February Round Up

It's a listing baby, but not as we know it...

The month began with the excellent FDM CCS Insight Circular Markets event which brought together the who’s who in the secondary market universe. The Samsung keynote from Richard Chang strengthened their messaging on secondary market intent [insert applause here], the telco panel highlighted the gap between intent and the competitive reality of too many operators. I've a feeling those GSMA pace-setting targets will be quietly brushed under the carpet. According to one telco, the global leasing companies might end up having everyone's lunch for breakfast and, reading between the lines, in-store mis-grading feels like an employee lawsuit waiting to happen. Other than that, here’s the stuff that may or may not have made it into a full article…

Market

A few days earlier the GSMA released their commissioned report: A Dynamic Framework for the Assessment of Horizontal Mergers1. The timing was deliberate; the Commission is currently consulting on revisions to its Merger Guidelines, and the telecoms industry wants its arguments baked into the new approach. BRG’s Xavier Boutin et al argue that the Commission's current framework is structurally biased towards short term price effects and subjects pro-competitive claims to a far stricter test that merging parties have never successfully met. The authors propose a three step framework that would require the Commission to identify all relevant dimensions of competition (including investment and quality, not just price), assess both pro and anti competitive "theories of competitive effects" symmetrically, and evaluate efficiencies under the same standard as harms. They argue no legislative change is needed; only updated guidance. The telecoms case study is the heart of the document and reads as a methodical post mortem of the Commission’s handling of Three/O2, Orange/MásMóvil and Three/Telefónica Ireland, contrasting these unfavourably with the FCC’s approach to T-Mobile/Sprint and the CMA’s treatment of Vodafone/Three. The core argument is that mobile networks are scale businesses where mergers improve the profitability of investment through larger subscriber bases and combined spectrum holdings, and that the Commission has repeatedly failed to engage with this reality in any quantitative depth. The report is, in essence, the intellectual scaffolding for the industry’s long-running campaign to further consolidate across the European markets, and with the 6G spectrum preamble underway2, a change in guidance couldn’t come soon enough.

Similar effects are likely from the UK Government Department for Science Innovation and Technology (DSIT) draft policy paper catchily entitled: Statement of Strategic Priorities for telecommunications, the management of radio spectrum, and postal services3. Give it a click if you’re really into the political drivers of consolidation, otherwise the DSIT separately published a Mobile Market Review call for evidence on 10 February, open until 21 April, which treats the three-operator UK market as settled and turns its attention to whether the policy and regulatory framework can sustain the investment needed for standalone 5G by 20304. Industry estimates put the cost at up to £34bn, against average annual MNO capex of £2bn between 2020 and 2024. While the review is overwhelmingly network focused, several threads deserve attention from anyone interested in the potential downstream effects. First, DSIT dedicates significant space to eSIM adoption, citing Juniper estimates of 440% growth in travel eSIM users over five years and potential operator revenue losses exceeding $11bn globally. Second, easier switching weakens the contract renewal moment on which carrier distributed device insurance, trade in programmes and managed upgrade cycles have traditionally relied. If consumers can hop providers without changing handset, the incentive structures that feed both protection attachment and the supply of trade in devices back into refurbishment channels begin to loosen. Third, the continued growth of MVNOs and the entry of fintechs like Revolut and Monzo into connectivity products compounds this; these channels rarely operate device lifecycle programmes at anything like the scale of the major MNOs. The document also flags that mobile services were 25% cheaper in real terms in 2024 than in 2019, which, combined with rising capex obligations, may push operators to lean harder into ancillary revenue lines like device financing, insurance and trade in as margin recovery tools, or alternatively to deprioritise them entirely in favour of core network spend. The direct to device satellite partnerships flagged in the review, notably Vodafone's investment in AST SpaceMobile and VMO2's tie up with Starlink, perhaps imply that D2D-capable hardware could become a catalyst for upgrade cycles, with knock on effects for the volume and vintage of devices entering the secondary market.

Notably absent from the entire document is any mention of repair, refurbishment, circular economy obligations or device sustainability. For a strategic review of a market in which circularity is an increasingly important growth vector, employer and solution to some of the UK’s WEEE problem, the omission is striking. Perhaps the responsibility is being left to the practically invisible 18-person Circular Economy Taskforce Committee and their delayed (early 2026) Circular Economy Strategy. Obviously they didn’t mean too early in 2026 especially now the committee Chair and Deputy Chair’s times are already up5. F.F.S.

Hop across the North Sea however, and despite all that nasty European legislation, it appears Germany has managed to publish its draft transposition of the EU Right to Repair Directive, with rules applying from 31 July 20266. Smartphone and tablet manufacturers will be legally obliged to repair defective products on consumer request even after the two year warranty has expired, free of charge or at a reasonable price within a reasonable time. The obligation lasts as long as ecodesign rules require spare parts availability; for smartphones, that means batteries, display assemblies and speakers for a minimum of seven years from when the model ceases production7. Consumers who choose repair over replacement during warranty get a one year extension. Critically, manufacturers are prohibited from using software or technical protection measures that hinder repair, including by independent third parties, and cannot mandate the use of original spare parts. They must also supply parts and tools at a reasonable price. For the device protection and repair market, the combined effect is substantial: this is not just a right to ask for repair, it is a legal framework designed to keep independent and third party repair viable across the device's useful life.

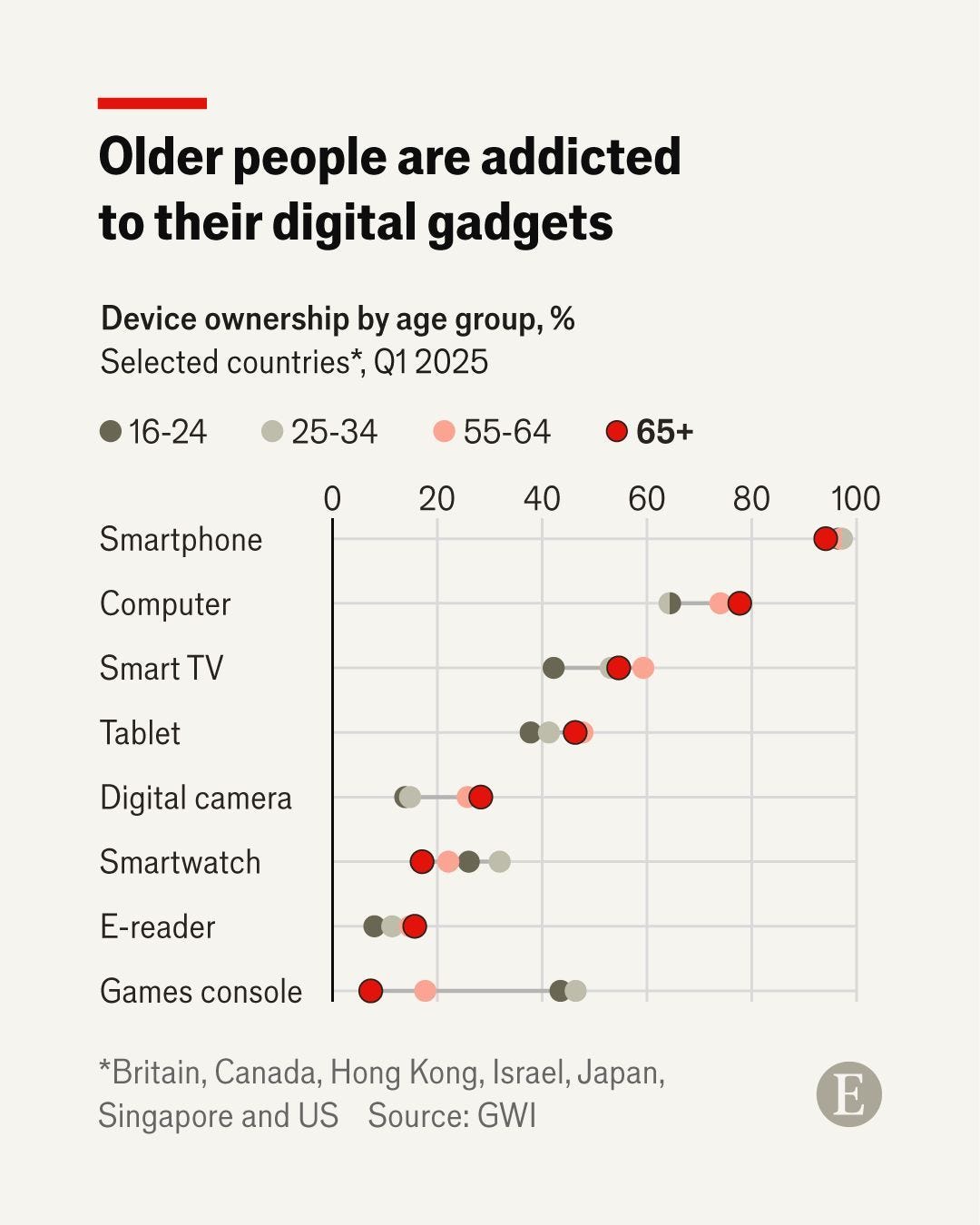

I wasn’t getting quite enough out of my Economist subscription to renew it, but just before it ended, I came across an article highlighting that smartphone ownership might be more tightly packed across the age range brackets than previously thought8. No longer can we aim our outrage at Gen-Z or Gen-Alpha for being glued to their phone screens. Increasingly we are to be outraged at the outraged as the 65 plussers tap in their Wordle guesses at the local National Trust cafe. Adjust your marketing accordingly.

I’m always keen to read about and promote organisations, especially not-for-profits, working to advance the sector. Material Focus is one such organisation, "on a mission to stop the valuable, critical and finite materials inside electricals from going to waste”', funded by the UK’s Extended Producer Responsibility regulations. They offer insight and occasionally funding. If you didn’t know about them, you might well be paying for them, so worth a look.

Companies

First up, congratulations to Closing The Loop on reaching eight million collections through their one-for-one partner programme9. It’s a significant milestone for the firm and behind the numbers, the real-world impacts are perhaps even more important:

440 tonnes of e-waste not ending up in landfills and responsibly managed

95% of the valuable metals and raw materials recovered and returned in the value chain

an estimated 19,500 living wages created within collection networks

safer working conditions and stable income for hundreds of collectors

All of them fantastic achievements in their own right demonstrating the impact of sustainability operating at scale. Good stuff.

Despite my temporary annoyance every time I go to pick up French company accounts, congratulations also to Back Market for closing their 2025 with over $3.5bn in global GMV, representing 32% year on year growth10. The company also delivered its largest Black Friday in history with 41% year on year growth during the period. Growth was driven by repeat purchasing and category expansion beyond smartphones into laptops, tablets, gaming consoles and audio. At an estimated average selling price of $330 and industry-standard marketplace commissions, that implies roughly 10.6 million transactions and platform revenue in the region of $500m. In France, their first and most mature market, the business delivered 35% EBITDA margins. Separately, the company has reached EBITDA break-even at the global level, which implies that the profitable European operation is currently funding US market entry. Core US test markets grew more than 40 percentage points faster than the company average in 2025. Non-smartphone categories now represent roughly 40% of US GMV, and nearly 50% of Gen Z consumers say their next smartphone will be refurbished. According to Joy Howard, Back Market's CMO, replacement lifecycles are extending as devices increasingly function as access points to cloud-delivered intelligence rather than standalone performance machines. I'm still trying to decipher whether that's a genuine structural thesis or marketing poetry.

CECONOMY's Q1 2025/26 results (October to December) revealed that refurbished product sales across its MediaMarktSaturn network increased nearly fivefold year on year to 205,000 units, a data point the company chose to surface exclusively in its investor presentation rather than the press release or statutory quarterly report11. The volume growth is genuinely striking and signals that Europe's largest consumer electronics retailer is embedding secondary devices into its omnichannel model rather than treating them as a peripheral experiment. That said, 205,000 units against €7.6bn in quarterly group sales remains a rounding error in revenue terms; even at generous ASP assumptions, refurbished likely accounts for around 1% of turnover. The fivefold increase tells you more about how small the base was than how large the business has become. CECONOMY is clearly positioning refurbished alongside Retail Media (+85% income growth) and Services & Solutions (+13.7%) as proof points for its margin diversification strategy, and the direction of travel matters, but the destination is still a long way off.

The Best Buy deal has done some heavy lifting, driving Assurant's Connected Living segment to deliver 12% revenue growth in FY2025, reaching $5.4 billion and breaking out of four years of effective stagnation12. However, Adjusted EBITDA of $506m grew just 3.7%, compressing margins from 11.0% in FY2022/23 to 9.4%. The disconnect is more striking when set against the operational backdrop: devices serviced through trade-in and upgrade programmes have declined 21% over three years to 22.7 million units, even as carrier partners reported record handset sales. Revenue is accelerating, earnings are barely keeping pace, and device volumes are moving in the opposite direction. It’s a shame the results came out a week after the Circular Markets event, otherwise we could have probed their Connected Living chief with a question that that didn’t involve an AI-stack answer. In-depth downloadable report available here.

Samsung announced a significant expansion of its Care+ device protection service across 17 European markets, effective 19 January 202613. The enhanced offering now includes unlimited accidental damage repairs, 175 walk-in repair locations, coverage while travelling abroad (with the previous 60 day trip limit removed), and a free battery replacement when capacity drops below 80% after the standard warranty expires. Customers can opt for monthly rolling payments for up to 60 months with the freedom to cancel at any time, or a two year upfront plan. Optional theft and loss coverage is also available, with replacement devices dispatched within 48 hours and Samsung Knox Guard used to remotely block missing devices. The service, which covers phones, tablets, wearables and PCs, is underwritten by AmTrust Specialty Limited and administered by bolttech Device Protection (Ireland) Limited. That’s a win from Assurant I think.

It’s not all bad news for Assurant’s European team though. They did launch a net new mobile insurance plan with Chase in the UK14. Chase Protect offers the usual bank bundle of worldwide travel insurance, mobile phone insurance, and Breakdown Cover, available at a fixed monthly rate of £12.50. The mobile insurance cover protects you, your partner or spouse, and all children (under the age of 18, or under 24 if in full time education) living at your home address against loss, theft, damage and technical faults, up to £2,000 per claim for repair or replacement, replacement of accessories up to a value of £250 and there’s up to 4 approved claims in any 12-month period. Standard fayre. According to the release, Chase serves over two millions customers in the UK (not sure if they are all current account customers) which at a 4%-6% attachment rate, means the programme could get to 80k-120k subs. Big swings, mini-roundabouts.

Raylo Group Limited filed its FY2025 accounts (year ended 30 September 2025) and the numbers were pretty decent. Revenue grew 49% to £41.5m, billing subscriptions jumped 63% to 151,056 and, most notably, the group posted its first statutory operating profit at £1.5m, a meaningful swing from the prior year’s £1.1m operating loss. EBITDA nearly doubled to £10.9m at a 26% margin, whilst gross margins ticked up to 77% from 74%. The existing customer book continues to do the work, generating £12.2m in operating profit before £10.9m of new customer acquisition investment dragged the consolidated number back down. ARR hit £48.4m, representing 17% forward momentum over statutory revenue, which suggests next year’s top line has another decent step up baked in. The loss for the year narrowed to £3.8m from £5.4m, although still weighed down by £5.3m in financing costs which remind you this remains a capital hungry model despite the “subscription infrastructure” platform messaging. Still, for a business that was EBITDA negative just two years ago, the trajectory is difficult to fault. In-depth downloadable report available here.

Foxway released their Q4 2025 year end report15, and the headline numbers were strong: net sales of SEK 2,129.3m (€183.6m) grew 22.9% in constant currency with adjusted operational EBITDA up 43% to SEK 124.5m (€10.7m). The real story, again, is the segment divergence underneath. Recommerce C&E, the weakest segment just twelve months ago, delivered 245% EBITDA growth on the back of AI driven enterprise equipment demand, while Recommerce Mobile, previously the profitability engine, saw margins decline from 12.6% to 4.5% as management deliberately discounted to clear inventory. CWS showed Q4 recovery but also absorbed a SEK 350.4m (€30.2m) goodwill impairment, signalling a downward rebasing of medium term expectations for the segment. Full year operating cash flow evaporated to SEK 1.0m from SEK 292.1m, and alternative net debt rose 20% to SEK 2,172.0m (€187.2m). I will publish a full analysis on Friday.

Investments

Either there’s been very little activity, or I’ve managed to miss the hot deals in our part of the Circular Economy last month. The highlight appears to be the news that bolttech are in talks to acquire MoneyHero16. The Singapore headquartered, NASDAQ listed personal finance aggregation platform provides services for credit cards, personal loans, mortgages, wealth, insurance, and other financial products connecting the providers of these products with matched and ready-to-transact consumers. The thesis eludes me, other than both companies have some common backing via Richard Li’s Pacific Century Group. Oh, hold on… Bolttech, valued at $2.1 billion after last year's Series C, considered and shelved a US IPO two years ago. MoneyHero is already NASDAQ listed with a market cap of $60 million. Acquiring MoneyHero hands Bolttech a public listing without the inconvenience of an IPO process, which would require the sort of financial transparency that lets the market, rather than a private funding round, determine what the company is actually worth. A reverse takeover is a far stronger thesis than the strategic case for grafting a consumer comparison site onto a B2B2C exchange whose entire model depends on not competing with its distribution partners. Smarts.

Peace,

sb.

When I last reviewed the legislation the time period was constrained by when the last product was placed on the market. Things may have moved on, or there’s a translation issue. The difference would be subtle, but “ceased production” is perhaps slightly easier to manage.