Market Analysis: Potential Impacts of the Chip Shortage on the Secondary Market

No DRAM was spared in generating the banner image for this article...

Back in 2020, one of Apple’s declared risk factors, was that “Future operating results depend upon the Company’s ability to obtain components in sufficient quantities on commercially reasonable terms”, and it held some pretty solid boilerplate language.1 Then, after the foundry-capacity shortage hit between 2020 and 2023,2 Cupertino’s risk team provided us with more specifics in how that factor had materialised: “For example, the global semiconductor industry is experiencing high demand and shortages of supply, which has adversely affected, and could materially adversely affect, the Company’s ability to obtain sufficient quantities of components and products on commercially reasonable terms or at all.” And, whilst Apple referred to this as a past event in their 2023, 2024 and 2025 10-Ks, they added the warning that “Such disruptions could occur in the future”.3

And well they could, as Apple’s use of the present tense returned midway through the 2026 financial year with management’s discussion and analysis pointing out that: “The Company is experiencing a period of supply constraints and increasing costs for components driven by factors such as industry supply-demand imbalances for components, including advanced semiconductors, storage (NAND) and memory (DRAM). The Company expects these trends to intensify, which, together with actions that may be taken by the Company in response to such trends, may materially adversely affect demand for the Company’s products and negatively impact the Company’s revenue, costs, gross margin, results of operations and financial condition.”4 Not only are we now at component-level callouts in the interim report, Tim Cook pointed out that in addition to the memory (DRAM and NAND) price increases now hitting margin, and continuing to rise, they have an additional manufacturing constraint with SoC nodes.5 If it weren’t for the fact they are one of the world’s richest companies, ouch.

Context

Those with knowledge of the various contract priorities in play have labelled the chip shortage as an “allocation crisis”.6 Without that insight, I’ll take Apple’s lead and follow along with the supply-demand imbalance. Three firms hold roughly 90% of the DRAM market by revenue: SK hynix, Samsung and Micron, who had been happily churning out memory for all sorts of manufacturers in all sorts of sectors. Then comes along AI and their hyperscalers who need a lot more juice in the form of High Bandwidth Memory (HBM), a form of DRAM which, due to the increased demand, offers an immediate opportunity for higher margin revenue. It’s not speculative either. In October 2025, Samsung and SK hynix signed a letter of intent to supply OpenAI’s Stargate project with 900,000 DRAM wafers a month.7 Overall, HBM is due to take 23% of total DRAM wafer output in 2026, up from 19% last year.8

That creates a shortage in memory for everyone else which shows up in price, with a 130% surge in combined DRAM / SSD pricing by the end of 2026. Gartner suggests this could raise prices on PCs by 17% and on smartphones by 13% above 2025,9 although Counterpoint offered a more restrained 6.9% rise back in December last year.10 Apple, it seems, have decided to pay up and accept the margin compression, as gross margin slipped 200bps QoQ to 38.7%. Samsung, whilst elsewhere being lumped in with Apple as a co-absorber, are perhaps getting to their limit. Q1 MX operating margin fell from roughly 11.6% to 7.3% in the S26 launch quarter, even with a “captive” memory division. The margin landed in DS, and MX paid the bill, which means if Samsung can’t protect handset margins, arm’s-length OEMs are even more exposed, as highlighted by last month’s news that Xiaomi, Oppo and Vivo have planned to cut shipment targets by up to 30% as their costs cannot be absorbed or passed on to their more budget conscious customers.11 Overall, Counterpoint now expect 2026 global smartphone shipments to fall 13.9%.12

Near Term

Clearly the gap left by the drop in new device shipments is a great opportunity for the secondary market to fill with shiny refurbished devices. Well, possibly. Those devices have to come from somewhere and as I highlighted last month, the FDM CCS Insight gems from their latest Mobile Buying Guide included that over 40% of respondents say they replaced their previous phone because it was damaged or no longer functioning properly with a further 3 to 9% citing loss or theft. In other words, close to half of phones are now bought out of necessity rather than aspiration. Not only that, nearly one third of Brits plan to keep their old phone as a back-up compared with 18% planning to trade it in13 and according to the most recent Eurostat data, 51.16% of EU27’ers are keeping their old phones in the household, with 18.5% selling them or giving them away.

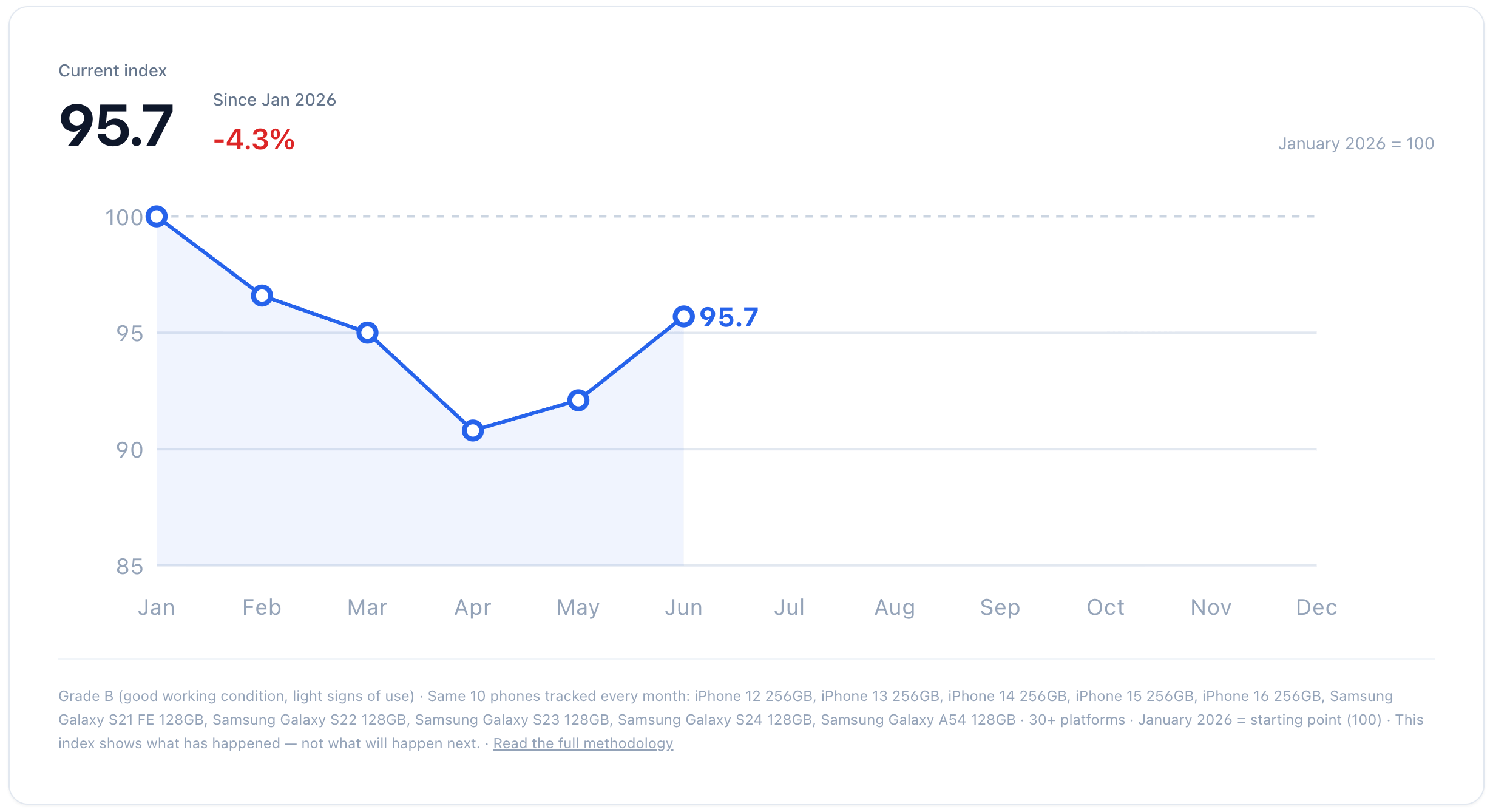

That baseline continues to leave supply stuck and whilst having a back-up device close to hand or being concerned about privacy and security concerns are valid, increasing the offer price to consumers is perhaps the quickest way to reduce trade-in friction and begin to unstick supply. Asset depreciation over time is rarely linear, although baking in an approximate 2% monthly decline for smartphones has been there or thereabouts for years. But Apple bucked the trend back in May with price rises clustered around the current flagship and most recent Pro models. The iPhone 16 Pro Max was up £55 in the UK and €20 in Germany. The devices that rose the most, or even rose at all are the models that Apple wants owners trading up from, presumably to the iPhone 17 or even 18 equivalents in a few month’s time. True, this is a single snapshot, but if prices rise again at the next update, it points at the shortage doing to used values what it is already doing elsewhere to new prices. More widely, RecommerceIQ’s monthly buyback index, covering grade-B stock in France, Germany and Italy show pricing falling 9.2% from the start of the year until April and then ticking back up a total of 4.9% over May and June.14

For the 18% of us that trade-in, the cost of upgrading is the price of new minus the trade-in. That gap only holds steady if the trade-in prices rise by the same cash amount as all those new phones coming under pricing pressure. Picking the more recent Gartner 13% price rise on a flagship device near £1,200 is roughly £150. Apple’s best trade-in uplift of £55 is about a third of that. So the price gap is widening. The chip shortage lifts new prices faster than it lifts used values and the widening gap should be precisely what pushes consumers towards a refurbished device.

So does any of this prise the phone drawer open? Probably not, or at least not by much. Those phones are being kept as back-ups, despite the actual instances of failure being rare, and due to privacy and security concerns, that are probably over-indexed. Not, for the most part, because the trade-in offer price was too mean. That’s not to say improving the offer won’t reduce the friction, but a larger cheque doesn’t automatically make sense for someone holding onto an old handset as insurance against losing or breaking the new one. There is a second mismatch too. The rises landed on the current flagships and recent Pro models, which are precisely the devices least likely to be sitting forgotten in a drawer. The phones that are gathering dust are older, and their values remain flat or still falling. So the offer improves on the phones people are keeping in use, and barely moves on the ones they have already set aside. Add to that the widening gap, and the upgrade maths gets worse rather than better for the very people deciding whether it is worth the bother. The likelier outcome, then, is that the shortage grows demand for secondary devices while leaving the supply of them much as we found it with the drawer staying shut.

Medium Term

Whilst the near-term impacts of the chip shortage fit neatly into a kitchen drawer sized box, the secondary market impact over the medium and longer term is harder to predict due to the compound effect across the inputs and it’s not all one-directional.

On the basis of my survey data from last year, I noted the drift from an average primary hold time of 3.4 years to 3.67 years.15 In that article I used a cohort model, rather than a simple average, because the extended lifecycle owners would only be a small slice of the base to begin with. This means the effect is back-loaded as each year’s cohort holds longer and the cohorts stack, the drag compounds with new UK sales falling to an estimated 13.1m units by 2028, a cumulative 9% contraction and approximately 1.3m fewer devices in the pool driven by people keeping their phones just a little longer. The effect of a primary market releasing fewer devices starves the channel that depends on them with devices that are being returned arriving a bit more (ab)used and a bit more depreciated with lower residuals. A smaller and lower grade pool before the chip shortage entered the fray.

The recent Telco Equipment Revenue Trackers go some way to provide evidence of the decline predicted in the cohort model.1617 Across mature Western Markets, handset revenues are now falling, in some instances enough for operators to bury the numbers alongside multiple other spurious revenue lines. There are some outliers, and there are some markets, particularly in Eastern Europe that are earlier in their cycles and still growing. But, they are not large enough to offset the larger, more mature sources of device volume. The trackers were written to explain the telco equipment revenue as a supply forecast for the secondary market. Every quarter of contraction in the mature core is another quarter of devices that will not be arriving from the carriers between 2028 and 2030. And, whilst Apple are trying their hardest to offset the overall decline, the channel switch to direct buying from the OEMs isn’t enough to plug the gap.18

Where last year’s model had one slow variable, hold times drifting upwards, the chip shortage adds a second force that drives the first. Pricier new phones and a widening upgrade gap will perhaps push people to hold even longer, so the shortage deepens the contraction, suppressing new volume now while stretching the replacement cycle further and thinning the trade-in pool later. And it bites on quality again just as much as volume since, according to the CCS data, the upgrades that do happen are increasingly forced ones, with devices coming back harder used rather than merely older.

Everything so far points one way, thinner and poorer, but there is a force pulling the other way. The same shortage that suppresses supply is lifting residual values, and rising trade-in offers are the one thing that could keep or shake devices out of the drawer against the hold-time drift. The net more likely to be fewer devices to compete for, but certainly not a complete collapse. I’ll be keeping an eye on the chippy’s for more indicators along the way…

Peace,

sb.

2023 10-K available at:https://d18rn0p25nwr6d.cloudfront.net/CIK-0000320193/faab4555-c69b-438a-aaf7-e09305f87ca3.pdf

2024 10-K available at https://d18rn0p25nwr6d.cloudfront.net/CIK-0000320193/c87043b9-5d89-4717-9f49-c4f9663d0061.pdf

2025 10-K available at: https://d18rn0p25nwr6d.cloudfront.net/CIK-0000320193/c24e7a28-5254-4dfa-9447-62aaa3c24bb1.pdf