March Round Up

Make hay Mr Fox...

It’s hard to keep up with market values. As regular readers of this Substack might recall, my disdain for the inflated numbers often bandied around is measurable. This month I’ve seen two reports released on the global refurbished phone market: one with a 2025 value of $20 billion projecting $75bn by 2033 at a 15% CAGR and another putting the 2025 market at $34.94 billion growing to $57.66 billion by 2032 at a 7.41% CAGR. I’m not even going to grace them with a reference. Instead, here are some news items from March that are far more worthy of your attention…

Market

There was one particular press release that did deserve some unpacking. In this instance a press release issued by PR agency Definition, implied that £23.47bn in unrealised UK trade-in value had been identified in a new research report collab between Alchemy & FDM CCS Insight1. That headline grabbing figure duly made its way into trade coverage including Mobile News2. But the attribution is misleading. The CCS Insight work is a separate piece of consumer research covering trade-in barriers, upgrade intent and loyalty across a combined US and UK sample3; the £23.47bn is a press office calculation derived from an entirely separate Censuswide survey of 2,000 UK adults, buried in the Notes to Editors, and based on consumers' self-reported perceived device values rather than actual secondary market prices, which makes it complete nonsense. Additionally, the press release methodology note manages to be internally inconsistent: 2.89 unused devices at £283.99 per household produces £820.50, which multiplied by 28.6 million UK households equals £23.47bn; but the note also states a per-household figure of £599.13, which would produce a total of £17.1bn, and implies an average device value of £207.31, not £283.99. None of this appears in the Alchemy/CCS published report, which contains genuinely useful data on structural trade-in barriers, which I also covered at the beginning of December last year in Europe’s Retention Problem.

Contrast these device values with what Virgin Media O2 reported to have paid out over the last year4 and the value gap perfectly illustrates the Alchemy/CCS top reason preventing trade-ins: values are too low. VMO2 paid out £6.6m to customers for approximately 85,500 devices. That averages out at £77.20, well below the consumer-perceived device value cited in the Censuswide survey. In addition to the value gap, other equally familiar reasons resurfaced in the VMO2 news release including 70% of customers worrying about personal data being accessed if they pass on or recycle their old smartphone. More than three quarters of customers said they would be more likely to recycle their old device if they could make money from it, while almost seven in 10 (68%) say they would be more likely to buy a refurbished device if they had greater confidence in its quality, perceived or otherwise.

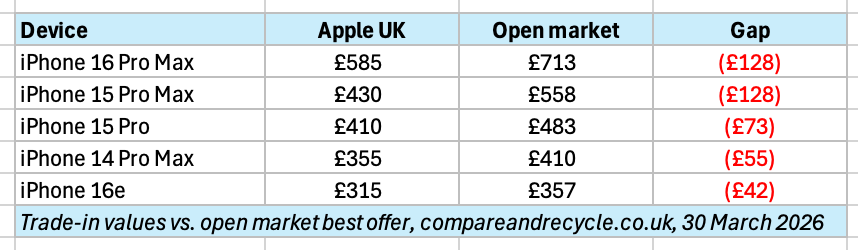

Regardless of what the consumer thinks their device is worth, market values are probably the more reliable indicator. As first reported by MacRumors, in the US, Apple has decided that your iPhone 16 ProMax is worth up to $15 more than it was last month5. Looking at the UK, Apple came to a different conclusion and decided the same phone was now worth up to £65 less at £585, down from at least £650 in December, and at the time of writing a significant £128 below the open market. Across the complete iPhone range there are ups and down with the iPhone 15 Pro Max falling the most in percentage terms down 17.3% to £430 from £520, again £128 below the open market. Whether that’s coincidence or reflective of Apple’s internal pricing logic can’t be determined from this data set alone.

With the Galaxy S26 range on sale from 11 March, the contrast with Samsung's approach is instructive. Samsung is deliberately trading above open market to retain its mid-to-premium installed base6, Apple is trading below it on every device in the UK sample, including the newly launched iPhone 16e at £315 against an open market best offer of £357. The approach to loyalty via commercial logic running in opposite directions through the same purchase channel is worth watching.

I think the Strategic Circularity newsletter is worth a share and a signup if you’re keeping tabs on EU policy movement.

Companies

Samsung stepped away from their Samsung Care+ repair-at-all-costs policy that had sometimes frustrated customers. Until now, devices covered under the policy would not be replaced unless repair was physically impossible, with customers reporting waits of up to six weeks while components were sourced and replaced one by one.7 From the Galaxy S26 launch, Samsung Care+ now guarantees a replacement device dispatched within 48 hours of a claim being accepted in the UK, with worldwide coverage limited to in-store repair rather than advance exchange. Existing Care+ customers will receive the same benefits over the coming months; US availability remains unconfirmed. The shift is worth noting beyond the customer experience improvement. Replace-first rather than repair-first means Samsung now generates an increased stream of devices flowing back through its refurbishment and parts network, rather than repaired units going back to customers. Combined with the trade-in pricing strategy discussed above and in full here, it looks less like a standalone product update and more like Samsung continuing to tighten its grip on the full device lifecycle.

Following up on my Foxway Q4'25 article here, on their investor call at the beginning of the month, the CWS lease base contraction was confirmed by management; there was explicit Mobile guidance of tough conditions through the first two quarters of 2026, with the EUR/USD dynamic adding a new US import headwind; C&E is entering 2026 with elevated inventory at SEK 368m (~€33.7m) and DRAM pricing was described as stabilising in February; and full year operating cash flow sat at just SEK 1.0m (~€92k) against a working capital commitment of SEK 688m (~€63.1m). The overarching thread was that the business headed into 2026 with one segment carrying deliberate inventory risk, one rebuilding from a contracted lease base, and one navigating structural headwinds, all on a very thin cash generation base. Until, that is, Nordic Capital and Norvestor injected SEK 300m (~€27.5m) in fresh equity, citing sourcing opportunities driven by AI infrastructure investment and giving management the firepower to act on C&E momentum without touching the bond structure. Keep that tail a bit longer Mr Fox, and make hay…

Five months on from Refurbed’s €50m capital raise and it was great to read that the Austrian marketplace has passed €3 billion in cumulative GMV reaching the milestone in under 12 months after hitting the €2 billion mark in April 20258. The implied annual run rate of approximately €1 billion is broadly consistent with the 40% annual GMV growth the company cites, and aligns with the trajectory visible in its filed accounts9. The expansion into thirteen new European markets, including the UK, France, Spain and Poland, brings refurbed to 24 active markets and an addressable consumer base of 486 million. The company also cites a return to profitability, which readers of Finsur's September 2025 analysis will recall was achieved via strict cost control measures rather than any specific operational leverage. Still, it feels like there’s some momentum building and collaborations with new non-core OEMs like GoPro10 will open doors to other consumer electronics OEMs who, imho, are lagging well behind the mobile/tablet/laptop manufacturers in secondary lifecycle management. Good stuff.

Asurion has expanded its Complete Protect offering on Amazon, adding Norton 360 Deluxe cybersecurity protection, access to in-person repair services at nearly 700 uBreakiFix locations, a $100 annual credit towards maintenance of eligible furniture and appliances, and the removal of the previous 30-day waiting period for new claims, all at an unchanged monthly price of $16.9911. Complete Protect covers an unlimited quantity of eligible products purchased through Amazon, encompassing everything from laptops and gaming consoles to jewellery, rugs, mattresses, and sporting goods, provided purchase dates fall within 90 days of plan enrolment12. The product positions Asurion beyond device insurance and more as a household tech membership provider, shifting the value proposition from reactive break-fix coverage towards continuous utility aligning with Domestic & General’s subscription approach13. Those inclined to read the small print, however, will note that the T&Cs treat the cybersecurity component with some care. The plan documents describe the Norton benefits as third-party services subject to change, and explicitly state that use of them is deemed an assumption of all risks by the customer, with no liability attaching to Asurion, its administrator, or Amazon for any resulting data loss, financial loss, or reputational damage. With the press release describing Norton 360 as delivering "greater post-purchase confidence." the question is confidence for whom?

Assurant announced a new device protection partnership with Dutch flanker brand, hollandsnieuwe (HN)14. The new programme extends the existing Vodafone.nl relationship with the full-cover tier, the HN Uitgebreid at €11.95 per month and the Vodafone Garant Top at €19.00 delivering broadly comparable protection: accidental damage, defects outside warranty, theft in all forms, and loss. The Vodafone.nl product adds accessory cover up to €250, a 48-hour unauthorised use window versus 24 hours over the new HN product, alongside claims across the Benelux region rather than the Netherlands only, and express repair at no additional excess for Top policyholders. Against that, HN customers face lower excesses on every claim type: €30 versus €45 for damage, and €59 versus €100 for theft or loss. Whether those supplementary benefits justify a premium difference of €84.60 per year is a question consumers can now answer for themselves. The announcement demonstrates solid momentum in the Dutch market for Assurant having only announced a new programme with Odido back in September 2025.

Three quick fire wins from the unstoppable bolttech in the last month. Alongside Tre Sweden and Samsung, they launched Samsung Care Services with the product available exclusively through Tre’s direct sales channels15. Pretty much a standard offer covering device protection, global repair using genuine Samsung parts, and an extended battery warranty. It’s the latest in the rollout in the Samsung Bolttech journey and I’d give you a product overview if the T&Cs link pointed to the correct place. Teething issues, I’m sure. The second partnership announced was with MediaMarkt Spain to launch Alquílalo España, an electronics rental programme offering flexible contracts of 12 to 36 months, bundled damage cover, mid-contract upgrade options, and a circular return model16; the scheme went live on 5 March in 11 pilot stores and is expected to roll out across all MediaMarkt Spain locations by end of 2026, building on the existing partnership with MediaMarkt Poland. Rounding out, ASUS South Africa appointed bolttech Repairs South Africa as an authorised nationwide service partner from 1 March 2026, providing carry-in and courier repair services for both consumer and commercial ASUS devices, with typical turnaround targets of five working days for carry-in and nine for courier collections17. Busy month.

A class action filed in December 2023 by Maurice Blackburn against JB Hi-Fi, covering extended warranty sales dating back to 2011, is working its way through the Victorian Supreme Court with a sample trial scheduled for October 2026. The allegation is a familiar one in device protection circles: that the warranties largely duplicated rights consumers already held for free under Australian Consumer Law, and were sold using misleading conduct. With around eight million potential group members, the exposure is significant. Less visible is the fact that the warranties were underwritten by Virginia Surety Company and administered by The Warranty Group Australasia, both now part of Assurant, which faces an identical question in a parallel Maurice Blackburn action against Harvey Norman over its Product Care product. Despite TWG's involvement in both programmes, neither proceeding appears in Assurant's most recent 10-K filings suggesting the financial exposure might not be material, or perhaps just still unknown at this stage.

Investments

Other than Foxway’s SEK300m investment from existing investors noted above, the biggest news came from Cashify, the Gurugram-based recommerce platform as they gear up for an IPO. The company appointed ICICI Securities, JM Financial and Nomura as bankers in late March, targeting a raise of Rs 1,500–1,800 crore (~€160m–€192m), with early backers Bessemer Venture Partners, Olympus Capital Asia and Blume Ventures expected to take partial exits through an offer for sale component18. Confidential filing is planned for June to July, with listing expected in early 2027. The financial trajectory supports the ambition: FY25 operational revenue reached Rs 1,096 crore (~€117m), up approximately 17% year on year, while losses reduced 80% to Rs 10.5 crore (~€1.1m), driven by revenue growth rather than cost reduction alone. At the Series E post-money valuation of $248m on $133m revenue, Cashify was trading at roughly 1.9x revenue; the IPO target implies a more ambitious multiple on a materially improved financial profile. The parallel with Servify's own IPO preparations is hard to ignore: two Indian device lifecycle platforms, both approaching public markets in the same window, suggest the sector is achieving solid momentum in the subcontinent.

Following up on the bolttech/MoneyHero acquisition news I reported on last month, talks appear to have stalled. According to DealStreetAsia19, negotiations have been complicated by an internal investigation into MoneyHero's board chairman Kenneth Chan, with no binding agreement reached and all parties publicly silent on next steps.

Peace,

sb.