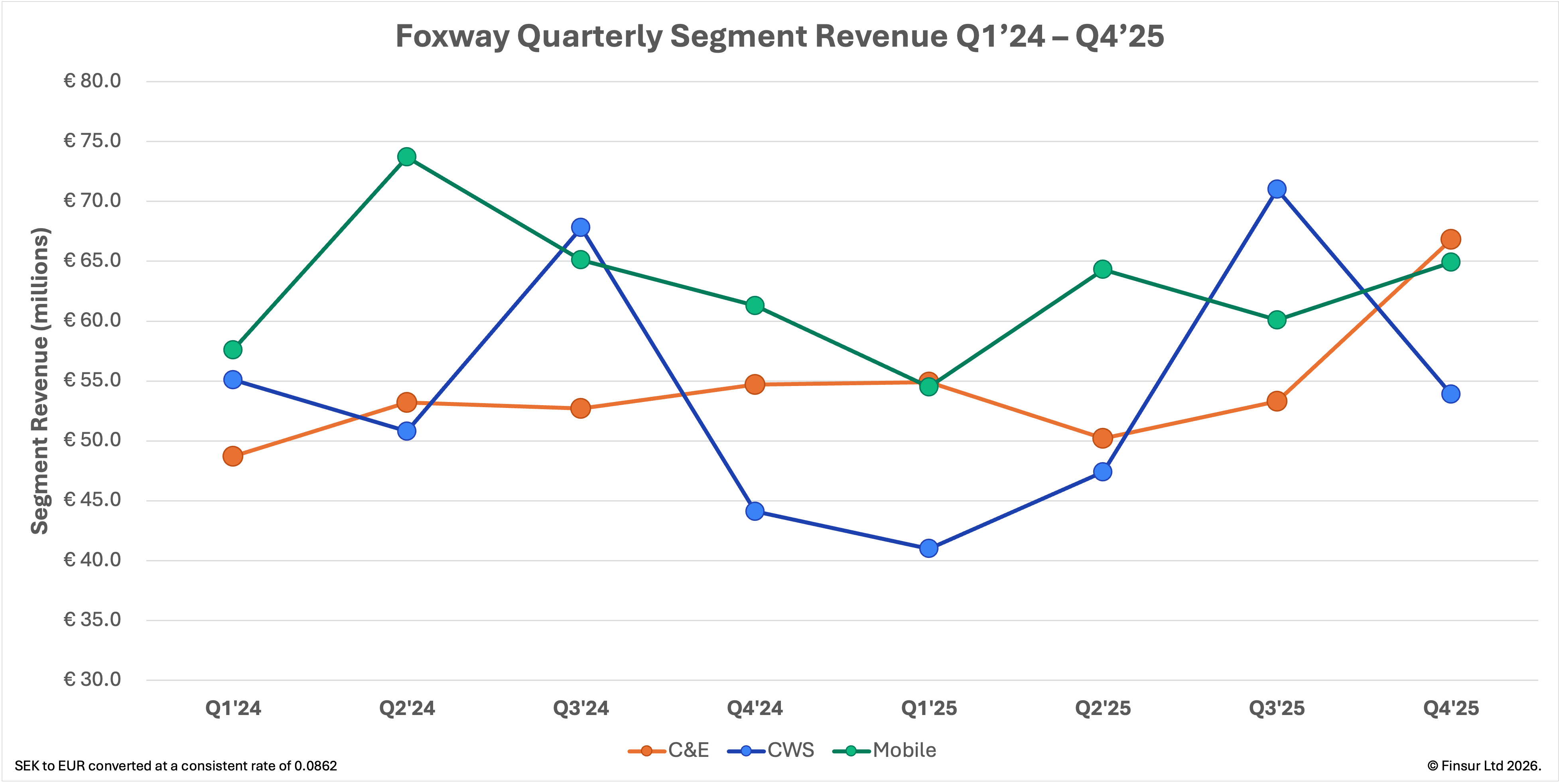

Q4 top line net sales grew 17.4% (22.9% constant currency) to SEK 2,129.3m (€183.6m) resulting in the strongest quarterly revenue in Foxway’s reporting history. Importantly, all reporting segments contributed growth which is the first time that’s happened since coverage began. The Q4 acceleration just about saved the year, papering over the weakness of the first three quarters, with 0.4% or 3.2% on a constant currency (cc) basis growth to SEK 7,833.6m (€675.3m). It would be easy to claim the Q4 result suggests some momentum, but the full-year results are more indicative of three businesses still finding their rhythm: the growth was entirely driven by C&E (+12.0%) with CWS (-1.1%) and Recommerce Mobile (-2.3%) declining on a full-year basis. The full year picture is beginning to reveal three stories beyond simple variability.

C&E: Q4 net sales grew 22.1% (31.0% cc) to SEK 774.3m (€66.7m) offering the standout performance result by a considerable margin. CE had been the most consistent of the three segments, trading in a narrow quarterly range of the prior seven quarters, making the Q4 breakout notable. Full year net sales increased 7.6% to SEK 2,612.4m (€225.1m) or 12.0% cc ending the year as the only segment delivering full year growth and the sole driver of group level constant currency improvement. Management attributed the Q4 surge to enterprise equipment demand driven by AI data centre capacity expansion, with pricing levels continuing to increase through the quarter.

At Teqcycle, Foxway’s premium refurbished computer brand, volumes more than doubled YoY scaling across European markets and the ABD acquisition will add additional computer refurbishment capacity. Höijer framed the acquisition as building a second processing hub, mirroring the Tartu mobile facility in Estonia. That’s a strategic bet on C&E’s trajectory continuing despite overstock and computer recovery services remaining below prior years, implying Teqcycle and enterprise equipment are expected to become the segment’s dominant revenue drivers.

The key question looking at C&E is how much of the upswing is the AI infrastructure cycle (cyclical) versus Foxway’s improved positioning in enterprise refurbishment (structural). The year end report describes C&E’s performance as driven by an “AI-led market upswing” and references supply chain disruptions leading to rising prices and increased market activity; management’s own framing appears to lean on the external tailwind rather than operational execution. Höijer also emphasised AI driven memory chip shortages as a key factor and indicated that major hardware vendors are signalling significant price increases across key product segments heading into 20262. Whilst this is positive for C&E’s near term outlook, it reinforces the view that current performance is partly supply-constrained pricing rather than pure volume growth.

CWS: Q4 net sales improved 22.3% (24.0% CC) to SEK 625.1m (€53.9m). The growth was driven by first lifecycle device sales as newly onboarded customers from the Q1 2025 contract signings finally began to flow through the P&L.

The lease component is worth a closer look. Operational net sales, which includes the value of leased devices, increased 15.5% to SEK 730.1m (€62.9m) lagging the net sales. The implied lease component shrank from SEK 120.9m (€10.4m) in Q4 2024 to SEK 105.0m (€9.1m), a 13% decline. The full year confirms the pattern. Operational net sales SEK 2,904.1m (€250.3m) vs SEK 3,017.1m (€259.9m), -3.7%; the lease component contracted 12.2% from SEK 490.6m (€42.3m) to SEK 430.5m (€37.1m). This implies the new customer onboarding is weighted towards outright equipment procurement rather than the recurring DaaS model that forms the basis of the CWS proposition. Fewer devices on lease also means fewer coming off lease, explaining the decline in second lifecycle sales that management flagged.

CWS full year net sales SEK 2,473.6m (€213.2m) vs SEK 2,526.5m (€217.7m), -2.1% reported, -1.1% constant currency; so despite Q4’s recovery the full year was still negative. The 2024 customer churn event and replacement freezes from major clients weighed on the first three quarters. But with new customer onboarding starting to show revenue impact from Q3, management implementing a new operating model during Q4 and launching a new customer portal, the strong pipeline should assist continued revenue recovery through FY2026.

Mobile: The 6.0% increase in Q4 net sales to SEK 753.1m (€64.9m) on a 10.9% cc basis looks like a recovery at first, but needs unpacking. Management explicitly stated that Q4 revenue growth was “largely driven by price discounts in effort to reduce inventory levels ahead of Q1 2026”, implying the volume was bought with margin, not organic demand improvement.

The clearance pattern echoes last year. Management entered 2025 excited about the Samsung Galaxy S25 launch driving Q1 trade-in volumes (and it did), then spent the middle quarters selling through Samsung inventory before discounting in Q4 probably to clear ahead of the next cycle. As noted in my Q4 FY2024 article, I was sceptical that any phone launch would be the vanguard of a supercycle and the FY2025 trajectory suggests this is becoming an annual working capital treadmill rather than a growth catalyst.

The Apple side of the equation is arguably more concerning. iPhone launches in September/October should drive a Q4 sourcing surge, but Foxway has consistently found it difficult to benefit. The Q3 report explicitly stated the expected post-iPhone seasonal uplift had not materialised, with every quarterly report throughout 2025 flagging Apple sourcing as challenging due to competitors accepting lower margins and high market prices on popular models. Foxway's mobile sourcing is increasingly dependent on one OEM's product cycle whilst being priced out of the other. This is beginning to feel like a capability gap.

Full year net sales ended down 5.4% or down 2.3% (cc) at SEK 2,828.4m (€243.8m) versus SEK 2,988.6m (€257.4m) in FY2024. The decline was driven by slower sourcing activities early in the year, weaker Marketplace sales, a failure of the expected post-iPhone seasonal uplift to materialise, and continued aggressive competitor pricing particularly on Apple products. In the year end interview, Höijer conceded there were “some temporary headwinds” and when pressed on whether the weakness was structural, pivoted to talking about the market size rather than answering the question directly. Whether the stated priorities of margin improvement, sourcing optimisation and platform development (including AI based trade-in grading) are enough to beat the competition in the Apple auctions, is very much an open question.

Continue reading for:

Why C&E’s record margins may not be what they seem and what it means for the PE thesis

The balance sheet dynamics behind a business generating SEK 706m in EBITDA and SEK 1m in operating cash flow

Three events converging within eighteen months that will define whether this is a credit recovery or a restructuring conversation

Alternatively, this article is available as a PDF here.