January Round Up

Device disposal, bomb disposal, and other January highlights...

I’m really looking forward to the CCS Insight Circular Markets 2026 event on 4th February this week. The attendee list is a who’s who of companies innovating and operating in the Circular Economy. I’ve covered many of them and there are a few more articles in the pipeline so it will be great to hear from the business leaders directly. If you’re a subscriber and wanted to say hello, you’ll probably find me somewhere near the front row taking plenty of notes.

With that, here’s a round up of the interesting items that caught my attention as we began 2026…

Market

The European Commission launched a public consultation on the revision of the New Legislative Framework (NLF), the 2008 infrastructure underpinning CE marking, conformity assessment and market surveillance across around 30 EU legal acts1. The consultation runs until 4 February 2026, with draft legislation currently flagged for Q3 2026 as part of a proposed European Product Act. For the secondary market, the revision is significant because the NLF was built for products being “placed on the market” once; it doesn’t natively accommodate circular scenarios where devices re‑enter commerce after repair or refurbishment. The Commission explicitly acknowledges this gap, noting that compliance may need to be assessed “dynamically, for example after recycling or repair”, and refurbishers and circular‑economy businesses are explicitly named as stakeholders in the process. The revision is also expected to be the main vehicle for rolling out Digital Product Passports as the default channel for product information and documentation across CE‑marked goods. Whether this ultimately delivers the regulatory simplification that industry groups like DigitalEurope are lobbying for, or simply adds another compliance layer on top of the existing maze, remains to be seen. I’ll dig deeper into that in a follow‑up regulatory piece building on last July’s Circular Economy Act article2.

If you see a market research report on mobile phone insurance suggesting the largest competitor globally is writing about $9bn and has 3% of the market and Telefonica Insurance writing about $180m has 1%3, with an 11.5% CAGR expectation to a total market of $60.51bn by 2030, I’d recommend ignoring it and consider a paid subscription to this substack instead because I won’t charge you $4,490 for a load of shite. Right, off the soapbox.

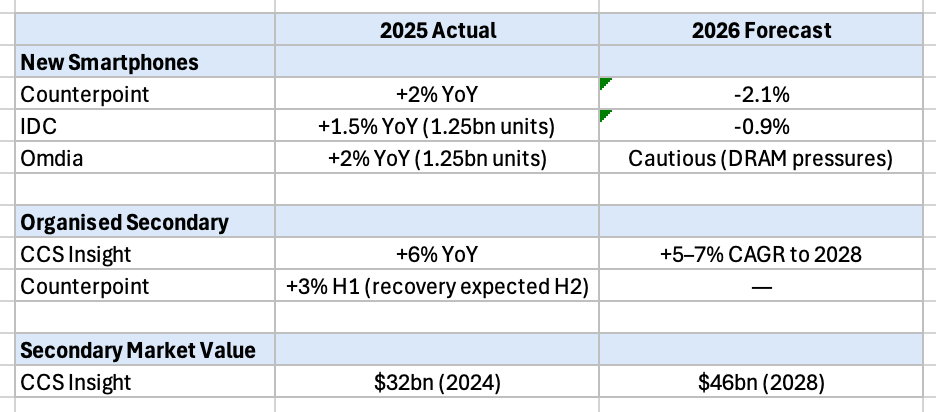

Far more credibly, Counterpoint’s final view of 20254 sell-in clearly showed Apple as the winner in the growth stakes putting on 10% to take a 20% market share overall. Samsung also appeared to benefit from the flight to premium devices putting on 5% over the year to end up with a 19% market share. Xiaomi, Vivo and Oppo remained flat in the top five, outside of which Nothing and Google performed well with 31% and 25% YoY growth respectively. However the general view is that primary market growth continues to decelerate. Counterpoint, IDC and Omdia all forecast flat-to-negative new shipments in 2026, with memory-cost pressures (CCS Insight’s Ben Wood’s “Ramageddon” sums it up nicely) weighing on ASPs and consumer demand. By contrast, the organised secondary market is emerging as the growth engine, with CCS Insight forecasting +6% growth in 2025 rebounding to sustained 5–7% expansion through 2028. Counterpoint's H1 data showed refurbished units at only +3% YoY, but expects recovery as trade-in programs scale. The secondary market is now estimated at $32B (2024) growing to $46B (2028), representing roughly 25% of new device sales in 2025 and growing market share. Here’s a summary:

Pieter Waasdorp’s Secondarymarket.news article on issues with agentic AI grabbed my attention pretty quickly5. I traced it back to an article published on Modern Retail at the beginning of the month reporting on the experience of Californian stationery seller Angie Chua6. Despite not selling on Amazon since 2016, she discovered her product catalogue had become available for sale on Amazon’s marketplace and she’d had a bunch of orders from “@buyforme.amazon”. Whilst Buy For Me remains a US-only pilot for now, it raises questions that European operators should be monitoring, particularly given the stricter regulatory environment around data protection and consumer rights that would apply if this model crossed the Atlantic. More broadly, it previews a shift in how platform commerce might evolve. If agentic intermediation becomes the norm, European refurbishers and platform sellers might be wondering if their current channel strategies are defensible. I’d start with:

Who controls how refurbished listings and data are used by AI agents, and can they re‑list or route orders without explicit consent?

When an AI agent mis‑specifies a refurbished device or creates fulfilment/returns issues, where does legal and financial responsibility sit? With the marketplace, the agent provider, or the seller?

As EU rules on platforms, product compliance and fairness evolve, will agentic commerce structurally disadvantage compliant European refurb merchants, or can it be shaped to protect their data, margins and visibility?

Peter C. Evans, writing on Platform Professional7, offers an optimistic take: AI agents will systematically favour platforms with structured, verifiable data, potentially rewarding early Digital Product Passport adopters and accelerating grading standardisation. If he's right, European refurbishers who've invested in compliance could find themselves at an advantage. Yet the FT's coverage of the current US landscape suggests we're some distance from that tidy outcome8. Amazon is suing Perplexity, blocking third-party agents, and watching its share of AI referrals collapse while Walmart hoovers up the traffic. Retail media revenues face erosion, fraud risks are multiplying, and nobody has resolved the basic question of liability when an agent gets it wrong. The commercial reality, for now, is messy. European operators would be wise to watch closely, but not to assume the American model will simply replicate itself within a regulatory environment that takes consumer protection and data rights rather more seriously.

Companies

Apple reported its fiscal Q1 2026 last week, with iPhone revenue up 23% to $85.3bn on the back of the iPhone 17 launch9. Tim Cook described demand as "simply staggering" and claimed all-time records across every geographic segment. China alone, however, appeared to carry the hardware revival with revenue surging 38% to $25.5bn, reversing the softness evident in the annual 10-K filed just months earlier. In the US, Verizon's Q4 results lend some credibility to Cook's claims; equipment revenue rose 9.1% and the consumer postpaid upgrade rate jumped from 4.5% to 5.0%, suggesting genuine sell-through10. AT&T posted similarly strong equipment revenue gains, up 12.7% to $7.4bn, reinforcing the picture of robust US sell-through11. Europe is harder to read. The region's 12.7% growth sits below the group average and could theoretically be driven almost entirely by Services rather than hardware. I'll have to wait until the likes of DT, VMO2 and Telefonica report their Q4 handset revenues to determine whether the sell-in records translated to European sell-out.

In the CCS Predictions 60 article, last December, I covered the European retention problem with hibernating phones. I’d concluded that keeping old phones for back-up in a drawer was based on fears that rarely materialise and customers might need reminding as much. So, it was great to see Cashify’s CMO aligned with the cause in India and expanding on the idea with a link to e-waste. Love it.

ecoATM reported good progress throughout the year. It’s almost impossible to get any financial information from non-listed entities in the US, so I have to make do with whatever gets self-reported. That said, management would have to be pretty happy with the collection of almost 7.5m devices over the course of the year and by hitting 7,000 kiosk installations via 21 new retail partners with over 1,100 kiosks installed in the existing retail network. Add in the Canadian expansion via marquee client Walmart, and you’d be ok with feeling a bit smug. Although I’d be feeling smugger if I could corroborate that with some financial data. According to Tracxn, ecoATM’s last raise of $50m in March 2023 was part of their $325m Series D round bringing total equity funding to just under $400m since inception. If new CEO Matt Furlong’s credentials are anything to go by, 2026 growth should shape up to be a decent curve.

EE’s device and insurance teams have had a busy few months by the looks of things. The insurance team, alongside long-term partner Chubb, announced Multi Tech Cover including loss, theft, accidental damage and extended warranty, worldwide cover backed by manufacturer approved repairs for an “unlimited” number of eligible devices12. The new offer sits alongside their existing Single Tech Cover product options which include AppleCare Services and are available during the checkout process. Multi Tech Cover starts from £15.99 a month for accidental damage policies and from £22.99 a month for full cover, including loss and theft. The cover extends to the household covering up to 20, so not unlimited then, devices belonging to spouses, partners, kids and permanently residing relatives, and despite some claims limits, breakdown claims are unlimited, possibly. Claims are settled by repair or replacement with similar spec and may be refurbished. The only comparison that quickly comes to mind is Barclays Tech Pack by Likewize.

Just about a week later, EE’s device team got in on the launch act with its refurbished range including airtime and targeting “Gen-Z Tech-Thrifters” who, according to the news release, view owning pre-owned as a badge of honour13. The range now includes New devices, Good As New devices (from EE’s 14-day returns stock) and "Refurbished Apple and Samsung devices subject to a 53-point inspection covering all the usual. A refurbished iPhone 14 in very good condition with a minimum 80% battery will set those badge-wearing GenZeders back £18.43 per month on top of £25 for a 25GB data plan14. Besides the fact that EE quote the outdated ADEME research on device carbon savings15, this is a positive initiative. Good stuff.

More news on device protection partnerships as bolttech announced a new partnership with Sony in Hong Kong16. My Sony Care+ launched in mid-December covering cameras and lenses and is expected to expand across the Xperia smartphone lines, TV’s portable music players and headphones during 2026. The development builds on Sony’s existing extended warranty offer by adding complimentary accidental and liquid damage covering repair costs up to the RRP or a one-time beyond economic repair replacement. The partnership also deepens the strategic investment relationship with Tokio Marine who provide backing for the programme. Worse news for bolttech at the beginning of the year though with the news they’d been a victim of a ransomware attack17. Ouch.

Samsung launched a broadside into the European refurbished market with the news their Certified Renewed Programme will be expanding into the UK, Germany and France18. The announcement was followed up by an excellent event at their FX store in London’s Kings Cross in collaboration with CCS Insight. I’m assuming the programme is going to take some time to scale given there’s still only one model available on their site19, but what really got me digging was a reference to the currently unavailable New Galaxy Club as a core part of their secondary market strategy. Click here for the lowdown.

Whilst researching the latest MTR Group accounts filing, I noted that Samsung had altered their trade-in UX. Previously when trading in a device, you’d get a link to a branded MTR sub-site to continue your trade-in journey. That’s all changed and the consumer no longer leaves the Samsung site to trade-in their device. For the user, it’s a significant improvement on the previous process. For Samsung, I am assuming it gives them better visibility over the trade-in price and therefore MTR’s acquisition cost on a device level basis. I’m not sure who was first to the change, but the Apple UX is now practically the same, remaining on-site rather than linking out to the Likewize Apple trade-in portal.

Recommerce Group and LiftForward have announced an exclusive European partnership combining LiftForward’s device financing and subscription platform with Recommerce’s refurbishment and buyback operations. Under the deal, Recommerce becomes LiftForward’s sole buyback partner for all European transactions and the exclusive distributor of LiftForward’s platform across the region. The alliance positions both companies to offer Forward Trade-In and upgrade programmes to retailers, carriers and OEMs. According to the release, LiftForward brings its established OEM relationships (notably Microsoft) and lender integrations (including BNP Paribas Personal Finance), while Recommerce contributes its 1.2 million device annual throughput and existing portfolio of 10+ European FTI programmes. The partnership essentially creates a single stack covering the financing front-end, trade-in orchestration and device disposition, reducing integration complexity for channel partners looking to deploy upgrade schemes and I’m fairly certain that BNP will have had their IFRS 15 Appendix B paragraphs 64 to 76 pretty well nailed for some time alongside the balance sheet to support them.

After a four-month trial, MusicMagpie have pushed beyond the direct and kiosk channels by rolling out in-store smartphone trade-ins across more than 1,300 Timpson locations20. The service offers instant assessment and payment within minutes and directly addresses what AO CEO John Roberts calls "apathy" as the biggest barrier to device trade-in. The reality may be more complex. Research into European device retention suggests behavioural barriers run deeper: 47% of consumers keep old phones as backup devices, performing "some type of functional utility calculation that guaranteed connectivity is worth more than the value of a trade-in offer." Censuswide research cited in the announcement suggests that 68% of consumers prefer to trade in devices in person and a quarter cite immediate payment as very important. The Timpson partnership certainly addresses the friction and value perception barriers, but whether instant cash can overcome backup anxiety remains to be seen. I hope so, whilst many of the drawer phones may have limited value, making trade-in habitual is going to need more initiatives like this.

I’d reported on the potential redundancies at Exertis last month after significant local and national coverage. The latest news is that approximately 400 Exertis UK employees now face involuntary redundancy after the consultation process in addition to those opting for the voluntary redundancy programme21. Not especially good news at Exertis Supplies either. VOW Wholesale, owned by EVO, is in advanced negotiations to acquire Exertis Supplies but is proposing to take only the stock and customer list, closing the Elland site entirely. Of 186 staff, just 28 would transfer to VOW's Normanton headquarters, all in sales or commercial roles. An employee rep acknowledged the potential loss of 158 jobs was "not the outcome we wanted." The TUPE transfer is scheduled to complete on 9 February22.

Investments

Assurant has acquired RL Circular Operations, the reverse logistics division of Australia's TIC Group, to strengthen its operational capabilities across Australia and New Zealand23. TIC Group, founded in 1989, operates centralised return centres and asset recovery programmes with offices in Melbourne, Auckland, Mumbai and Gurgaon. The deal reduces Assurant's reliance on third-party logistics providers in "priority APAC markets". Financial terms were not disclosed.

After the £16.5bn deal to merge Three UK with Vodafone closed last year, Hutchison continues looking for opportunities to offload its European telecom assets. Three Ireland appears to be next on the list with Liberty Global on the other side of the table in a deal reported to be worth around €1.5bn24. For Liberty Global, the acquisition would give Virgin Media Ireland its own mobile network infrastructure rather than relying on its current MVNO arrangement with Three. Hutchison is reportedly also examining disposals in Sweden and Denmark, while Reuters suggests Wind Tre has explored a potential tie-up with Iliad's Italian business. The broader picture is one of continued European MNO consolidation, with Hutchison systematically reducing its operator footprint to minority stakes and outright exits while cableco-telco convergence deals reshape national markets.

A raft of filings at Companies House preceded the news that Raylo have secured a £30m funding round comprising of £10m in equity led by Citibank alongside a further £20m in debt from existing investor NatWest25. Notably, the £10m equity arrives via a new 'Senior Shares' class ranking ahead of existing Series A and Seed+ investors in the capital structure. The funds will be applied to support continued UK growth as well as market development beginning with the US later this year. That’s not the easiest first market to tackle but perhaps the new partnership with LG, announced at the same time, will provide a lead client? The funding follows a strong FY2024 where Raylo achieved EBITDA positive status at £5.6m, a £7.5m turnaround, whilst growing billing subscriptions 59% to 92,446. However, net debt of £38.2m against just £2.3m cash at year end underlined the capital intensity of the rental model. Full analysis in my Raylo FY2024 report.

News that Foxway have acquired Romanian tech specialist ABD prompted me to look again at their covenant constraints26. ABD (All Birotic Devices Trade & Service S.R.L.) is a Bucharest-based refurbishment operation with around 50 employees, specialising in restoring devices to premium standards through respraying and skinning, essentially cosmetic restoration that allows refurbished units to command higher resale prices. The company already provides services to Foxway linked to the Teqcycle premium brand, so this is vertical integration of an existing supplier rather than market expansion. ABD reported revenue of approximately EUR 6.3m (SEK 69m) in 2024 with an 11% EBITDA margin. In previous commentary I’ve been using the full IFRS Net Debt (SEK 3,216.9m / EUR 292m at Q2 2025) and not excluding sale and leaseback liabilities, the financing structure that underpins Foxway’s DaaS growth. I apologise. The covenant-relevant figure is closer to their reported Alternative Net Debt: SEK 2,173.1m (EUR 198m) at Q3 2025. Against LTM Adjusted EBITDA of SEK 658.7m (EUR 60m), this produces a covenant leverage ratio of approximately 3.30x, well beneath the 4.50x threshold and requiring no equity contribution for debt-funded acquisitions. ABD fits easily within Foxway’s covenant capacity and even assuming full debt funding at a generous 7x EBITDA multiple, post-acquisition leverage would remain around 3.34x. The seller reinvestment element appears to reflect alignment incentives and cash conservation rather than covenant necessity. However, the structural constraint I identified would still apply to larger M&A transactions. With roughly SEK 790m (EUR 72m) of debt headroom before reaching the 4.50x threshold, Foxway can pursue bolt-on acquisitions in the EUR 5-25m range without constraint. Beyond EUR 75m, the economics tighten considerably, and anything approaching EUR 100m+ would trigger the 40% equity contribution requirement. Foxway’s FY2025 year end report is due on 26th February. I’ll cover that in full shortly thereafter.

Right, that’s about enough from me and remember, if you ever feel like your WEEE problems are getting too much, they’ll never be as bad as the poor person that came across this…

Peace,

sb.