November Round Up

Trade-ins, trade-offs and Foxway even bagged a Tre-Sverige...

I’ve been finalising a client project this last month, researching multiple household names in consumer electronics. I have to say that by and large from the consumer perspective, the general standard of manufacturer after-sales processes for non-mobile categories is shit. They range from sprawling and confused approved or unofficial service networks that may or may not appear on support pages supposedly there to help you locate your nearest dealer, to replacement only options that don’t give a second thought to repair, let alone self-repair, and certified refurbished? Well, that’s almost a non-starter. For some manufacturers, the scale of the problem is clearly enormous and for others, perhaps the economics of repair just don’t add up and who knows which landfill returns are ending up in. In the consumer space, the phone, tablet and laptop secondary markets are admittedly imperfect, but many readers of this substack are actively working on improving the sector and are streets ahead of other consumer electronic asset classes. You should all pause for a second and have a well deserved pat on the back. Right, back to work. Quite a few companies released Q3 results in the last month, so I hope the longer than usual update gives you something to get your teeth into…

Markets

OK, so the latest Secretary of State for Environment, Food and Rural Affairs may not have had their feet under the table for too long, but any background on why there’s a delay to the UK Circular Economy Strategy was severely lacking in the latest EFRA Committee hearing1. Anyway, apparently it’s now known as the Circular Economy Growth Plan and won’t be arriving for consultation until 2026. Perhaps the size of the committee has something to do with it2. The introduction of Packaging Extended Producer Responsibility legislation3, Deposit Return Schemes4 and Simpler Recycling5 are all welcome but, if the Circular Economy is a real priority, the committee needs to evidence some output, which now includes Consumer Electronics Reuse and Waste6.

More from the UK government. This time the Competition and Markets Authority are stepping into, or rather stepping on, some dubious online selling practices7. Remember the days when you could sign up for an insurance policy or two without even knowing about it, keep paying the premium for 10-years, stick in a miss-selling claim and spaff the proceeds on two weeks in Benidorm? Well, thankfully those days are gone, and opaque opt-in or opt-out language should have been a thing of the past too. However, among the 8 firms into which the CMA have opened investigations, are two electrical retailers: Marks Electrical in relation to default opt-ins and; Appliances Direct in relation to time-limited sales and default opt-ins. The CMA are clear that they have come to “no conclusions about whether the law has been broken in any of these investigations” and I am sure it’s all one big misunderstanding.

According to a post from Varun Mishra at Counterpoint Research8, Apple has broken into the top 5 smart phone brands in India by market share. This is a significant milestone in a country that spawned plenty of home grown budget manufacturers and became addicted to anything that was born out of BBK Electronics. Apple’s 9% market share, which has grown alongside Vivo and iQOO, cements India as their third-largest market. Oppo maintained share whilst Samsung, OnePlus, Xiaomi and POCO all lost ground.

The US customer is a strange beast and for years, their willingness to be sold to has confounded my natural scepticism. But, after me chirping on about lengthening device lifecycles in the UK and Europe, perhaps change is afoot across the pond. According to CIRP9 as reported by Pieter Waasdorp over at SecondaryNews10, in the twelve months ended September 2025, 42% of US buyers replacing an Apple iPhone replaced a device that was older than three years. That’s up sharply from 32% in 2024 and 24% in 2019. So maybe longer ownership cycles are accelerating in the US after all with hardware and durability enhancements, software longevity and value being cited as possible drivers. Whilst it’s only one data point, it’s certainly one to watch. Even keeping your phone a few months longer would have significant revenue implications in the world’s largest iPhone market.

Companies

I was planning to include AO World’s interim half-yearly results in this section, however, their Switch24 iPhone upgrade product, with its novel approach to separately financing the depreciation and the residual value, warranted deeper investigation, so there’s a full article here.

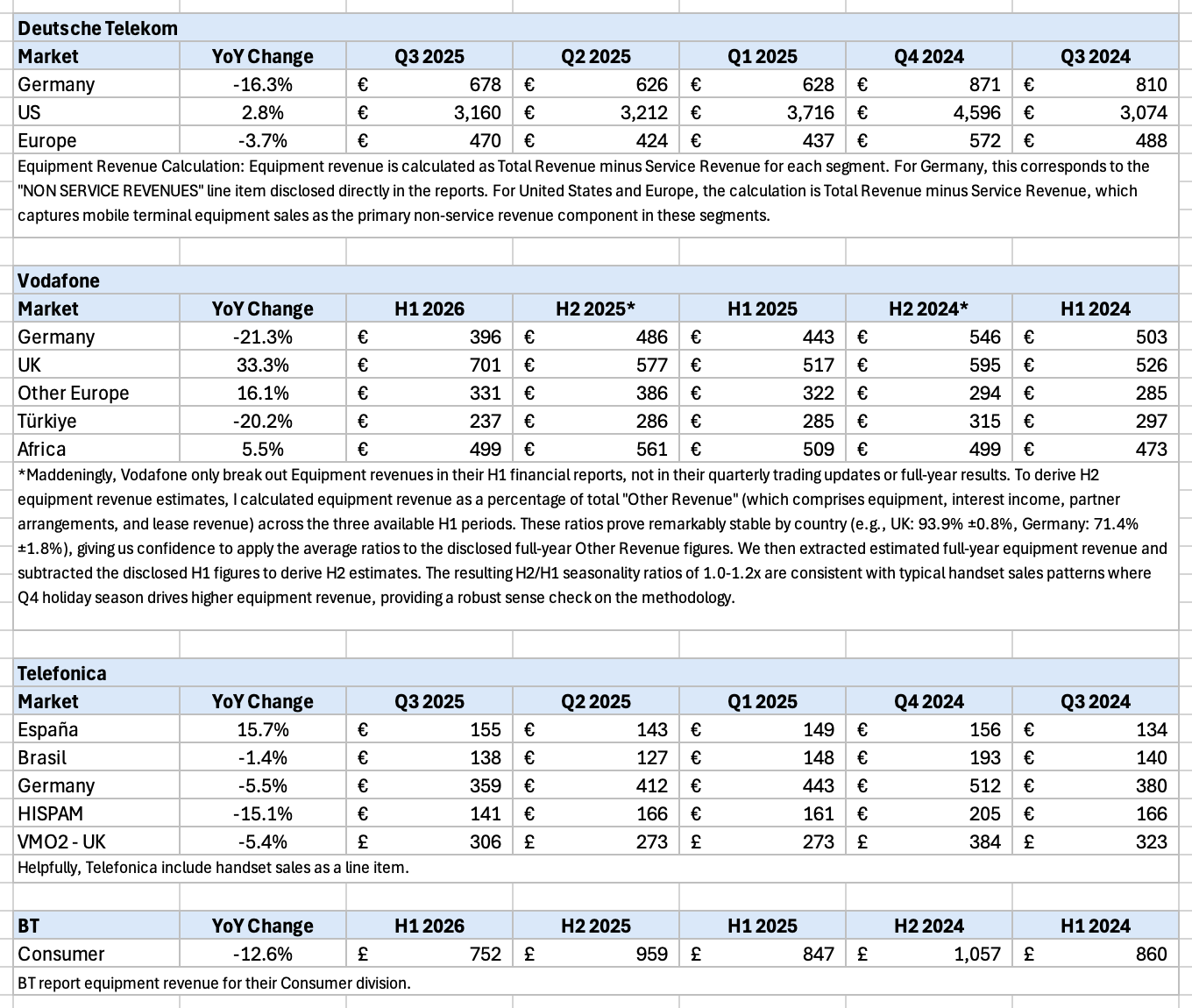

Without a subscription to IDC, Counterpoint and so on, telco equipment sales data is one of the few practical proxies available for future device activity. However, I’ve mentioned before, it’s not always possible to extract handset data from other equipment sales like set-top boxes, routers and so forth. So it’s usually directional, although in some cases (Telefonica, TMUS) there’s specific handset sales data. As we all wait to see if the iPhone17 hype is real, there are couple of Q3 highlights offsetting an overall European decline (from this list) of 3%:

So directionally, here’s a skip through some of the Q3 results:

Equipment revenue for DT in Germany was up QoQ but down 1.3% YoY. The US was up 2.8% YoY and the other European OpCos were down 3.7%.

Vodafone’s equipment revenue was down a significant 21.3% YoY in Germany and down 20.2% YoY in Türkiye. Other Europe and Africa posted gains and the UK’s 33.3% rise was down to the full period consideration of the results from Three.

BT’s Consumer division posted a 12.6 YoY decline in equipment sales.

Good news for Telefonica in Spain with sales up 15.7% YoY offset by declines everywhere else. If anyone has any additional info on the Spanish handset sales increase, please feel free to comment below. I reported on VMO2 last month but included them here for completeness.

Sticking with Telefonica for a moment, the insurance captive, Telefonica Seguros filed their FY2024 accounts. There will be a deeper dive at some point over the next few weeks, but a preliminary peak highlighted that despite a drop in UK handset sales, attachment rate improved 0.4pp to 10.1% (FY2023: 9.7%). Attachment rates crept up in Spain as well to 4.9% (FY2023: 4.7%) and even Germany showed some improvement to 2.4% (FY2023: 2.2%). At 10% attachment rates, the German insurance premiums could top €100m rivalling the UK. Someone will crack that nut one day.

More insurance results came through courtesy of Assurant with hints a significant win11. The company’s Connected Living division (device protection, extended warranty, trade-in) posted a 10.6% increase in Adjusted EBITDA to $127.8m (Q3 2024: $115.5m) driven by new client programmes and partnership expansion. Net earned premiums and other income grew 10.9% YoY to $1.36bn and net written premiums rocketed 20.6%. There was a management note about some backward vertical integration in the trade-in offer to cover logistics. The bigger news, however, was the new partnership with the “world’s largest specialty consumer electronics retailer” which matches the fact that BestBuy’s GeekSquad protection plans switched from AIG to Assurant on 12th August. Big win.

The historic challenge getting individual franchisees to sell B2C insurance policies via buying groups may have been finally bridged by Domestic & General’s new partnership with Euronics UK. According to the press release all parties are delighted to offer “IndieCare” via Euronics 430 independent UK stores12. Appropriate retail pricing and inappropriate commission rates will be key in translating projections to performance with both fixed term (single premium) and subscription (recurring premium) policies available. I’m unclear about Euronics UK revenues at over £250m versus holding company revenues at Combined Independents (Holdings) Ltd closing in on £500m but either way attachment rates between 5% and 10% would build a pretty decent programme. Good luck.

Foxway’s Q3 2025 performance13 offered tentative signs of stabilisation, with revenue declining just 0.7% year-on-year to SEK 2,116.6 million (€182.0 million), though constant-currency growth of 1.8% revealed some underlying momentum as CWS and Recommerce C&E finally gained traction. The segmental picture showed marked divergence: CWS posted 5.4% constant-currency growth as Q1 contract wins began converting to revenue, with operational EBITDA margins improving to 5.2% from 4.6%; Recommerce C&E delivered standout performance with 59% EBITDA growth to SEK 45.2 million (€3.9 million) driven by enterprise equipment demand and Teqcycle expansion; whilst Recommerce Mobile continued struggling, declining 4.9% in constant currency as aggressive competitor pricing in the Marketplaces channel compressed both volumes and margins, with operational EBITDA falling 39.4% to SEK 48.2 million (€4.1 million). Management’s observation that the historically expected post-iPhone-launch market rebound hasn’t yet materialised may reflect broader market weakness, or Foxway’s own pricing discipline in the face of aggressive competition could be obscuring early demand signals that competitors are capturing through margin sacrifice. Group adjusted operational EBITDA of SEK 107.4 million (€9.2 million) at a 4.8% margin remained under pressure but crucially cash flow swung decisively positive to SEK 150.2 million (€12.9 million) as inventory reductions in CWS and C&E partially offset Mobile’s working capital intensity. Net debt declined 3.6% sequentially to SEK 3,100.3 million (€266.6 million) whilst alternative net debt reached SEK 2,173.1 million (€186.9 million), though the leverage overhang remains unresolved with nine-month operational EBITDA of just SEK 167.5 million (€14.4 million) at a 2.8% margin tracking well below the annual run-rate required for covenant compliance. Nordic Capital’s deleveraging timeline continues slipping further beyond original expectations, reinforcing the strategic bind whereby operational improvement must accelerate dramatically to restore acquisition capacity before competitive dynamics force Foxway from consolidator to target whether they like it or not.

The report that Foxway have partnered with Tre Sverige14 should bring some cheer, at least as another proof point. But, from the last full-year results the carriers revenue recognised at a point in time (handsets) was €189m, so let’s say 250k units. Three’s total take back of devices across the group was 140k units15, so the Swedish volumes are not going to be enormous. The Swedish deal comes on the back of the same product partnership in Denmark so something is clearly going right for Foxway, just not big enough or quickly enough to counter the ever increasing cost of financing.

Absolutely fantastic to read that Fairphone are expanding into the US market16. After announcing a big (61%) jump in Q3 revenue growth YoY, the Dutch modular phone creator are embarking on going State side with their Fairbuds XL. According to the launch release, growing US consumer interest in sustainability as right to repair bills are live in every state. Let’s hope the Amazon sales take off and more products follow.

A few interesting partnerships announced this month:

Reconext has integrated its ITAD services directly into ServiceNow, allowing enterprises to manage the entire end-of-life device process, from retirement requests through logistics, data wiping, and final disposition, all within the same platform they already use for IT asset management17.

Raylo are putting their platform expertise to good use powering Dyson Renewed product subscriptions18. UK customers get to access certified Dyson refurbished products on flexible, low-cost subscriptions with every device being returned for refurbishment at the end of the term.

Congrats to Phil Kemish and the rest of the Reboxed team for the tie-up with USwitch. They’ve launched a new co-branded comparison marketplace. The site integrates Reboxed’s technology and allow users to purchase used devices and trade in old handsets.

Finally, according to an AIM group release19, Back Market CEO, Thibaud Hug de Larauze projects that the company’s turnover will grow by 30% year-over-year to reach $3.5 billion. That sounds like it confirms ECDB’s projections of over €3bn GMV which would suggest actual revenue to be €350m - €525m on a 10-15% commission range. Perhaps they’ll even go so far as to publish some accounts this year. Nah.

Investments

Orange has agreed to buy the remaining 50% stake in MasOrange, its Spanish joint venture, from private equity firms KKR, Cinven, and Providence for €4.25 billion, giving it full control of Spain’s largest telecoms operator just 19 months after the original merger20. The deal, expected to close in H1 2026, effectively costs Orange almost nothing out-of-pocket since it received €4.4 billion in cash during the 2024 merger structure. Full ownership eliminates shared governance with the PE firms, allows Orange to accelerate strategic decisions around 5G and fiber investments, and blocks a potential IPO that the PE firms could have triggered from April 2026.

SquareTrade Limited (the UK entity) was the recipient of an £18.4m capital injection at the end of October (filed November). The FY2024 accounts don’t indicate any liquidity concerns so something interesting might be brewing. One to watch.

It’s now been over 12 months since the Ingram IPO and up until recently share performance has been, well, miserable compared to, well, everything. Still, that hasn’t stopped Platinum Equity beginning to unwind their position21.

More PE goings on as the Aurelius acquisition of Exertis (and MTR) from DCC has come through the legal entity filings. The charges filed show a standard two-tier LBO structure with the acquisition debt held at the Irish holdco and Wells Fargo ABL facilities at the operating companies including MTR Group. Whether or not the thin-margin, high-working-capital businesses can support leverage is possibly a question Aurelius should have asked of Nordic Capital.

For those looking to raise, there’s still cash out there:

e-Bike circularity specialist Upway nabbed $60m bringing total funding to $125m22.

Turkish refurbished electronics platform, Easycep, raised €45m to accelerate expansion in the smartphone market and widen the product set23.

Vinted began to explore a share sale at an €8bn valuation allowing some early investors to cash out24. Any process is likely to kick off in 2026. Slightly outside our wheelhouse, but worth watching for buyer appetite.

And that’s about it for the month. A very warm welcome to new subscribers and another pat on the back to everyone getting this far! A heartfelt thank you to those of you who chose to pay for another month or for the year. It’s very much appreciated and will help me expand the research. If you’re finding the content useful please like or comment as it really helps out with the substack algorithm.

The next round up will be early in 2026 and so I’ll take this opportunity to wish you all a merry Christmas and a happy New Year and may it bring peace to those that need it the most.

Best,

sb.

Another valuable summary, Stuart. thank you!