Company Analysis: Raylo Group Limited FY2025

Seven for a profit, never to be sold...

Key Findings

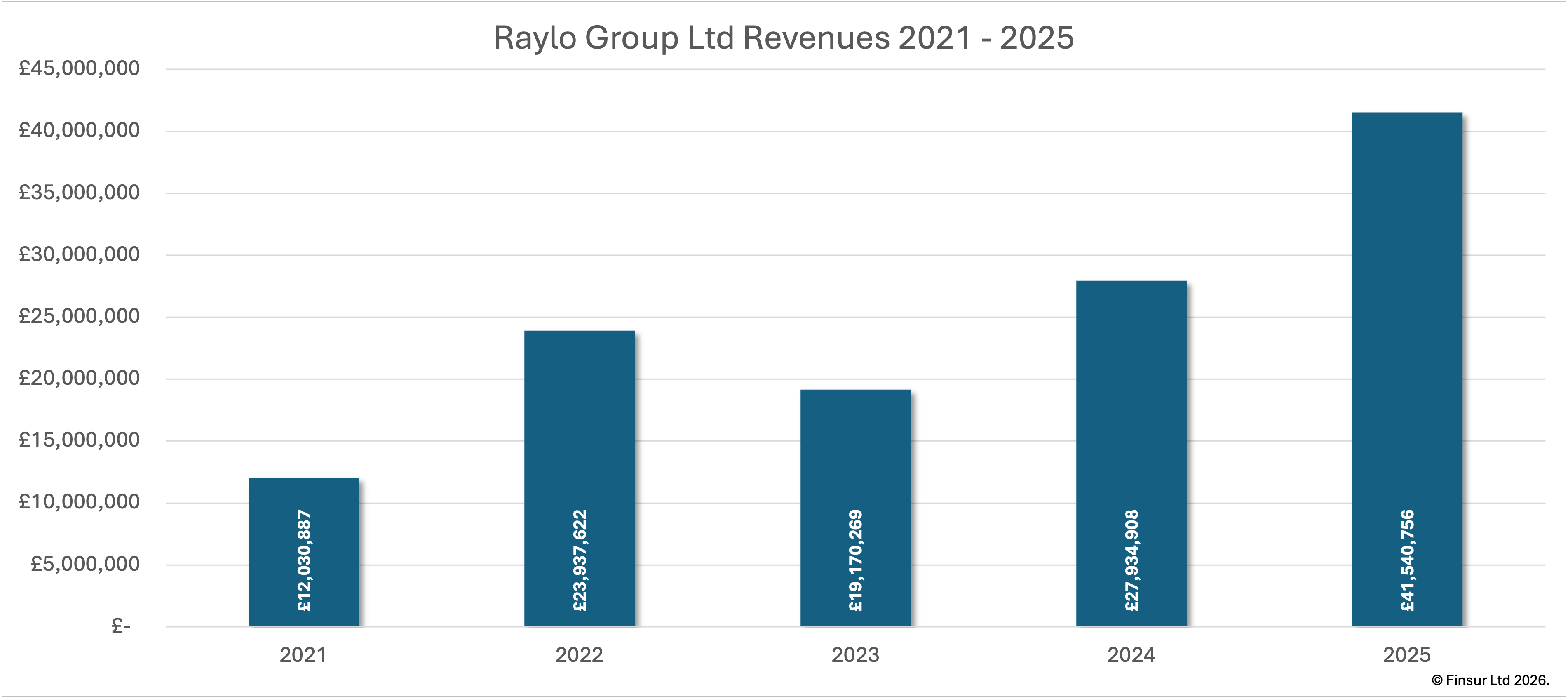

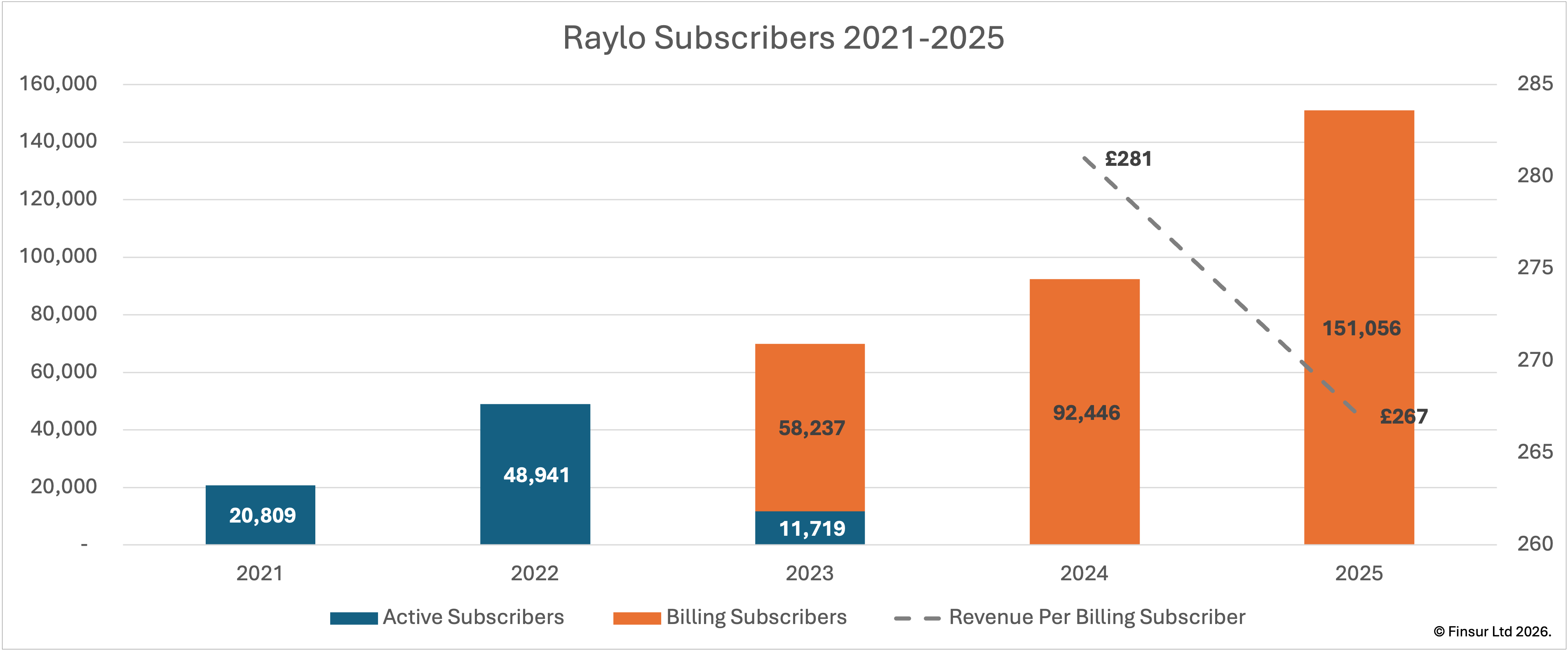

Raylo delivered its first statutory operating profit of £1.5m in FY2025, a milestone that validates the subscription rental model after seven years of development. Revenue grew 49% to £41.5m | Billing subscriptions increased 63% to 151,056 | EBITDA nearly doubled to £10.9m at 26% margin | ARR reached £48.4m with £6.9m forward momentum over statutory revenue. A £30m fundraise led by Citi, comprising £10m equity and £20m NatWest debt, valued the business at £150m post-money. The share structure was comprehensively reset in December 2025, establishing a new liquidation waterfall that promotes institutional investors above earlier backers. The original Finsur break even model predicted profitability at 133,000 subscribers; it likely arrived somewhere between 120,000 and 130,000. Close enough.

In a particularly English turn of events, I’ve noticed myself saluting ever more magpies over the last few years. To anyone less superstitious, the sight of me shuffling along the local trails witnessing a raised hand to brow without a receiving officer anywhere to be seen, is odd, possibly. But superstition aside, the reason behind my increasingly frequent martial tick is entirely related to an increase in annual mileage combined with an increase in the magpie population, which has been on a distinctly upward trend since 20161. To coin a favourite phrase, the harder I practice, the luckier I get. After Raylo’s 2025 accounts dropped last week, it appears management subscribe to a similar code of practice.

Recap

This is the third Finsur report2 on “the subscription platform for the world's leading electronics brands.”, so just a quick reminder of their model: no upfront fees, monthly subscription, device lifecycle management, circular economy ethos, founded 2018. The original model took shape as a B2C website offering electronic device rentals directly to consumers. However, since 2021, management have evolved the proposition to include RayloPay and have brought device subscription capability to other brands including Apple, PlayStation, Google, Dyson and Lenovo3. The latest OEM partnership, announced at the beginning of this month, powers LG’s premium device portfolio rentals including selected TVs, soundbars and monitors4.

Raylo is now well positioned as a “subscription infrastructure” business and confirmed the capability stack in their latest filing:

Credit and fraud underwriting using proprietary Xylo-AI risk models

Wholesale funding to support financing of device subscriptions

End-to-end device lifecycle management using their proprietary Nexus platform

At the end of January this year, alongside the LG partnership, Raylo announced a £30m fundraise, with £10m in equity led by Citi and another £20m in debt from Natwest. That’s genuinely positive, but for a business able to demonstrate a clear path from device rental to subscription infrastructure, the post-money valuation of £150m5 caught me a little on the hop. So let’s have a look…

Performance

Key Performance Indicators

- Revenue: £41.5m (FY2024: £27.9m, +48.7%)

- Billing Subscriptions: 151,056 (FY2024: 92,446, +63.4%)

- ARR: £48.4m (FY2024: £30.4m, +59.1%)

- Gross Profit: £32.2m at 77% margin (FY2024: £20.6m at 74%)

- EBITDA: £10.9m at 26% margin (FY2024: £5.7m at 20%)

- Operating Profit: £1.5m (FY2024: operating loss £1.2m)

- Annual Billing per Subscriber: £267 (FY2024: £281)

- Existing Customer Net Income: £6.9m

- New Customer Acquisition Investment: £10.9m

- Subscriber Acquisition Cost: £186 (FY2024: £202)

- Net Debt: £62.2m (FY2024: £38.2m)

Management were very likely pleased with top-line performance as the business continued to deliver substantial revenue growth hitting £41.5m up 48.7% YoY (FY2024: £27.9m) which, since revenue was first disclosed for FY2021 is a 36.3% CAGR. Even better, the core subscription engine is growing faster than the top-line suggests. Management’s revenue disclosures reveal the growth quality as consumer hire agreements increased 55.1% to £40.3m (FY2024: £26.0m). Asset sale income actually fell 36.2% to £1.3m (FY2024: £2.0m). Fewer asset sales implies fewer devices reaching end-of-life disposal, which would be consistent with a faster-growing portfolio still on early subscription terms.

With third-party channel distribution enabled, FY2025 billing subscriptions increased 63.4% to 151,056 (FY2024: 92,446), that’s almost 59,000 net new subscribers in a single year and by the end of the year, annual recurring revenue (ARR) had improved to £48.4m (FY2024: £30.4m, +59.1%). The gap between ARR and statutory revenue widened to £6.9m (FY2024: £2.5m), implying second half acceleration and a strong exit run rate heading into FY2026.

As you might expect, the introduction of B2B2C channels, with a wider asset variety, has impacted the annual billing per subscriber. Although the importance of this metric declines a little without having the channel splits. Still, it’s an interesting data point which dropped £14 from £281 in FY2024 to £267 in FY2025. Additional partnerships are likely to drag this further downwards as the channel mix rebalances away from B2C sales.

Continue reading for:

How Raylo’s first statutory operating profit was delivered whilst simultaneously investing £10.9m in new customer acquisition

Why Citi’s entry triggered a complete share restructure and what the new liquidation waterfall means for existing investors

At a £150m valuation, is Raylo a finance company with platform ambitions or a platform business that happens to finance devices?

Alternatively, you can download the full article as a pdf file here.