Alchemy FY2025 Financials: $826m Revenue, $400m to $500m Implied Equity Value

If the slipper fits...

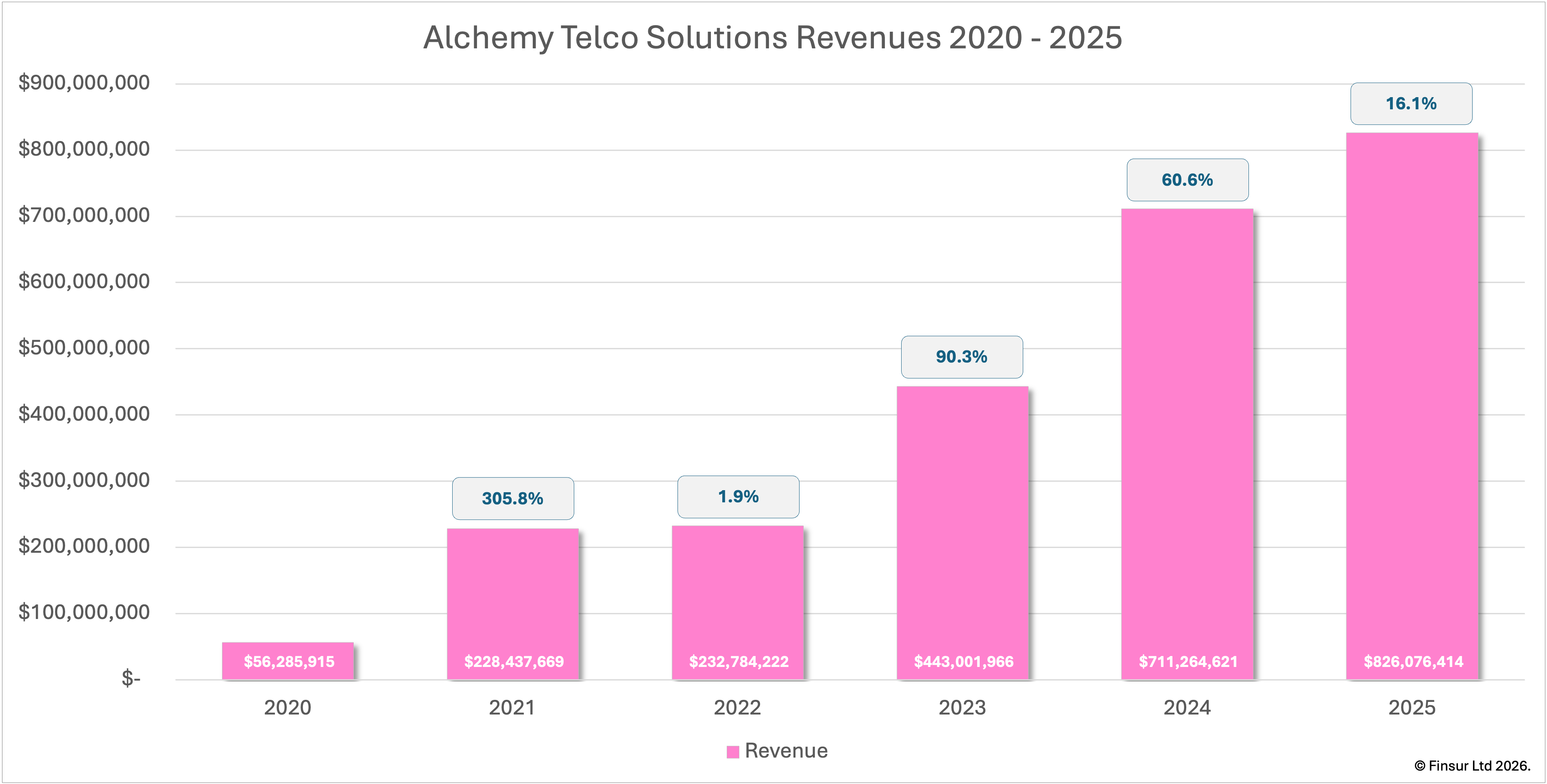

Key Findings: FY2025 revenue $826m | +16.1% YoY. Operating leverage textbook: gross profit +32.9% to $73.5m, EBITDA +64% to $33.4m at 4.04% margin, profit for the year +98.3% to $24.0m. Gross margin recovered 112bps to 8.90% as the FY2024 inventory unwound from $113.9m to $88.2m without margin penalty. Balance sheet transformed: cash tripled to $98.0m, $39.8m of borrowings cleared, KPMG installed as auditor, employee share option plan active. Implied equity valuation $400m to $500m, central case $450m, anchored on Genstar's 10x at Likewize. Macquarie's 45% stake worth approximately $200m at the central case. Full analysis available as a downloadable report at reports.finsur.co.uk

When is the right time to sell? Probably sooner than you want to believe and Macquarie didn't earn the Millionaires' Factory nickname by waiting until midnight at the party. On 30th April 2026, Alchemy filed their FY2025 accounts and they read like a business about to climb into the carriage and head to the ball: borrowings cleared, cash tripled to $98m, Macquarie short-term funding run down from $10.6m to $55k and KPMG installed as auditor. Whatever the immediate intent, this is what getting ready looks like.

Recap

Since the first Finsur analysis on Alchemy Telco Solutions back in March 2025, all the basics have remained stable. Ownership is still split between management’s Enviro Management Consultants Limited (EMC) with 55% and Macquarie with 45%. The structure still flows from the Irish entity (company number 595997). The principal activity remains smart device trading and collections. Key director slate is unchanged with Walter Vicente and Gary Noone representing EMC and Lou Tricarico and Kevin Doherty representing Macquarie with James Murdock (Group CMO) as founding executive on the UK entity slate.

Alchemy Telco Solutions Canada appeared for the first time in the consolidated subsidiary list joining the entities in Ireland, the UK, US, Australia, Hong Kong, Japan and Dubai. Notably, key management positions were strengthened with Fraser Parker joining as Group CFO in March 2025, Alex Croft picking up the helm as Managing Director for the UK in May, Hirofumi Yamada as Managing Director, Japan in July and Alexandra Hussenot becoming Managing Director, Europe in November.

Some of the external positioning appears to have been given a bit of a buff and polish. Five capabilities are now more clearly defined: Alchemy Circularity offers a managed service for OEMs, retailers and carriers; Alchemy Trading focus on B2B wholesale transactions; Callisto the trading platform is now positioned explicitly for repairers, resellers and SMB wholesale; Loop Mobile focuses on B2C ecommerce reaching consumers directly and indirectly via the major European marketplaces; and Loop Business does the same in B2B mode for small businesses.

More recently, Alchemy were recognised by Deloitte as a winner of their Impact Award1 in December 2025. There was a fireside chat with Stephen Wise (Global Marketing Director) at the FDM CCS Insight Circular Markets 2026 event in February 20262 and a second consecutive FT1000 listing in March 20263, although I dislike the Waste Management & Recycling sector categorisation. Perhaps most indicatively, Macquarie’s own Commodities and Global Markets business published their case study on Alchemy framing them as a “$1bn industry leader” with more than 3000 customers in 60 countries, supported by 16 processing facilities in 13 countries across 5 continents4. Just South America and Antarctica to go then.

FY2025 closed thirteen months ago. The signals since suggest a business that has continued to accelerate. The question is whether the audited numbers support the inferred trajectory or merely set the floor for it. Let's dive in…

Performance

FY2025 revenue was up 16.1% to $826.1m (FY2024: $711.3m), an actual increase of $114.8m. Not too shabby at all, but well short of my $950m forecast which I based on a continuing declining revenue growth range of just over 33%. That’s me perhaps being over optimistic but still, their five-year CAGR holds up extremely well at 71%.

All revenue is reported under a single class of business (smart device trading and collections) and beyond geography there is no segment disclosure. Ireland posted $1.5m (0.18% of total revenue) and down from $1.8m in FY2024. The UK posted $58.4m in revenue (7.07% of total) and was essentially flat from $58.9m (8.28% of total) which all points to growth consolidating in the Rest of the World, up 17.8% to $766.1m and 92.7% of total revenue from $650.6m or 91.5% of the FY2024 total. As I flagged last time, filing limitations in the US and Japan prevent further meaningful disaggregation but the partner profile (Apple, Verizon, T-Mobile, Best Buy, Walmart, Amazon, Back Market, eBay, Asurion, Assurant), keeps the centre of gravity firmly in the US.

Whilst no unit information is provided in the accounts, Macquarie’s case study claim of more than 12 million devices processed to March 2026 against cumulative group revenue of approximately $3.6bn through that date (also relying on the stated $1bn in 2026)5, implies a current-period blended ASP in the $300 to $350 range. Applied to FY2025 puts the implied volume at approximately 2.4 to 2.75m for the year. Headcount rose from 222 to 245 (+10.4%) against revenue growth of 16.1%, taking revenue per Alchemist from $3.20m to $3.37m, a 5.3% improvement.

For the year ended December 2025, ATRenew Q4 2025 posted 28.9% growth on $3.0bn. Foxway’s Q4 FY2025 results showed that the Mobile Recommerce segment declined 2.3% on a constant currency basis for the same period, with Alchemy sitting neatly between the two. I’ve included the main PCS Wireless entity in Europe and the Likewize Services UK entity for completeness, but in revenue terms, neither disclose their full stories.

In a Yahoo Finance interview published on 1 March 2025, James Murdock described Alchemy as “doing around $900m of business” with the company reported as “on track for a run rate over $1bn through 2025”6. Macquarie’s case study cites “annual revenues of more than $1bn”, both of which reference roughly the same TTM March 2026 window. This implies that the Q1 to Q3 FY2026 quarterly trajectory was running materially ahead of the FY2025 average. Whether through organic acceleration, related entity revenue or platform GMV recognition, the trajectory is clearly upward. With revenue growth decelerating to 16.1% but the public framing pointing at a $1bn run-rate, the value in this set of accounts shows up below the revenue line.

Finsur is reader-supported and the analysis takes time. If you want the full picture on Alchemy's profitability story, the balance sheet transformation, the valuation work and the three paths management may take, a paid subscription continues from here. Alternatively, the full report is available as a downloadable report here.