Apple Operations International FY2025

Cork's popping...

Key Findings:

- Apple Operations International reported net sales of $235.3bn for the year to 27 September 2025, up 5.9%, consolidating almost all of Apple’s business outside the US.

- AOI’s reported net income of $68.9bn equals 61.5% of Apple Inc’s $112.0bn group net income, before the further US tax due as profits move up the chain.

- AOI is Ireland’s largest company by filed turnover, recording roughly four times the combined revenue of the ten largest companies listed on the Irish stock exchange.

- AOI paid dividends of $69.4bn, marginally above the $68.9bn earned in the year, and increased lending to its parent by 25.9% to $60.3bn.

- Apple Distribution International, the principal non-Americas distribution channel, files no standalone accounts under an Irish parent-guarantee exemption, leaving online-direct revenue outside the public record.

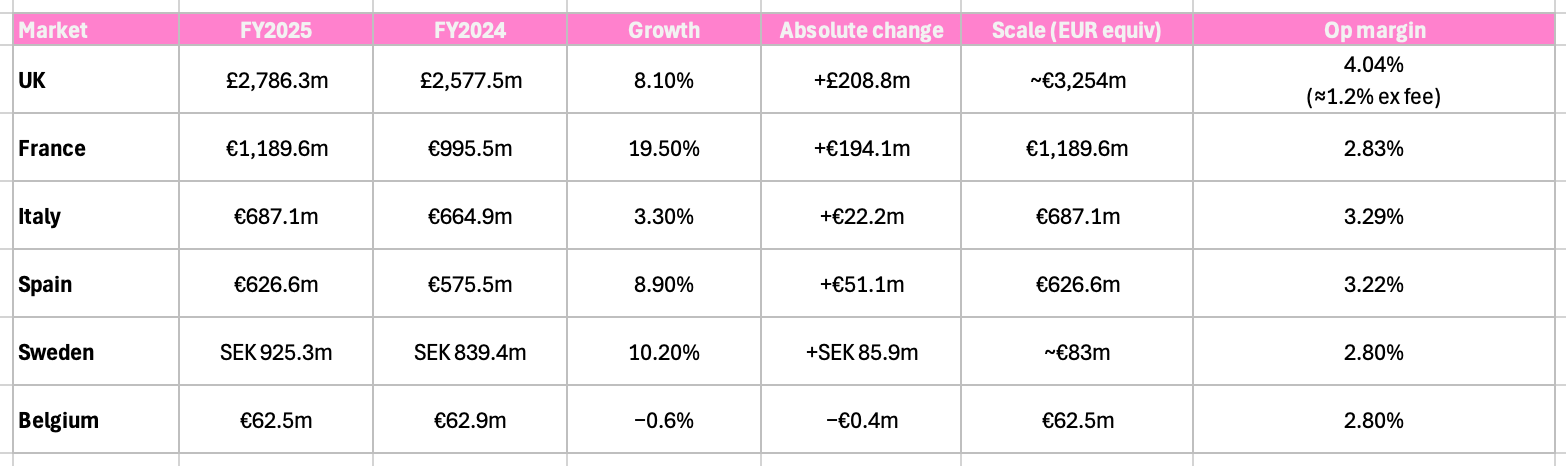

- Five of six filed European retail markets grew in FY2025, from France at +19.5% to Belgium at −0.6%, with UK turnover the largest at £2,786.3m, up 8.1%.

- Filed retail operating margins across all six markets fall within a narrow band of 2.80% to 4.04%, the UK figure lifted by a £79.6m intra-group service fee.

- Apple Europe Limited booked £1,377.0m of intra-group service income at a 68.5% operating margin, retaining £723.5m after a £242.1m UK tax charge, most of it lent back to the group.

I’ve been monitoring the ongoing channel switch by UK device buyers for a while. The evidence so far has been found in the declining Operator Equipment Revenues and increasing Apple Retail UK results. Looking for similar evidence in Germany’s Unternehmensregister was a short and fruitless exercise. Apple Retail Germany B.V. & Co. KG files no accounts under the §264b exemption (which lets a German partnership skip publishing its own accounts when a parent consolidates them). Following the partnership chain up and across, Apple Retail Europe in Ireland, acting as the limited partner, and Apple Holding B.V. in Amsterdam, acting as the general partner, took exemptions that didn’t give me any clues either. Stepping up another rung in the ladder gets you as far as Apple Operations International (AOI) of Hollyhill Industrial Estate, Hollyhill, Cork, Ireland. And they do file accounts, big ones…

Performance & Profit

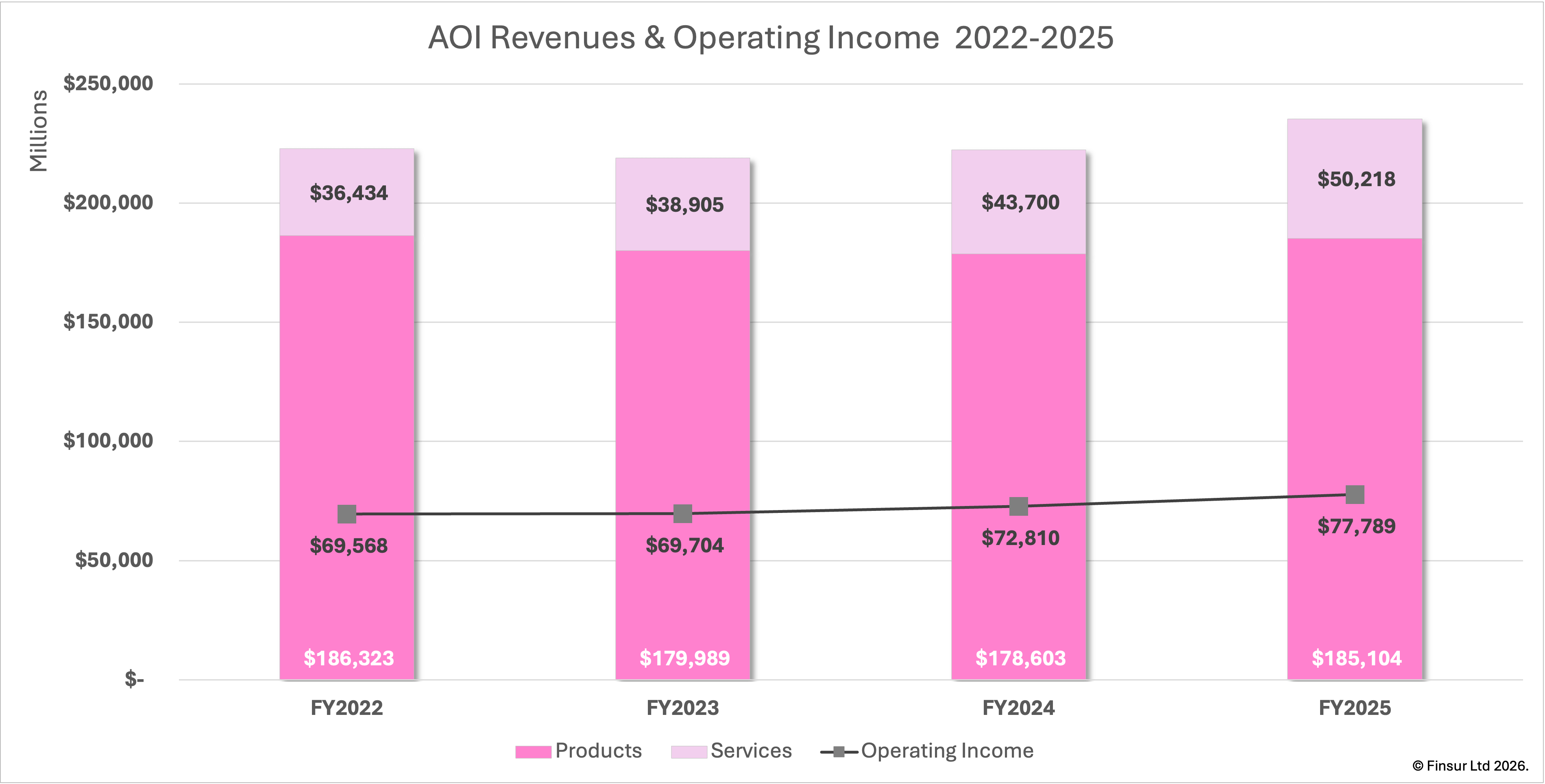

AOI's net sales were $235,322m for the year to 27 September 2025, up 5.9% from $222,303m a year earlier. Converted to euros, that's about €208.5bn. Operating income came in at $77,789m and net income at $68,887m, up from $51,158m in the previous year, although that year bore a one-time state-aid tax charge of $14.8bn, which accounts for most of the apparent jump.1 In the most recent Irish Times Top 1000, Apple's Irish operation is Ireland's biggest company by filed turnover at €205.4bn for the year to September 2024 with Google a long way second at €77.3bn and Microsoft third with just under €74bn.2 AOI turns over more than four times the combined revenue of the ten largest companies listed on Ireland's own stock exchange.3

Even at the AOI level and as you might have come to expect, management provide extremely limited analysis on the top-line number. There’s no country analysis and only a two-way split into products and services. Products net sales were up 3.6% to $185,104m (FY2024: $178,603m) and services net sales were up 14.9% to $50,218m (FY2024: $43,700m). The faster-growing, higher-margin part of the business is expanding its share, including income from iCloud, AppleCare, advertising, payments and content alongside the commission Apple retains on third-party apps through the App Store, recognised net of the publisher / developer share rather than the gross consumer spend. The $50,218m services revenue therefore sits well below the total value transacted across the channel. Overall, gross margin was up 8.6% to $110,819m (FY2024: $102,017m) with the rate widening to 47.1% from 45.9%, highlighting the mix shift towards services.

AOI’s operating expenses were up 13.1% to $33,030m (FY2024: $29,207m) split between R&D at $19,473m up 15.1% YoY and SG&A up 10.3% to $13,557m. Cost growth ran well ahead of the 5.9% increase in the revenue line, but the gross margin expansion easily absorbed it. Operating income was up 6.8% to $77,789m (FY2024: $72,810m), edging up the operating margin to 33.1% (FY2024: 32.8%). Roughly a third of every dollar of non-US net sales inside AOI ends up as operating profit. Not many places better than Ireland in which to capture such efficiency.

Net income was up 34.7% to $68,887m (FY2024: $51,158m), though the comparison is somewhat distorted by the aforementioned tax charge. Stripping that out by adding back the $14.8bn net charge would lift FY2024 net income back to about $66.0bn, putting FY2025 up 4.4% on an underlying basis against the headline. On the surface, the effective tax rate fell to 14.9% (FY2024: 33.0%) but stripping out the state-aid line, the underlying rate for FY2024 would have been about 12.3%, pretty close to the 12.5% statutory rate. FY2025's charge includes $1.4bn of Pillar Two income taxes, the first year the OECD global minimum tax rules apply to the group. It’s worth noting that further US-level taxation applies to the profits once they reach Apple Inc.

The scale of AOI’s cash generation is keenly illustrated by the dividends of $69,444m (FY2024: $67,621m, +2.7%) at a dividend per share of $6,944,367. Not your usual cents on the dollar. The total distribution slightly exceeded the $68,887m earned in the year, which meant that retained earnings ended marginally lower at $49,174m against $49,731m and total equity was flat at $47,925m against $47,967m. Outbound cashflows didn’t end there. Loans owed to AOI from the parent increased 25.9% to $60,344m (FY2024: $47,923m), the balance growing $12.4bn in the year whilst AOI’s own cash and marketable securities fell as surplus liquidity was swept up.

Scope

AOI’s consolidation is not, unfortunately, a tidy sales holding structure out of which we can calculate retail sales but a rather ungainly sprawl spanning roughly a dozen distinct activity types: holding companies, sales and distribution, national retail, manufacturing and procurement support, sales support and marketing, research and development, technical services and data centre operations, advertising resale, payment services, software, and minority stakes in renewable energy generation. If anyone was expecting an overseas sales arm, reset. AOI is the consolidation point for almost everything the group does outside the US. The geographic reach runs to well over thirty locations, from Delaware holding shells at the standard Wilmington registered-agent address through Ireland, the major European markets, the Gulf, Nigeria and Egypt, across to China, Japan, Korea, India and Southeast Asia. The Cork-based parent sits atop the lot.

AOI’s “nature of business” column from the subsidiary table in the filed accounts could be a legend for the group’s margins. A small set of phrases recurs across the list: “sales support, marketing and related services", "research and development, technical and other services", "sales, distribution and related services", and "retail company". Every national store operator is categorised as a “retail company” and in each, the filed operating margin sits in the low single digits: France, Belgium and Sweden on 2.8 per cent, Spain 3.2 per cent, Italy 3.3 per cent and the UK 4.0 per cent, although this includes £79.6m of intra-group service-fee income. Strip that and the pure UK reselling result is about 1.2 per cent. The two entities carrying the "sales support, marketing and related services" label that can be checked, Apple France and Apple Europe Limited, ran 72.0 and 68.5 per cent operating margins. The one "research and development, technical and other services" entity that files standalone, Apple (UK) Limited, ran 19.7 per cent. It appears that each functional subsidiary sits in a discrete margin band with support and marketing the richest, R&D in the middle and retail the thinnest. The uniformity of a margin that lands within a point and a half of itself across six countries suggests margin calibrated function by function and administered from Cork.

Alongside the UK R&D entity, two further R&D operations sit in Europe: Apple Technology Engineering B.V. & Co. KG in Munich and Apple Technology Engineering Austria B.V. & Co. KG in Linz. The data-centre operations sit elsewhere, in two Chinese entities, Apple Technology Services (Guizhou) and Apple Technology Services (Ulanqab). Beyond device related activities, the subsidiary list is still extensive. There’s Apple Advertising (Beijing) Ltd, whose stated business is to "promote and resell advertising placement service"; Apple Payments Services Limited at 280 Bishopsgate, London, providing "account information services" of which Apple Distribution International Limited is an appointed representative and acts as a credit broker.4 There’s UAB "Pixelmator Team" in Vilnius, "sales and distribution of software", the Lithuanian image-editing business Apple acquired.

Each subsidiary is a small entity carrying a larger signal about where the group has been and where it’s headed. Shazam Entertainment Limited, registered at The Shard in London, and acquired by Apple in 2018,5 is listed with its nature of business stated simply as "Inactive". Looking forwards, a cluster of renewable energy entities are held at partial stakes, unusual in a group that is otherwise almost entirely wholly owned. They include Chinese photovoltaic stations (Kangbao, Hohhot, two Aba Prefecture entities), a Chinese wind-farm operator (Nanyang Runtang), rooftop solar in Japan (Daini Nihon Solar Power), a photovoltaic operator in India (Clean Max Hyperion) and a Singapore-registered renewable fund (China Renewable Energy Fund II). These clean-energy stakes suggest some central procurement for the group's renewable-power commitments rather than an energy business in its own right, which the small scale and the generation-only descriptions support.

Filing Exemptions

The short and fruitless exercise in Germany was not an accident. The §264b dead end was the first wall of several, each a lawful relief from publishing local entity accounts and each claimed in a different jurisdiction. Taken individually, each exemption is unremarkable, but stacked across the group, they leave almost nothing standalone to read.

Searching in the Netherlands ended with a similar result. Apple Holding B.V., the general partner in the German retail business, files under Article 403 of Book 2 of the Dutch Civil Code, with the parent assuming liability and the results absorbed into group accounts. Apple Retail Netherlands B.V., the national store operator, filed its own accounts through 2021 and from 2022 switched to depositing group accounts under Articles 403 and 408 of Book 2 of the Civil Code. The turnover line that had been visible for years simply stopped.

Apple Distribution International, the Cork entity that is the principal distribution channel for the group outside the Americas, takes the Section 357 Companies Act 2014 exemption under a parent guarantee and files no standalone accounts. The revenues running through Apple's main European route to market are simply not in the public record.

The other method employed by management is redaction, rather than absence. Apple Europe Limited in the UK does file full accounts but declines to analyse turnover, citing paragraph 68(5) of Schedule 1 to the 2008 Regulations on the directors' view that disclosure would be seriously prejudicial; its related-party note discloses nothing, taking the FRS 102 Section 33.1A exemption as an indirect subsidiary of Apple Inc. The two lines that would reveal most are the two withheld. Seriously prejudicial?

European Retailers

Despite the purposeful calibrations and persistent exemption usage, there are still six European Apple retail entities providing a counterpoint to something missing. Of the six, the UK and France file a full set of accounts because the parent-guarantee filing exemption needs a qualifying parent that neither has. The UK specifically, post-Brexit, limited the s.479A audit exemption to groups headed by a UK-established parent for accounting periods commencing on or after 31 December 2020. With Apple Retail UK's parent incorporated in Ireland, the exemption is no longer available and a full audited set follows.6

Given this is a first capture, it’s not possible to imply a trend and there’s more work to be done to evidence any channel switching with additional country telco and retail data research required. But for now, the data offers a fixed reference point to measure future filings.

Five of the six markets grew, mostly in the mid to high single digits, Sweden into low double figures and France into the high teens. The channel switch thesis is grounded in the UK and explored in more detail in Apple Retail UK FY2025 company analysis. Set against UK telco equipment revenues declining over the same period, 8.1% growth to £2,786.3m (FY2024: £2,577.5m) is the channel switch out in the open. Apple Retail France topped the charts hitting 19.5% growth and posting almost €1.2bn in revenues with an absolute gain of €194m, unwise to suggest a trend, but consistent with the direct-channel share pattern ongoing in the UK.

Italy, from a scale position at €687.1m (FY2024: €664.9m), offered the lowest growth of the majors but market dynamics historically point to more equitable market shares across channels. Spain’s 8.9% growth was material, pushing Apple’s sales up to €626.6m (FY2024: €575.5m). However, Telefónica’s 17.9% domestic equipment sales growth was also impressive in the period, so this might be part of a broader market upgrade cycle.7

Growth in Sweden hit double figures at 10.2% but from a relatively low FY2024 base of SEK 839.4m (~€75.3m) to SEK 925.3m (~€83.0m). With Telia and Telenor both dropping equipment sales by around 4.0% over the last 12 months8, this might suggest a consumer preference moving towards direct purchase. Belgium’s -0.6% decline is the only contraction in the data set and at total revenues of €62.5m, is a fraction of the majors.

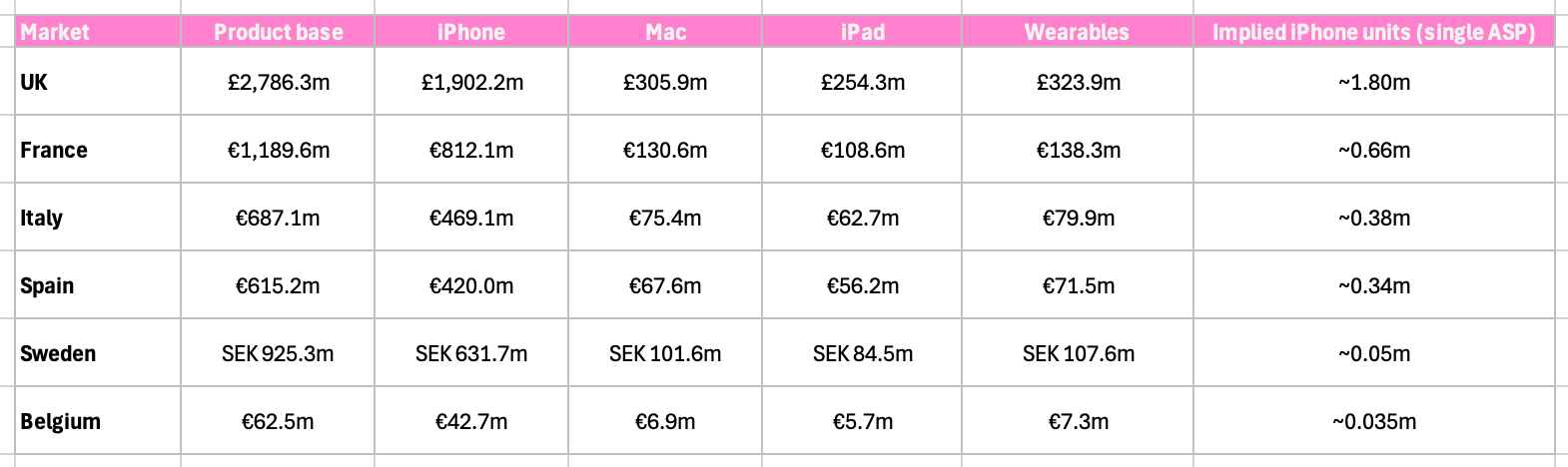

Lifting the reported US hardware product mix over the pond, stripping out the services element and re-weighting the percentages gives a solid proxy to apply to Apple’s retail revenues for some idea of product line sales. This means that the iPhone sits at roughly 68% of product revenues across the board and the table below therefore provides relative iPhone scale across the markets.

Implied iPhone revenues of about £1.90bn in the UK and €812m in France dwarf the other markets. Italy follows at €469m and Spain at €420m, with Sweden at SEK 631.7m (~€56.7m) and €42.7m in Belgium. Implying units using a single ASP for comparison purposes (£1,057 / €1,235), means roughly 1.80m iPhone sales in the UK, 0.66m in France, 0.38m in Italy, 0.34m in Spain, and then about 50,000 in Sweden and 35,000 in Belgium. That implies a total of roughly 3.3m iPhone sales across six of Apple’s European retail markets. Add the exempted markets back in, and at a complete guess Apple are probably selling in excess of 5m iPhones from their retail stores plus another several million directly online. Not too shabby.

Regional Principal

Back in my July 2025 article on Apple Retail UK, I’d mentioned the more interesting profit story was likely found in another UK based entity, Apple Europe Limited.9 As another subsidiary under the sprawling AOI umbrella, it’s too good an opportunity to pass up.

Apple Europe Limited provides marketing and administration support to Apple only at a charge of £1,377.0m and a cost of £433.9m. That’s a £943.1m margin even the sharpest legal and compliance consultancies couldn’t compete on. The intra-group fee is a transfer between Apple entities, so it nets to zero for the group: whatever Apple Europe books as income, the affiliates paying it book as cost. And because it nets out, the group is largely free to choose how big to make it. But the size of the fee decides where the Europe, Middle East, India & Africa (EMEIA) profit lands. Pitch the fee high, as here, and the profit pools in Apple Europe Limited. Pitch it lower, and the affiliates keep more, so the same profit shows up in whichever entities pay the fee instead. The total is unchanged; only its address moves. So setting the fee at the level that yields £943m is a decision to recognise that £943m in the UK company. With a little interest on top, it’s taxed at 25%, sending £242.1m to HMRC.

What’s left after tax, £723.5m, sits in the same closed circuit. The company declared £150.4m of dividends during the year (FY2024: £570.6m) paid up to the shareholder, AOI. The remaining profit stayed in the company, and equity climbed from £559.6m to £1,110.4m, close to doubling in 12 months. So the after-tax profit does one of two things, moves further up the group or waits on the balance sheet until it moves further up the group. In terms of cash, the company holds almost none of it. Its largest asset is a debtor of £949.2m, of which £838.7m is owed by other Apple entities: £780.8m by group companies, up from £1.7m a year earlier, and £57.9m by the parent. The money that the structure routes through Apple Europe Limited is lent straight back into the group, unsecured and repayable on demand.

So what is Apple Europe Limited? On paper, it’s a provider of marketing, sales support and administrative services. But the economics describe something else entirely: a regional principal carrying the strategy, the risk, the expensive management and the residual EMEIA profit. A genuine support function earning £943m at a routine markup would be sitting on billions of pounds of cost, not £433.9m. The only explanation that would justify the margin is the one the accounts do not make, with the Section 33.1A exemption taking the counterparties and the pricing method off the page. What remains is the substance: 1,072 people and a £297.4m payroll, real enough to make the UK a defensible home for a large slice of EMEIA profit and to pay the 25% in full, where a thinner, lower-taxed location would not survive a second look. All the accounts tell us is why some profit is taxed in the UK, not why it runs to £943m, and the exemption Apple Europe has taken means it never has to.

International Conduit

Step back up from the UK company and it all resolves to a single address. Apple Europe’s dividends run up to AOI, its £838.7m receivable is lent straight back into the group that AOI consolidates, and the retailers, the calibrated margins and the withheld lines all point the same way. Everything laid out here routes through Hollyhill on its way to Cupertino. AOI paid out $69.4bn against $68.9bn earned, a shade more than it made, and grew its lending to its own parent by a quarter to $60.3bn. That $68.9bn is 61.5% of the $112.0bn Apple Inc reported worldwide, taxed in Ireland but not yet in America. It lands in Cork and keeps moving. A holding company by name, a fascinating conduit by numbers, and on which basis, Cork is absolutely popping.

Peace,

sb.

Finsur is reader-supported and the analysis takes time. Please consider a paid subscription and if not, a free subscription really helps with traction. Additionally, if you can find your way to leave a comment, or even a hit the heart for a like, it makes a big difference.

Methodology

All figures are drawn from filed accounts read directly. The primary sources are the Apple Operations International Limited consolidated accounts for the year ended 27 September 2025, filed with the Irish Companies Registration Office, and Apple Inc’s Form 10-K for the same year end. The six European retail results, together with Apple Europe Limited, Apple France and Apple (UK) Limited, come from each entity’s own statutory filing, sourced from the UK, Irish, French, Italian, Spanish, Belgian and Swedish registers as applicable. Accounting frameworks differ: the AOI group accounts under IFRS as adopted by the EU, the AOI company and the UK entities under FRS 102, the Continental entities under local standards, and Apple Inc under US GAAP. Comparisons across them are directional and presented as such.

Currency conversions use ECB annual average reference rates, EUR/GBP at 0.857 and EUR/SEK at 11.15 for 2025, with figures kept in their reporting currency where directly cited. Each entity closes in late September, so the calendar-year average is a close approximation rather than an exact fiscal-year rate; the difference is immaterial to a turnover comparison and the figures serve only to place entities on a common scale. The implied iPhone split applies Apple’s FY2025 hardware product mix, services stripped and the four hardware lines reweighted to 100%, placing iPhone at roughly 68% of product revenue. Implied units apply a single average selling price across markets for comparison only; they are indicative, not a market price, and the genuine per-market figure will differ.

Two limitations bound the retail analysis. The comparable data spans two years only, FY2024 and FY2025, so it fixes a reference point rather than a trend. And the read is partial by design: the entities that file are set against a wider group that does not, including Apple Distribution International in Ireland and the German and Dutch retail operations, each having taken a lawful exemption from publishing standalone accounts. Statutory references are to the relevant companies legislation in each jurisdiction.

Apple Operations International Limited, consolidated financial statements for the year ended 27 September 2025, Note 6 (Provision for Income Taxes). Following the European Court of Justice’s judgment of 10 September 2024, which reinstated the European Commission’s 2016 state-aid decision, the Group recorded a one-time income tax charge of $14.8bn net in FY2024, being $15.8bn payable to Ireland from the escrow account less a $1.0bn reduction in its uncertain tax position. For background to the dispute, see Wikipedia: Apple–EU tax dispute.

Combined revenue of the ten largest companies by primary listing on Euronext Dublin, drawn from each company's most recent published full-year results: Ryanair €13.95bn (year to March 2025); Kingspan €8.61bn, Kerry Group €7.98bn, AIB Group €4.91bn, Bank of Ireland €4.33bn, Glanbia €3.55bn, Uniphar €2.77bn, Origin Enterprises €2.05bn, Cairn Homes €0.86bn and Dalata Hotel Group €0.65bn (all years to December 2024). The total is approximately €49.7bn, against AOI's €208.5bn, hence more than four times. Figures are reported group revenue except the two banks, stated as total operating income (net interest income plus other income), there being no comparable turnover line for a bank, and Glanbia, converted from a reported US$3,839.7m at the 2024 average rate. The basis is primary Dublin listing, which excludes three larger companies that have moved their primary listings elsewhere: CRH and Smurfit WestRock to the New York Stock Exchange, in 2023 and 2024 respectively, and DCC to London. Reporting periods differ, as noted. Sources: company full-year results announcements, accessed 9 June 2026.

Grant Thornton, “Are you ready for the end of parent company guarantees?”: https://www.grantthornton.co.uk/insights/opinion-blog/are-you-ready-for-the-end-of-parent-company-guarantees/

Finsur analysis: Q4 2025 Equipment Revenue Tracker.