Company Analysis: Swappie FY2024

Suomi-things Still to Work On...

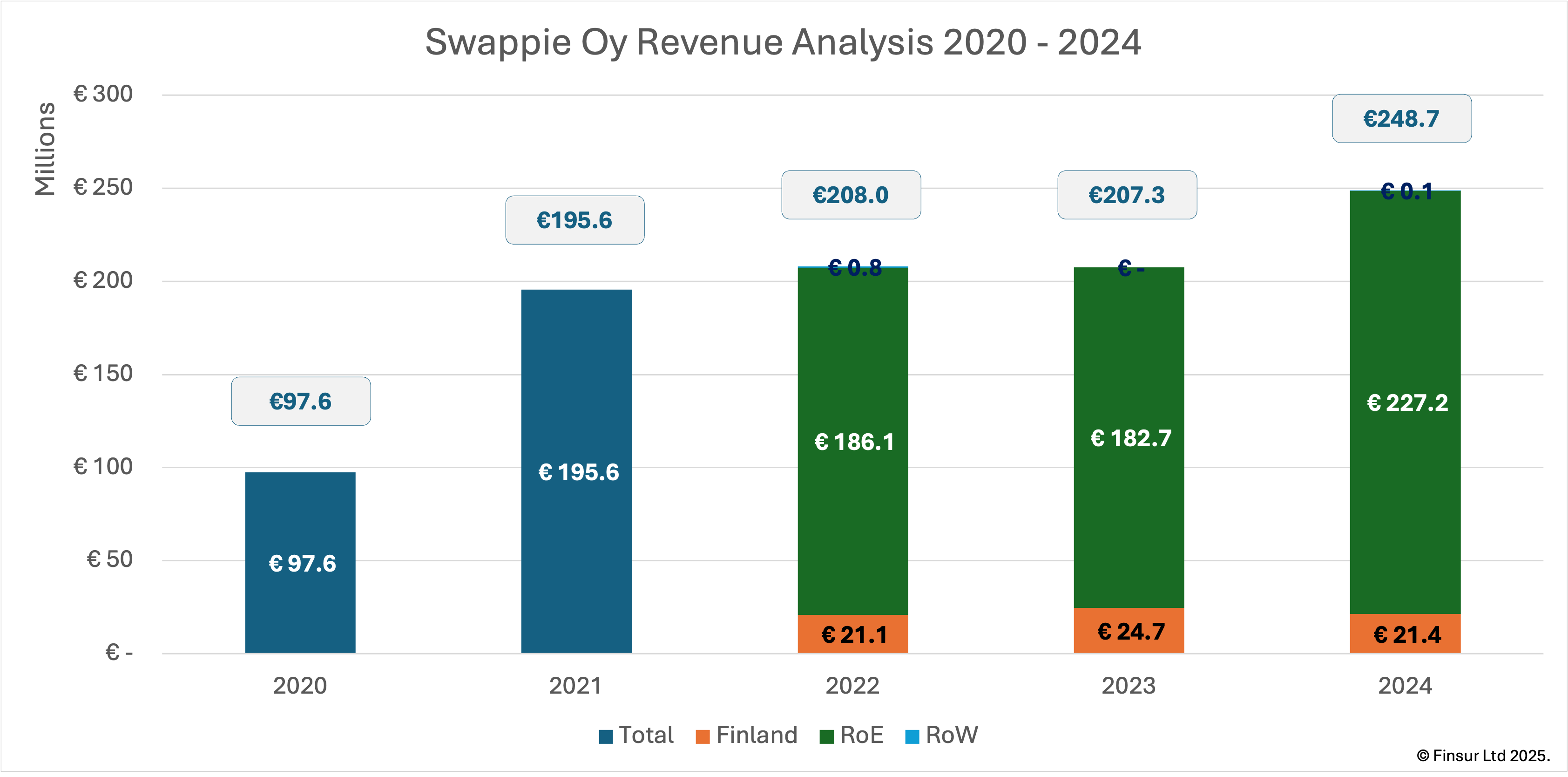

Key findings: FY2024 revenue €248.7m (+20.0% YoY) | Rest of Europe +24.3% to €227.2m, offsetting 13.1% home market decline | Gross profit €50.4m at 20.3% margin, improved 0.4pp YoY | Operating loss €(20.5)m at -8.3% margin (FY2023: -9.5%) | Net loss €(24.0)m at -9.7% | September 2024 capital restructure and CEO transition completed | Series C raised approximately $124m; implied valuation $496m to $744m assessed against the path to profitability | Full analysis available as a downloadable report at reports.finsur.co.uk.

Being firmly in the barbigerous camp for more years than my better half cares to remember, I had absolutely no interest in the Viking Shave Club. Swappie, on the other hand, is one of the other companies founded by serial entrepreneurs Sami Marttinen and Jiri Heinonen and has turned out to be one of the largest and most important European device marketplaces deserving far more attention. I covered them in the broader European Marketplaces1 article back in February this year and now that I’ve finally got around the grabbing myself a copy of the FY2024 filing, it’s time for a look under the konepelti.

Recap

Swappie, so the story goes, was founded in 2016 after Marttinen fell victim to fraud when buying a used iPhone online. In Finland? Well, despite my belief that no true Finn could commit such a crime, Swappie was born out of an existing entity, Digilean Nordic Oy, which the pair were using for start up ideas. Almost 10 years later their ambition of a circular economy has driven Swappie to operate across 24 European markets and the US (although I’m not sure that’s operational at the time of writing).

The expansion has been in part funded by three rounds of equity totalling approximately $170m and a more recent $18.4m loan from the European Investment Bank in 2024. Series A, three years after the business was founded, raised $5.6m from Inventure, Lifeline Ventures and Reaktor Ventures, all of whom have continued to participate in subsequent rounds. Series B, facilitated by Arma Partners a year later raised $40.6m and added the Finnish state-owned Tesi to the cap table. Series C came along with a significant $124m raised, although public disclosures of valuation are a bit thin on the ground. I’ll come back to that.

In September 2023, Swappie centralised all inventory and sales activity within the Finnish parent company. The subsidiaries in Estonia and Germany transitioned from independent trading entities into pure fulfilment and refurbishment service providers, with management describing the Estonian operation as becoming “a phone improvement service subcontractor to parent Swappie Oy”. The restructuring altered the Group’s working capital dynamics and risk allocation ahead of the FY2024 period under review. I’ll come back to that too.

After a long association as an investor and board observer, Jussi Lystimäki came on board as the new CEO in June 2025 packing a stellar marketplace CV and hired to lead the next phase of growth and circular innovation. For those of you unfamiliar, one notable feature is that that Swappie stick firmly to Apple kit. If you’re looking for anything other than an iPhone or an iPad, look elsewhere. Let’s see how that’s working out for them…

Performance

FY2024 Key Metrics:

- Revenue: €248.7m (FY2023: €207.3m, +20.0%)

- Gross Profit: €50.4m at 20.3% margin (FY2023: €41.3m at 19.9%)

- Operating Loss: €(20.5)m at -8.3% margin (FY2023: €(19.7)m at -9.5%)

- Net Loss: €(24.0)m at -9.7% margin (FY2023: €(21.6)m at -10.4%)

- Cash: €12.8m (FY2023: €14.4m)

- Employees: 777 generating €320k revenue per head (FY2023: 818 at €253k)

Source: Swappie Oy (3026755-2) filed accounts for year ending 31 December 2024

Back in February, I wondered if the 2023 marketing expenses reduction, as a part of the broader cost savings, would limit revenue progression in the current competitive environment. Well, it turns out I’ll never know because the 20.0% increase in FY2024 revenue to €248.7m (FY2023: €207.3m) was, according to the filing, primarily driven by increased marketing investments. I’m assuming this was in response to the competitive environment becoming, well, even more competitive last year. Regardless, I’m sure the additional €41.4m sales was very welcome. Whether it came at an acceptable cost or not, is a question for the profitability section.

Behind the improved top line, Swappie’s home game declined 13.1% with sales dropping to €21.4m (FY2023: €24.7m). However, there was no such problem with their away performance. The Rest of Europe sales improved 24.3% year-on-year to €227.2m (FY2023: €182.7m), more than offsetting the drop in sales in Finland. Whilst it’s not material, one aspect of income I’m unable to pin down is the remaining revenue from “Outside Europe” amounting to €100k. Despite the Swappie website listing the US as an operating entity, there appears to be no stock available (at least at the time of writing) in that market. FY2023 saw €336k in revenue from China via the Estonian subsidiary, which suggests some wholesale disposal going on in non-operating markets.

In addition to the geographic analysis, management helpfully offer some revenue category analysis and despite the services category being immaterial, it is growing. As you’d expect, product sales make up the vast majority of revenue with FY2024’s €246.6m representing 99% of the business (FY2023: €206.0m) showing 19.7% growth over the year. Services in FY2024 at €2.1m or 0.8% of revenues (FY2023: €1.3m 0.6%) grew 57.6% in FY2024 and is worth an explanation.

I am assuming the majority, if not all of the services revenue is generated by “Swappie Care”, a device upgrade subscription service that allows customers to exchange their Swappie purchased iPhone for a new device from the online store. Subscribers pay a monthly or annual fee based on their original phone’s purchase price. Key features include: a discount code worth 90% of the current equivalent phone’s price (capped at original purchase price); ability to upgrade twice within any 12-month period; automatic subscription transfer to the upgraded device; and a maximum subscription term of five years. The service effectively functions as both device protection and a regular upgrade programme, enabling customers to refresh their hardware whilst feeding returned devices back into Swappie’s refurbishment inventory. As with any assumption, there’s likely to be more questions raised, and the accounting treatment has me curious. I’ll come back to that.

Making some assumptions on unit economics, Swappie’s inventory is all Apple so the usual secondary market ASP is going to be a little low. Taking a €400 ASP results in FY2024 sales volume of approximately 617,000 devices. Using the same ASP for last year suggests an uplift of just over 100,000 devices in the year. Usual caveats apply, including the fact these estimates don’t account for product iPhone/iPad product mix.

Continue reading for:

Complete Profitability Analysis

Balance Sheet & Cashflow Assessment, including more on Swappie Care

Strategic Analysis

Also available as a standalone pdf report here.