Research Update: Galaxy Finco (Domestic & General) - FY2025

MAAGA: Making American Appliances Great Again...

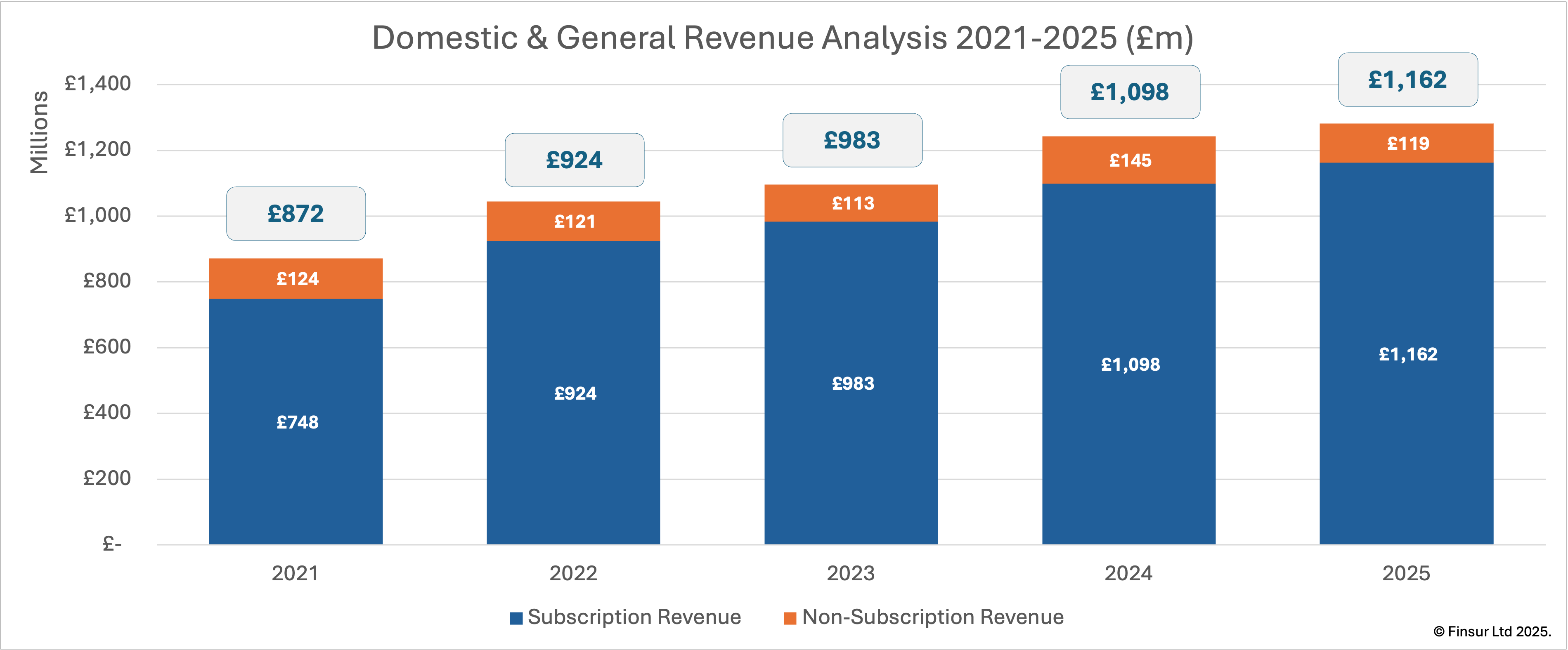

Key Findings: Domestic & General reported £1,162m revenue in FY2025, up 5.8% year-on-year, with subscription revenues now representing 90% of total group revenues at £1,043m. Adjusted EBITDA increased 14% to £162m with margin expansion to 13.9%. The UK delivered £912m revenue (+7%) though customer numbers stabilised at 4.7m. US subscription revenue surged 213% to £34m. With leverage improving to 4.9x and a 189% solvency ratio, valuation range of £1.8bn to £2.0bn looks achievable.

One of the reasons I started this substack was as a personal antidote to the absolute plethora of dubious statistics that permeate the online world. Over the past few months I’ve seen some gargantuan mobile phone insurance market size and growth rate predictions1 and secondhand device market sizes from a company that can also do you a report on the size of the global chicory market for $3,9992. There’s the biggest this or the fastest that but, one company you’ll not find in the fastest warranty company to a billion pounds in revenue category, is Domestic & General. Known to most as D&G, they reported surpassing the revenue milestone in 2024 a mere 112 years after being established in 1912. Good for them, not everyone needs to be on a list.

Recap

After starting life as an international cattle transit insurer, D&G’s predecessors first protected home appliances in the 1960’s and after a series of acquisitions were listed on the London Stock Exchange in 1991 adopting the now familiar moniker. In 2007, PE group Advent took them private before selling them to CVC in 2013. From memory, their key product at that time was a discretionary service plan (DSP) which contained a clause along the lines of “if we decide to pay out”. But, if it looks like insurance and it smells like insurance, it’s probably insurance and from 2018 the firm transitioned to insurance plans and capitalised the business accordingly. Welcome then, was the additional investment from the Abu Dhabi Investment Authority who took a 30% stake for an undisclosed sum. Since then the ownership percentages have shifted around a little with CVC maintaining their majority shareholding.

D&G operate in the UK where they are the largest home appliance insurer, Europe (with entities in Germany, Italy & Spain), Australia and more recently in the U.S. after winning the Whirlpool account in 2021 and strengthening operations with the 2023 acquisition of After, Inc. At the top of the group sits the Jersey-based “Galaxy” holding companies with the main insurance company, Domestic & General Insurance plc domiciled in the UK. The latest annual report highlights a total of 6.7m subscribers, 2.7m repairs and 400k replacements annually and looks shiny enough to be ready for a London listing. Let’s jump right in…

Performance

FY2025 Key Metrics:

Revenue: £1,162m (FY2024: £1,098m, +5.8%)

Subscription Revenue: £1,043m (90% of total, +9.3% YoY)

Adjusted EBITDA: £162m at 13.9% margin (FY2024: £142m at 13.0%)

UK Revenue: £912m (+7% YoY), 4.7m customers

European Revenue: £187m (-7% YoY)

US Subscription Revenue: £34m (+213% YoY)

Claims Ratio: 44% (9-year average maintained)

Combined Ratio: 94.5% (FY2024: 95.3%)

Retention Rate: 86%

Net Debt: £786m, Leverage: 4.9x (FY2024: 5.3x)

Solvency Ratio: 189%

Source: Galaxy Finco Limited filed accounts for year ending 31 March 2025

After breaking the £1bn barrier in 2024, management continue to sound pretty upbeat as the growth story continued into 2025. Total revenue reached £1,162m up 5.8% from £1,098m in FY2024. Over the 5-year analysis period from FY2021, D&G have registered a 7.5% CAGR.

From a product perspective, management are focused on developing the subscription business (old school: recurring premium) versus a planned decrease in non-subscription business (old school: single premium) suggesting that it’s higher quality. I’m not sure I wholly agree. Single premium has it’s place in consumer choice, but I get that subscriptions are better understood by investors and cashflows are more predictable. The focus is working. Subscription revenues climbed 9.3% from £954m in FY2024 to £1,043m in FY2025 with retention remaining remarkably stable at 86%. Non-subscription revenues dropped 17.9% in FY2025 after a jump in FY2024 due to the acquisition of After, Inc. Subscription revenue now accounts for 90% of the total group revenues with an 8.7% CAGR over the analysis period.

The UK delivers the vast majority of revenues, with apparently 1-in-4 households protected by a D&G policy3, although I’m not sure I can square that statistical circle. What is clear though, is that D&G managed to grow revenue 7% in their home territory from £855m in FY2024 to £912m in FY2025. It’s important to note, however, that the increase was completely attributed to more plans per customer and price increases as UK customer numbers stabilised at 4.7m. Revenue per revenue per customer increased from £147 in FY2024 to £155 in FY2025. B2B2C insurance firms have for the most part absorbed inflationary pressures, but that cannot continue ad infinitum.

European revenues dropped 7% from £201m in FY2024 to £187m in FY2025. However, this hides a 9% growth in subscriptions revenues offset by a 34% drop in single premium business, meaning that the subscription business now makes up 74% of the revenue, up from 63% last year. US subscription revenue grew significantly from £11m to £34m an increase of 213%. This took the subscription mix from 25% in FY2024 to 54% in FY2025.

Continue reading for:

Profitability analysis including claims ratio, technical ratio and combined ratio dynamics

Balance sheet assessment: £786m net debt, refinancing structure and solvency position

Commercial model deep-dive: commission structures, distribution network economics and partner tenure

US market analysis: Whirlpool deal extension and growth runway

Strategic outlook and valuation assessment

Also available as a standalone pdf report here.