Company Analysis: PCS Wireless FY2024

Let's tessellate...

Key Findings: One of three Apple Trade In vendors across nine European markets, plus Google's Pixel partner. Excelsior revenue doubled to €172m; combined European gross billings approached €300m equivalent, though intercompany flows obscure actual throughput. Transfer pricing architecture delivers controlled entity returns; combined European profit floor of €6.5m to €7.0m with the real contribution to PCS Wireless LLC invisible. Obsolescence provision at 35.8% of gross inventory is a structural outlier; every comparable is below 14%. UK Ltd capitalisation of £93k supporting £63.3m revenue (680x) defines asset light. Estimated European device intake: 1.0m to 1.5m units annually.

Apple’s legal pages can be very insightful, especially living in a jurisdiction that values transparency and consumer disclosure. Note the difference between the Apple legal trade-in page for e.g. Germany listing Alchemy, Likewize and PCS Wireless (because the Consumer Rights Directive requires consumers to be informed of the identity of any trader they are contracting with, not especially controversial), versus e.g. Canada which simply states that a third-party vendor exists. That list of three third-party vendors reminded me that I’ve yet to cover PCS Wireless and, given their importance in the secondary market, I was happy to start rectifying that oversight, and then I sat down with the accounts.

Recap

PCS Wireless LLC was founded in 2001 by Ben Nash and Praveen Arora, operating from New Jersey and Miami Lakes, FL. The company operates in the wholesale distribution, recovery, refurbishment and redistribution of pre-owned devices across 80+ countries. And, given my desire to dig through financial reports, to my mild and temporary annoyance, it remains privately held with no consolidated accounts in the public domain. Although that’s a decent caveat for any errors on my part. Every cloud.

PCS Wireless's European presence dates to 2013, when PCS Wireless NL Coöperatief U.A. (KvK 57921180) and PCS Wireless Espana 2013 S.L. were established as the group's continental wholesale trading vehicles, generating consolidated revenue of €159.4m by FY2022. UK operations followed with the incorporation of PCS Wireless UK Limited (12329873) in 2019 and PCS Wireless UK Mobile Limited (13518201) in 2021, both under the inimitable Fergal Donovan (now Cyculus) as regional president until 2023. The OEM trade-in business routes through PCS Excelsior Wireless Coöperatief U.A. (KvK 77551788), established in the Netherlands in March 2020 and co-directed by Donovan alongside Bashar Nejdawi (ex Brightpoint, Ingram and Clover), who also served as group COO and Chief Strategy Officer. Dutch commercial leadership passed to the also inimitable Pieter Waasdorp between 2022 and 2023. Lazer Herson’s 14 year tenure, latterly as CEO, preceded Ben Nash returning to pick up the position at the beginning of this year.

The distinction between the vendor T&C’s listed on the Apple legals is that, so far as PCS Wireless (PCS) is concerned, Apple provides the customer service for the trade-in programme including: the determination of whether the device is eligible for trade-in, taking possession of the device and inspecting the device, which implies that PCS is responsible for the Apple in-store trade-ins. The Alchemy and Likewize T&C’s are both structured around the consumer shipping the device to the vendor directly, which implies the online/mail-in model. Following the legal trail left by the Apple URLs would further suggest that PCS are responsible for the in-store programme in the UK, France, Germany, Italy, Spain, The Netherlands, Australia, Vietnam and Saudi Arabia. This article is focused on PCS performance in the UK and EU markets.

The European corporate structure has evolved considerably since PCS first established its presence. PCS Wireless NL Coöperatief U.A. (KvK 57921180) was originally the European sub-group holding company, filing consolidated accounts that included PCS Wireless Espana and AMLAT PCS Wireless Dominican Republic underneath it. During FY2023, both the Spanish and Latin American entities were transferred to PCS Wireless LLC in New Jersey, along with the 51% stake in Dignitas Distribution B.V. and the dormant Latam Cellular Holdings LLC. By the end of that process, PCS Wireless NL Coöperatief U.A. had been stripped back to a treasury and cash pooling function, with its consolidated revenue falling from €159.4m in FY2022 to €113.5m in FY2023 as the transferred entities dropped out mid year. PCS Wireless Ireland Limited, which had previously traded in mobile and computer technology, went inactive in 2023. The operational centre of gravity has appeared to shift to PCS Excelsior Wireless Coöperatief U.A. (KvK 77551788) as the primary European trading vehicle, supported by PCS Services NL Coöperatief U.A. running the Rosmalen processing hub acquired from New ComServe Group in 2022. Today, all European entities sit as direct subsidiaries of PCS Wireless LLC rather than underneath each other; the group runs flat, not hierarchical, which should make for easy reading, shouldn’t it?

Key Performance Indicators

Excelsior (77551788) FY2024: Revenue: €172.0m (FY2023: €84.1m, +104%) Gross margin: 5.0% | Net profit: €3.85m Net inventory: €6.13m (gross €9.54m less €3.42m provision) Receivables: €64.3m (€63.25m intercompany) Operating cash flow: -€19.99m

UK Ltd (12329873) FY2024: Revenue: £63.3m (FY2023: £28.3m, +124%) Gross margin: 1.3% | Net profit: £1.42m Stocks: £12.71m (FY2023: £5.57m, +128%) Employees: 37 | Net assets: £93k

Mobile UK (13518201) FY2024: Revenue: £57.7m (FY2023: £22.3m, +159%) Gross margin: 0.4% | Net profit: £1.60m Employees: 0 | Net assets: £2.43m

Source: Filed accounts for periods ending 31 December 2024

Performance

Headlines

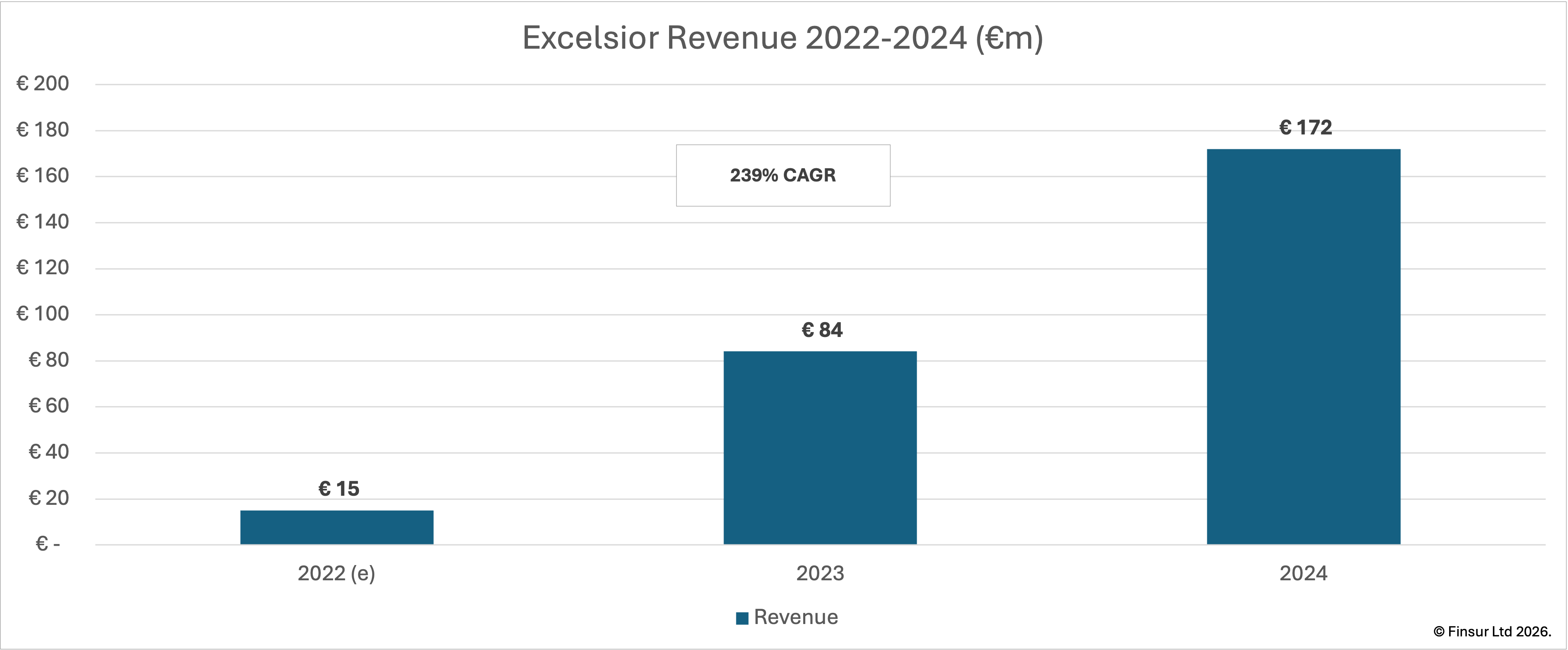

PCS Excelsior Wireless Coöperatief U.A. (“Excelsior”) posted revenues of €172.0m in FY2024, a 104% increase on the prior year (FY2023: €84.1m). The size of the business in FY2022 meant full accounts did not need to be filed, but a 452.65% net sales growth disclosed in the FY2023 filing, implies the FY2022 revenue was approximately €15m. That’s a significant three-year trajectory.

The UK operations run through two entities that serve distinct acquisition channels. PCS Wireless UK Limited (“UK Ltd”) wrote £63.3m in FY2024 and is the contracting party for Apple and Google Trade-In, acquiring devices directly from UK consumers under the OEM programmes. PCS Wireless Mobile UK Ltd (“Mobile UK Ltd”) appears to source devices from external trade suppliers, with its creditor profile implying purchases predominantly from non-group counterparties. FY2024 revenue for the Mobile UK Ltd was £57.7m and entirely from internal sales into the wider PCS group.

Altogether, the three European trading entities generated gross billings approaching the equivalent of €300m in FY2024. However, substantial intercompany flows mean that the actual revenue is likely to be much smaller and all the above entities are direct subsidiaries of PCS Wireless LLC, which doesn’t have to file. Grrrrr.

Intercompany Architecture

The filed accounts reveal a multi-entity structure where each node serves a specific transfer pricing function rather than representing an independent business. UK Ltd is explicitly described as a limited risk entity: “The Company risk is limited, and PCS Wireless Group bears the risk through the transfer pricing policy.” Its debtor profile (£19.5m owned by group undertakings, versus £1.4m in trade debtors) confirms the revenue must be mostly intercompany. A £3.95m “Management Fee Income” is exactly offset by a £3.95m “Transfer Pricing Adjustment” disclosed as an exceptional item, leaving UK Ltd with a controlled operating profit. The fee compensates for the operational work at their Bracknell facility.

UK Ltd’s entire £57.7m is classified as “Intercompany Sales” in accounting note 3, with all revenue arising in the United Kingdom. The £18.5m in trade creditors versus just £113k owed to group undertakings implies that it buys from external suppliers and sells back into the group. It has zero employees, two directors and a token 0.4% gross margin with profit driven by £1.9m from other operating income. This is a paper entity sitting between external device sourcing and the group’s continental processing infrastructure.

Excelsior carries a €63.3m receivable from PCS Wireless NL Coöperatief U.A., comprising €34.2m in trade debtors, a €21.1m current account, and €8.0m in invoices and credit notes. Cross-referencing against FY2023 accounts, which showed a €20.9m trade creditor owed to Excelsior subsequently confirming the direction: Excelsior sells to the PCS Wireless NL Coöperatief entity, not the other way around. The relationship has scaled dramatically (from €24.2m to €63.3m year on year). This implies that a significant portion of Excelsior's €172m revenue likely represents intercompany sales, which in turn distributes to external wholesale customers across Netherlands, EU, and non-EU markets.

The connection between the UK entities and Excelsior is less visible. Both UK entities take advantage of the FRS 102 s33.1A exemption, declining to disclose related party transaction detail. Excelsior's only disclosed relationship with a UK entity is an immaterial €136,632 current account with Mobile UK Ltd (settled in early 2025). UK Ltd's £21.6m "Rest of World" revenue is the most likely route for devices flowing from the UK acquisition channel to continental distribution, but the specific counterparty cannot be confirmed from the filed accounts alone.

Indicative Volumes

Volume estimation requires selecting which entity’s revenue best reflects actual device throughput. Excelsior’s €172m is probably the most useful proxy despite the intercompany element, because the devices flowing through it are real regardless of whether the next buyer is internal or an external customer. At an estimated B2B wholesale ASP of €175 to €200, reflecting a mixed grade and brand portfolio sold at a significant discount to consumer refurbished pricing, Excelsior’s revenue implies throughput of 860,000 to 980,000 devices annually.

The UK acquisition channels add further volume, although the degree of overlap with Excelsior’s figures means that a simple addition would probably overstate the position. UK Ltd’s £63.3m and Mobile UK’s £57.7m include substantial intercompany flows between each other and with continental entities. A conservative estimate for total European device intake, accounting for the two distinct UK acquisition funnels plus continental sourcing, would be in the range of 1.0m to 1.5m devices annually. At this scale, PCS sits among the largest European trade-in processors. Both UK strategic reports cite the same factor: "the growth of trade-in schemes." The revenue trajectory of the main trade-in entities maps to the rollout and deepening of these programmes across European markets.

Coöperatief Caveat

PCS Wireless NL Coöperatief U.A., the group's original European wholesale vehicle, has yet to file FY2024 accounts. Based on FY2023 trading patterns (€26.7m Netherlands revenue, €24.1m outside the EU as a standalone entity) and the dramatically expanded intercompany relationship with Excelsior, its FY2024 filing will be important for two reasons. First, it likely contains the external wholesale revenue that represents the true market-facing output of the European operation. Second, the scale of intercompany purchases from Excelsior (implied by the €63.3m receivable) will allow a more precise estimate of how much of Excelsior's €172m represents genuine external sales versus internal transfers. Until that filing appears, probably late 2026 based on prior patterns, the full European revenue picture remains incomplete. Easy reading? Not especially.

Continue reading for:

Transfer pricing mechanics, controlled margins and a combined European profitability floor of €6.5m to €7.0m

The obsolescence question: why 35.8% is a structural outlier and who bears residual value risk in the OEM trade-in chain

Strategic implications including capitalisation benchmarks, repair capability and the TessaB connection to Digital Product Passports

Alternatively, please click here for the article as PDF file.