Market Analysis: European CE Recommerce

The boards didn't get any longer, but they're all still paddling...

This report covers eleven operators with estimated aggregate specialist revenue of approximately €1.14bn | no integrated operator with filed FY2024 accounts delivered a profitable year | net losses range from €4.1m at Flip.ro to €24.0m at Swappie, and Rebuy, the only operator to have posted a positive operating result in FY2023, reversed to a net loss of €4.75m. Flip.ro is the dataset's standout: FY2024 revenue of €78.9m grew 53.9% year on year with the net loss ratio compressing from 11.4% in FY2022 to 5.2% in FY2024, the most compelling financial trajectory in the report. Post-period, Refurbed announced EBITDA profitability and raised €50m | confirming the marketplace model is sound once the cost base is aligned. Back Market, Recommerce and Certideal file no statutory accounts; their aggregate estimated revenue exceeds €400m and the French transparency pattern shows no sign of changing. Back Market's last disclosed valuation of $5.7bn was set at the January 2022 Series E raise; no further funding round has been announced and no statutory accounts exist against which to assess it. Full analysis available as a downloadable report at reports.finsur.co.uk.

In February last year, I published the European Marketplace Research Update covering the major secondary marketplace and integrated-model operators across Europe. My general opinion at the time was that operators needed to keep paddling or buy a bigger board in order to continue surfing the secondary wave. Now just over a year on, and given the continuing and increasing focus on the sector, it’s time for a refresh. This version anchors on the FY2024 filed accounts and combines recently published developments to offer a clear view of performance and trajectory.

If you’re looking at the European CE recommerce sector from an investment or strategic standpoint, this is the most complete evidence base currently available in one place. In addition to asgoodasnew, MusicMagpie (now part of AO World), Rebuy, Refurbed and Swappie, I’m pleased to be able to add Flip to the roster who provide significant coverage of Central & Eastern European markets. Whilst the transparency divide between France and everywhere else remains as wide as ever, the report makes best use of the financial data that has been made available to provide the widest possible coverage.

Orientation

Operators

This report features eleven operators, across three distinct categories: six with filed FY2024 accounts: asgoodasnew, Flip.ro, MusicMagpie, Rebuy and Refurbed and Swappie; three where disclosure is absent or limited to self-reported figures: Back Market, Certideal and Recommerce; and two platform companies that set gravitational context without being directly comparable: Amazon (Renewed) and eBay.

Of course, the European consumer electronics recommerce sector is considerably wider than the operators covered in this edition. UK-focused operators such as Reboxed and iOutlet, along with a range of other national companies are outside the scope for now on the basis of their size or regional significance.

Business Models

The primary business model distinction in this sector is “marketplace” operators versus “integrated” operators. Marketplace operators like Back Market and Refurbed earn commissions on the transactions between sellers and buyers. Their revenue is typically a take rate of approximately 10-11% applied to a Gross Merchandise Value (GMV). Integrated operators like Rebuy and Flip.ro buy devices wholesale or directly from consumers, refurbish them and sell them directly.

The secondary distinction is between specialist operators and platform generalists. eBay and Amazon list refurbished consumer electronics alongside every other product category, although they may run dedicated quality programmes, like Amazon Renewed, designed to improve the customer experience. Some specialists, like MusicMagpie also receive income from product categories like media.

The Transparency Divide

The final orientation point of note is the availability and granularity of filed accounts. Amazon and eBay accounts don’t provide the level of segmental reporting in their accounts to determine secondary market sales for consumer electronics which is perhaps understandable given their size. Equally understandable, but less acceptable is the habitual certificate of non-filing lodged by all of the French companies operating in this space: Back Market, Recommerce and Certideal all adopt the same approach of not filing annual accounts which, for a country operating at the forefront of secondary trends, is hardly setting the right example.

Marketplace Operators

Back Market

Back Market reported that 2025 global GMV hit €3.5bn, representing 32% YoY growth and announced global EBITDA profitability, with approximately 35% EBITDA margins reported in the home French market12. Of course, this tells nothing of net profitability, or the group position, and given that the US market became the second-largest market by GMV, and Austria, Italy and Portugal all reported triple-digit GMV growth in Q2 2025, they must still be investing heavily. The marketplace now operates across 18 different markets with approximately 17 million customers worldwide3.

Back Market’s growth has recently extended beyond market development. They launched a repair platform in France, Germany and Spain available to both customers and non-customers on a one-off or subscription basis4. More recently Back Market and Google have launched a programme where Back Market sells low‑cost ChromeOS Flex USB sticks you can plug into an old laptop to replace the existing OS with ChromeOS Flex, effectively “restarting” the device’s useful life rather than junking it5.

Additionally, Back Market’s B2B operation is growing with nearly 6,000 company customers in France and 250 in the US as at Q2 2025, reportedly doubling in the year. They have launched partnerships with Bouygues Telecom in France and Visible by Verizon in the US to add distribution reach beyond the marketplace.

Since the $510m Series E raise in January 2022, valuing the business at an eye watering $5.7bn, no further funding has been announced6. However, the reported EBITDA profitability would reduce any near-term pressure for external capital, though no balance sheet or cash position has been disclosed which could verify this. Unusual for a 35% EBITDA, €3.5bn GMV organisation, but not unfortunately unique.

Refurbed

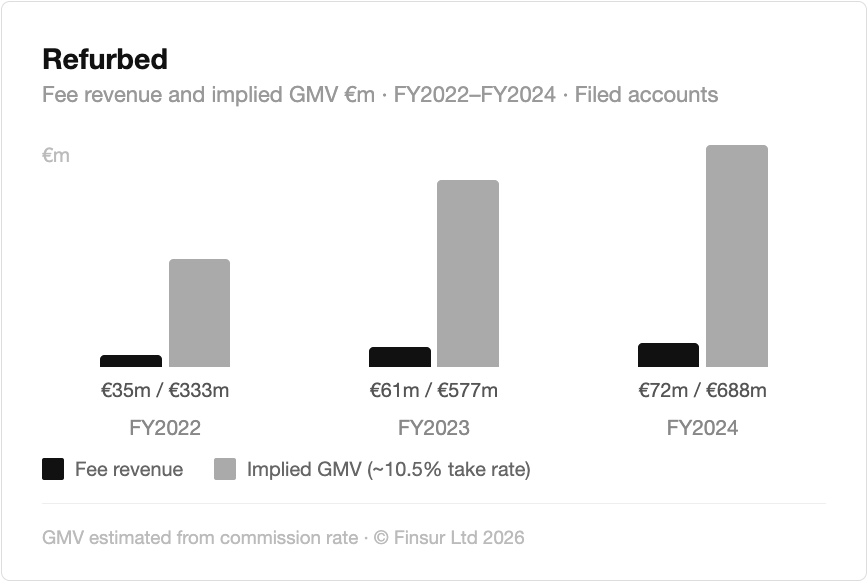

Refurbed is the only pure marketplace operator in this report that files audited accounts posting FY2024 revenue of €72.3m (FY23: €61.0m, +19%), solid growth which, at an estimated 10.5% average commission rate, would imply a GMV of €688m. However, top-line momentum was not the issue. FY2024 operating loss widened slightly to €19.4m (FY23: €18.6m) and net loss also widened to €19.8m (FY23: €19.3m).

Marketing and operational expenses rose to €49.3m (FY23: €35.9m), generating an estimated incremental marketing ROI of 0.87x: Refurbed spent approximately €13.4m to acquire an additional €11.7m of revenue and widen the loss by €0.8m. This was the central problem that stood out in the filed accounts.

Total people costs of €28.2m included contracted personnel representing 47.5% of the total, with cash of €6.65m and an estimated €12-13m of Series C funding remaining undeployed at year end. Intervention was necessary and management had structured the cost base with flexibility and retained sufficient runway to act.

Post period, the picture changed materially with a c.20% workforce reduction early in 2025 followed by a profitability announcement in June7, and a €50m capital raise in October8 with funds targeted for further geographic expansion, including the now live UK site. By March 2026, multiple sources reported that Refurbed had crossed €3bn in cumulative GMV, less than a year after passing €2bn, implying annualised growth in excess of 40%. For a business that filed a €19.8m net loss in FY2024, the FY2025 trajectory is some story.

With Back Market’s continued financial opacity, Refurbed offers the only available insight into the GMV threshold required for marketplace profitability and €688m in FY2024 wasn’t it. The speed of the post-period reversal, from widening losses to double-digit EBITDA profitability within two reporting periods, suggests that the cost base was the problem rather than the model. The workforce reduction provided a catalyst, the €50m raise with new institutional investors alongside the existing shareholders confirmed conviction in the underlying economics rather than rescue financing.

The strategic decision to enter the UK market is an interesting one. The UK is one of Europe’s deepest and most competitive recommerce markets, and Refurbed’s entry, backed by fresh capital and an already operational site covering 24 markets across 486 million consumers, with premium brands representing 90% of platform GMV9, raises the competitive stakes further for every operator with UK exposure.

The full analysis of Refurbed’s marketplace economics, capital structure, and the margin between filed losses and stated profitability is covered in the Finsur Refurbed FY2024 report.

Continue reading for:

Filed accounts analysis across six integrated operators including asgoodasnew, Flip.ro, MusicMagpie, Rebuy and Swappie, with gross margin, net result and employee efficiency data where disclosed

The Comparative View: a fully populated cross-operator data table covering revenue, profitability, inventory, headcount and investment stage across all eleven operators in this report

Strategic Outlook: where the sector goes from here, including the profitability frontier, the consolidation precedent and the geographic opportunity that Western European operators have largely ignored

Alternatively, a PDF version of this report is available to purchase here.